As corporates increasingly commit to “green” commodity production and marketing strategies, it will be critical to understand the prospects for any resulting price premia (and the implications for profitability from investment in decarbonisation).

In this Spotlight we discuss the fundamental drivers of, and outlook for, green premia across a range of commodities. These are shown to differ widely across markets depending on consumer preferences, the structure of individual production chains, and the supply of eligible products in any market, both now and in the future. CRU Consulting have deep expertise in evaluating pricing drivers in metals, mining and fertilizer markets. We are actively helping clients to assess market balances for “green” and “brown” product segments as a basis for better understanding the potential terms of trade or bargaining power in any future contract negotiations. To discuss these opportunities further, please contact via the form below.

Green commodities are emerging…

One way or another, consumers are likely to pick up the tab for the costs of reducing the environmental footprint of mining, metals, and fertilizer production. However, these can be recovered in different ways, including indirectly through lower returns to equity holdings, or as a result of increased government funding requirements. Of perhaps most direct consideration will be the mechanisms by which commodity prices are impacted. Here, either governments will tax producers in relation to the damage caused, thereby (in theory, at least) encouraging firms to clean up production to avoid a commercial penalty. This is currently the case, for example, with greenhouse gas emissions from the production of steel, aluminium, nitrogen and other industrial products in the EU Emissions Trading Scheme (see here for more details). Alternatively, benchmark prices may remain largely unaffected with consumers paying a premium for greener products.

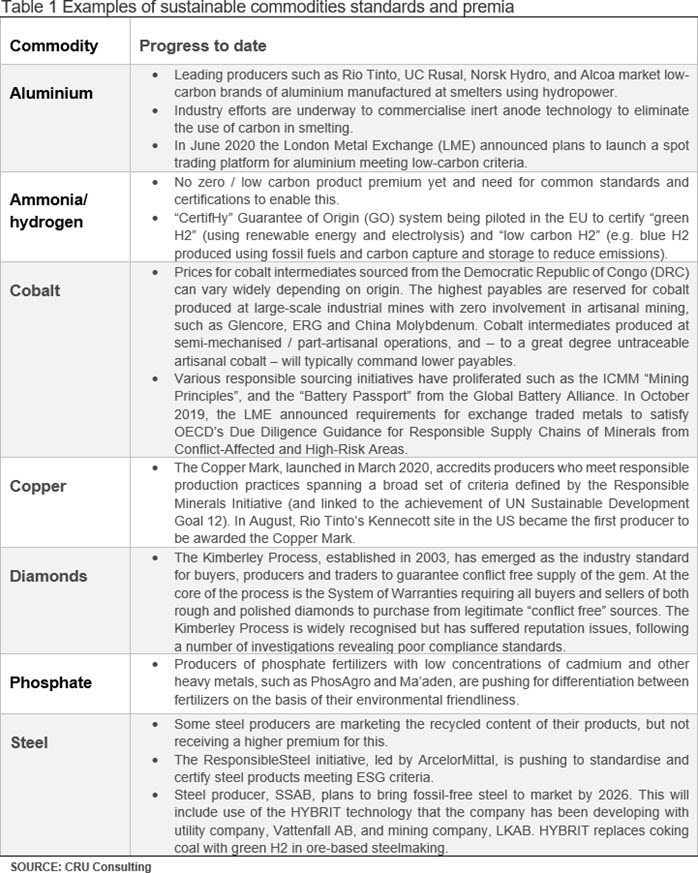

Differences between a given contract price and a global reference price for a commodity can exist for a whole variety of reasons, including (but not limited to) its product specifications, marketing costs, processing requirements, contract terms, etc. To enable a “green” premium, producers first need to clearly delineate the often otherwise hidden environmental characteristics of their products – based on standards, labels and certificates – which are both recognised and valued by customers. A number of examples of products seeking to demonstrate higher environmental, social or governance (ESG) standards have already begun to emerge across a range of commodities, but (with a few exceptions) remain quite limited in scope (see Table 1 for a high-level summary).

As metals, mining and fertilizer producers increasingly set out their commitments to develop and orientate their corporate and marketing strategies around “green” commodities, it will be increasingly critical to understand the commercial prospects for environmental product premiums, particularly where large scale investment is required to enable such a pivot. This requires a proper assessment of the drivers of future demand and supply (and the value and terms of trade associated) with more environmentally sustainable and socially responsible products.

