The European Green Deal sets ambitious targets to reduce net greenhouse gas emissions by at least 55% compared to 1990 levels by 2030 and to become climate neutral in 2050.The European Commission estimates that achieving these targets would require additional investment of €520 billion (bn) each year over the coming decade, over and above what is already being spent. This is equivalent to 3.3% of EU GDP in 2022 or 6.6% of the bloc’s government spending. It is easy to argue that the cost of the green transition could be even higher, as the cost of public investment is notoriously prone to underestimates. An estimate by the University of Greenwich suggests that the additional investment required for a successful transition would be up to €855 bn per year, not including investment in transport.

Achieving the EU’s climate targets will stretch public finances

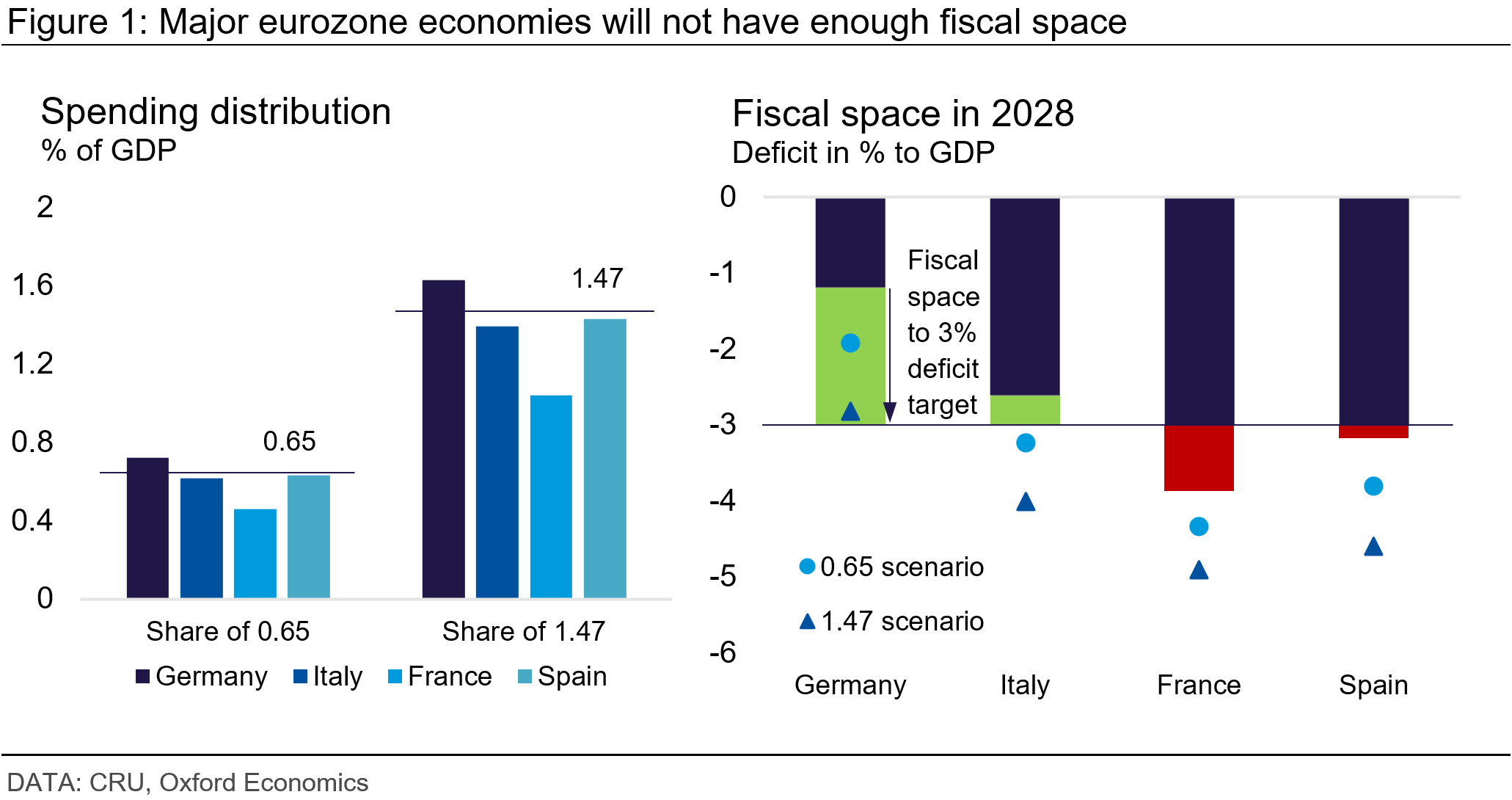

Assuming an additional annual investment need of 3.3% of GDP and using information from the National Energy and Climate Plans as well as previous literature, we assume that between 20% and 45% of the additional funding requirement will need to be financed by governments. We study two scenarios, one with a government share of 20% as a lower limit and one with 45% as the upper limit. The costs are therefore estimated at 0.65% and 1.47% of EU GDP, annually. Following the economic literature, we assume that investment needs will be relative to current emission levels. That is, the higher the current emission levels, the higher the investment needs in a given country. Following this approach, we calculate the investment needs for the four major eurozone economies, i.e. Germany, France, Italy and Spain (see Figure 1, left-hand side).

There is insufficient fiscal space under EU rules despite budget consolidation

European governments are expected to tighten their belts and we forecast the deficit ratio in European economies to fall over our forecast horizon. However, even in 2028, after five years of fiscal tightening, only Germany would have sufficient fiscal space to finance both spending scenarios (see Figure 1, right-hand side) (ignoring Germany’s own debt break rules which limit the federal structural deficit to 0.35% of GDP). The other three major European economies would not be able to finance either the lower limit nor the upper limit scenario without exceeding the EU deficit limit of 3% of GDP, cutting other expenditure, or raising taxes.

Increased fiscal pressure will not only come from the green transition, but also from countries' plans to increase their military spending in order to meet NATO's 2% target. Ageing populations will also put pressure on public spending. Of the four major European economies, only France is meeting its NATO commitment, while Germany (1.4% of GDP in 2022), Spain (1.5% of GDP in 2022) and Italy (1.7% of GDP in 2022) would all have to increase public spending to reach 2%.

A possible route forward could be to exempt climate spending from the EU fiscal rules or to introduce a common debt mechanism for investment in the green transition, but northern countries, including Germany, would heavily resist either proposal. The EU could also put more of the burden of adjustment on market mechanisms such as carbon pricing, which create incentives for the private sector to invest. However, this will pass costs onto businesses and consumers in a very visible way, which will be politically unpopular.

The EU faces an unpalatable set of choices if it wishes to pursue both its climate goals and prudent fiscal policy. This trade-off is no less real in the US but is currently being ignored by politicians – with neither party showing any inclination to reduce large fiscal deficits. Even though EU governments have agreed on a slightly less stringent fiscal framework, we believe that meeting the bloc’s ambitious climate targets by 2030 will be challenging for public finances. We should also not rule out the possibility that the next European Parliament and European Commission might pursue a less ambitious climate policy.

Explore this topic with CRU