Will consumers pay a premium?

Consumer preferences in favour of cleaner, yet more expensive, products are necessary (but not sufficient) for a green premium to exist. On the face of it, the value placed by consumers on a range of ESG related issues is on the rise, particularly among younger consumers in western countries. Within the environmental space specifically, carbon emissions and climate change are rising up the social and consumer agenda: this is evident, for example, from the mass protests at the UN Climate Conference in 2019 (or the growth in the “Extinction Rebellion” movement).

To date there is little historical precedent for low carbon commodities commanding a premium. But, as we know, the past is not always a guide to the future. Consumers have previously demonstrated a willingness to saddle costs associated with higher social and governance standards, including in agriculture. Fair Trade coffee, or Forest Stewardship Council certified wood products, are commonly purchased at a roughly 15-25% mark up. However, it is also noteworthy that, decades after their introduction, such brands still account for a small share of the market (just 1% in the case of Fairtrade coffee).

The conditions for discovering whether a price difference for sustainable metals could exist are increasingly falling into place. Exchanges such as the London Metal Exchange (LME), for example, now enable consumers to identify and source low-carbon aluminium on their trading platform. At this stage, however, it is unclear if there will be sufficient demand and supply for low carbon materials for such “decommoditisation” to take place. Overall, this is likely to differ across materials according to patterns in their usage and cost, as well as the nature and market structure associated with their production and trade.

These considerations could ultimately be so fundamental as to determine market access. For several years, for example, cobalt that was perceived as at risk of violating human rights and causing pollution (particularly contracts potentially involving artisanal supplies from DRC), traded at a roughly 20-25 percent discount compared to LME prices. Since 2019, however, all cobalt traded on the exchange is required to undertake an audit assessment of its compliance with OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas (or equivalent), with full compliance from 2023.

Visibility to final consumers matters for demand

A key barrier to charging a premium for low carbon and other forms of green commodities is that they are often sold into a manufacturing chain or embedded into investment goods (making them weakly visible to final consumers), and where there are not yet markets for identifiably sustainable products. Thus, the high dependency of commodities, such as steel, on demand from the construction industries is a potential impediment to the emergence of a green premium. The structure of the value chain also matters: the existence of intermediary supply chain entities – whose purchasing decisions are weakly visible to the final customer and whose products are highly substitutable with other suppliers of semi processed goods – are a potentially key obstacle to robust demand side for green metals.

On the flip side, the closer and more visible a supplier is to the final customer, the more conducive the conditions are for green premia, particularly where there are clear links between particular consumer choices and the associated environmental outcomes. Metals demand in sectors such as automotives and consumer electronics, for example, are already demonstrating a high degree of sensitivity to ESG-related factors: major buyers of cobalt, including Apple, VW and Tesla are increasingly demanding that all metal procured satisfies high ethical and environmental standards. Moreover, with producers such as Huayou Cobalt now deciding to stop buying product from artisanal producers, the growth of responsible sourcing can no longer be considered a purely “Western” concept.

As is clear from CRU and Fitch’s joint special report on Emerging ESG Risks in the Metals and Mining Value Chain, the focus is now increasingly shifting towards carbon emissions: in July, for example, Apple committed to being 100 percent carbon neutral for its supply chain and products by 2030 (building on its existing commitments to purchase carbon free aluminium). Volkswagen and Toyota are also among the major corporates with the ambitious aim of eliminating carbon emissions completely from their entire value chains (including their suppliers and from a full life cycle perspective).

However, not all consumer brands will be as able to discriminate in their raw materials sourcing as high value vehicle and electronics manufacturers due to differences in fundamental cost structures and substitution possibilities. The share of raw materials costs in final product values (and the costs of greening the supply chain relative to overall margins) will differ across commodities and end uses. In the case of aluminium beverage cans or food packaging, raw materials costs are critical to profitability, by contrast the cost of aluminium used in a car is a fraction of the final sales value. Moreover, the existence of alternative materials for the production of food and drinks receptacles increases the price elasticity of demand.

Demand for green construction and investment materials currently lags, but may evolve…

What is the prospect for end uses outside of automotive and high value electronics and consumer products to start demanding (and, importantly, paying for) greener products? Take the steel industry, for example, where – according to analysis by CRU Consulting – billions of dollars of value are potentially at risk under a 2 degree and other stringent decarbonisation scenarios. Steel industry players are subject to growing pressure from investors and are piloting numerous process innovations designed to reduce the carbon footprint of their products.

However, to date there remains limited evidence of product discrimination among mainstream construction industry clients. This is not to suggest, however, that preferences will remain static (indeed our own market intelligence suggests that producers and intermediaries are beginning to anticipate a gradual shift in customer appetite for low carbon construction materials). Producers are also seeking to stimulate a greener downstream. In 2018, ArcelorMittal, for example, launched Steligence, a new information service aimed at promoting a more holistic use of steel in construction, through supporting steel customers and building designers to develop and construct buildings with steels that use less material, embody less CO2 and improve occupancy value.

Moreover, shifts in government policy may also act as a potential catalyst of structural change, including through increased focus on public procurement as a potential policy instrument in recent years. Governments in around 60 countries – including both leading industrialised countries and major emerging markets such as Brazil, China, India, Indonesia, and South Africa – are now employing environmental criteria alongside traditional cost and service quality metrics. For example, the construction of the Sydney Metro Northwest – one of Australia’s biggest public transport projects comprising 31 metro stations and more than 66 kms of new metro rail – imposed specific sustainability requirements on steel procurement and construction related emissions.

What would a step change in the application of such rules mean in practice? To date, the impact of these and other demand creation schemes remains unclear, warranting deeper enquiry into the implications of any future structural shift in green metals demand associated with the investment and construction space.

Understanding supply is critical

Fundamentally, any green premia would emerge from negotiations between buyers and sellers designed to account for the specific ESG characteristics of whatever commodity is being delivered and where. Clearly such outcomes would be specific to the market, buyer and product in question (and could differ across products, regions and time). Nonetheless, it should be intuitive that the outlook for any low carbon premia would also depend on the market supply of eligible products: scarce supplies, in the presence of a market demand, being conducive to an emergent premium. This, in turn, will be impacted by a range of factors including the structure of the value chain, the environmental standards required by customers, the costs of compliance with these standards and, of course, the magnitude and stability of any premium.

Once again, the structure and transparency of the industry will matter. Complex value chains require consistent certification at each step of the chain to validate consumption standards to the final consumer. For example, in the case of developing a premium for “green ammonia”, this requires both certificates of origin relating to the supply of renewable energy in hydrogen production, and for the processing of the hydrogen into ammonia. Certification will need to differentiate between zero carbon ammonia using solely green ammonia, versus low carbon ammonia from fossil fuels using some carbon abatement technologies, such as carbon capture and storage (e.g. “blue ammonia”). The complexity and opacity of these changes, and the degree of trust which exists between buyers and sellers, thus has the potential to shape supply.

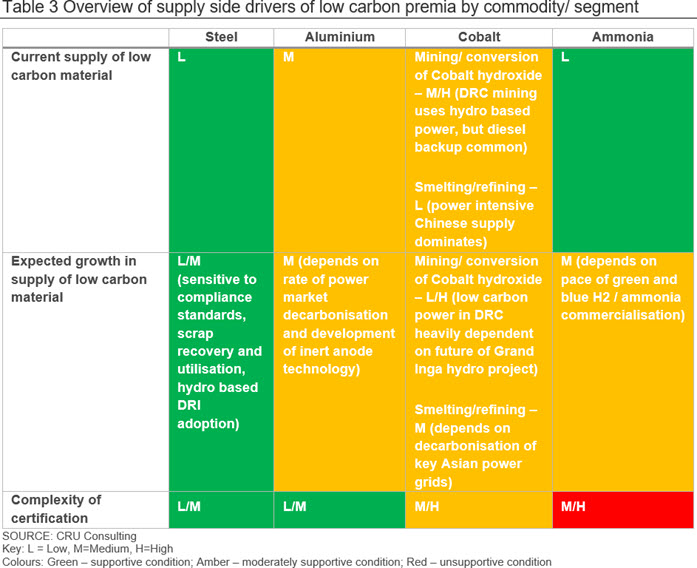

Market and technological factors will also have an important bearing: the lower the carbon intensity required by customers, and the higher cost of compliance (relative to any premium), the more limited the supply. Take the steel industry as a case in point: CRU’s steel carbon curve suggests that less than ~10 percent of production has a CO2 intensity of lower than 0.5 tonnes per tonne of steel. In contrast, in the aluminium industry, a relatively higher proportion of production – ~25-40% of the global total – has effectively zero scope 2 emissions due to the availability of hydropower, potentially representing ample supply of low carbon metal for interested end users.

Moreover, supply will evolve differently across industries and regions (particularly if trade policies continue to be employed to create exchange frictions). This will require a proper understanding of policy and corporate decision making, informed by the potential for both incremental process efficiencies and longer term transformative technological change, as well as the associated cost implications. In the case of steel, for example, CRU identify substantial opportunities for reducing emissions with the adoption of best available technologies in traditional steelmaking (see here for a discussion). By contrast, our view is for more limited future reductions in the power intensity of aluminium manufacture (although the potential for decarbonisation of power is relatively higher).

The outlook for green price premia

One way or another, consumers are likely to pick up the tab for the costs of reducing the environmental footprint of mining, metals and fertilizer production, including through higher commodity prices, lower returns to equity holdings or increased government funding requirements. As producers increasingly develop and orientate their corporate strategies around “green” commodities, it will thus be critical to understand the commercial prospects for future pricing premia, particularly where large scale investment is required to pivot a business.

Fundamentally, any green premia would emerge from negotiations between buyers and sellers. This will require an understanding of consumer preferences for low carbon materials as well as the structure of, and technologies employed in the supply chains through which they are delivered (both now and in the future). Clearly such outcomes would be specific to the market, buyer and product in question (and could plausibly differ across products, regions and time), depending on the market supply of eligible products, and potential barriers to entry and trade.

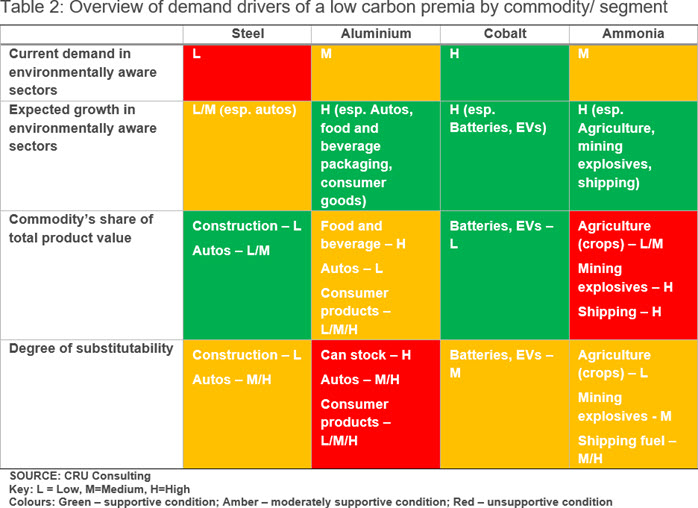

Among the commodities reviewed in this article, we find that demand conditions for a future low carbon materials premia are overall most favourable in cobalt, with material supply currently most abundant. The aluminium industry is perhaps the most intriguing test case for a low-carbon premium emerging – it is a material emitter, and there is a significant differential between the best and worst in the industry. The challenge now is whether it can grow the demand for low carbon product sufficient to tighten this section of the market to the extent where a significant premium could emerge.

The issues and questions raised here are both fundamental and challenging, warranting proper analysis and evaluation, with a particular focus on future dynamics. CRU Consulting have deep expertise in evaluating pricing drivers in mining, metals and fertilizer markets, including in relation to environmental factors. Our approach focuses on understanding the potential future market balances for low carbon versus high carbon product segments as a basis for better understanding the potential terms of trade or bargaining power in any future contract negotiations. Drawing on negotiation theory, this enables us to analyse the value of the best available outside option for both buyers and sellers in each region and market (taking account, where relevant, linkages between these), in order to define and evaluate the bargaining zone governing any future premia across regions and segments.

Explore this topic with CRU

CRU Consulting

-

Rebecca Gordon

Chief Executive Officer, CRU Consulting London -

Francisco Acuna

Principal Consultant Santiago -

Jessica Alves

Consultant Sydney -

Marcelo Bolton

Senior Consultant Santiago -

Juan Brihet

Senior Consultant Santiago