In the next month, we forecast carbon prices will be stable. Hydro will stay strong across mainland Europe with above average precipitation forecast for end-December, but wind has the potential to underperform with the forecast dying down by the end of the year.

Hydro will continue to perform strongly, while wind may taper

Hydro has had an exceptional December and, although wind output was down m/m, it was still performing at above average levels. Above average precipitation is forecast for the next couple of weeks and reservoir levels are high, so strong hydro output is expected across mainland Europe to continue over the next month. Wind is forecast to stay strong over the next week but has the potential to drop below average and poses an upside risk to EUA demand. Overall, our base case view is that renewables will have marginal impact on the carbon price in January, with an upside risk if wind underperforms.

Gas prices will stay low in January

Gas prices plummeted in December, causing a reversal of prior gas-to-coal switching across Europe. Gas prices are forecast to stay low and coal prices are expected to rise slightly to render gas even more competitive with coal. However, this will have minimal impact on EUA demand as further switching should be limited.

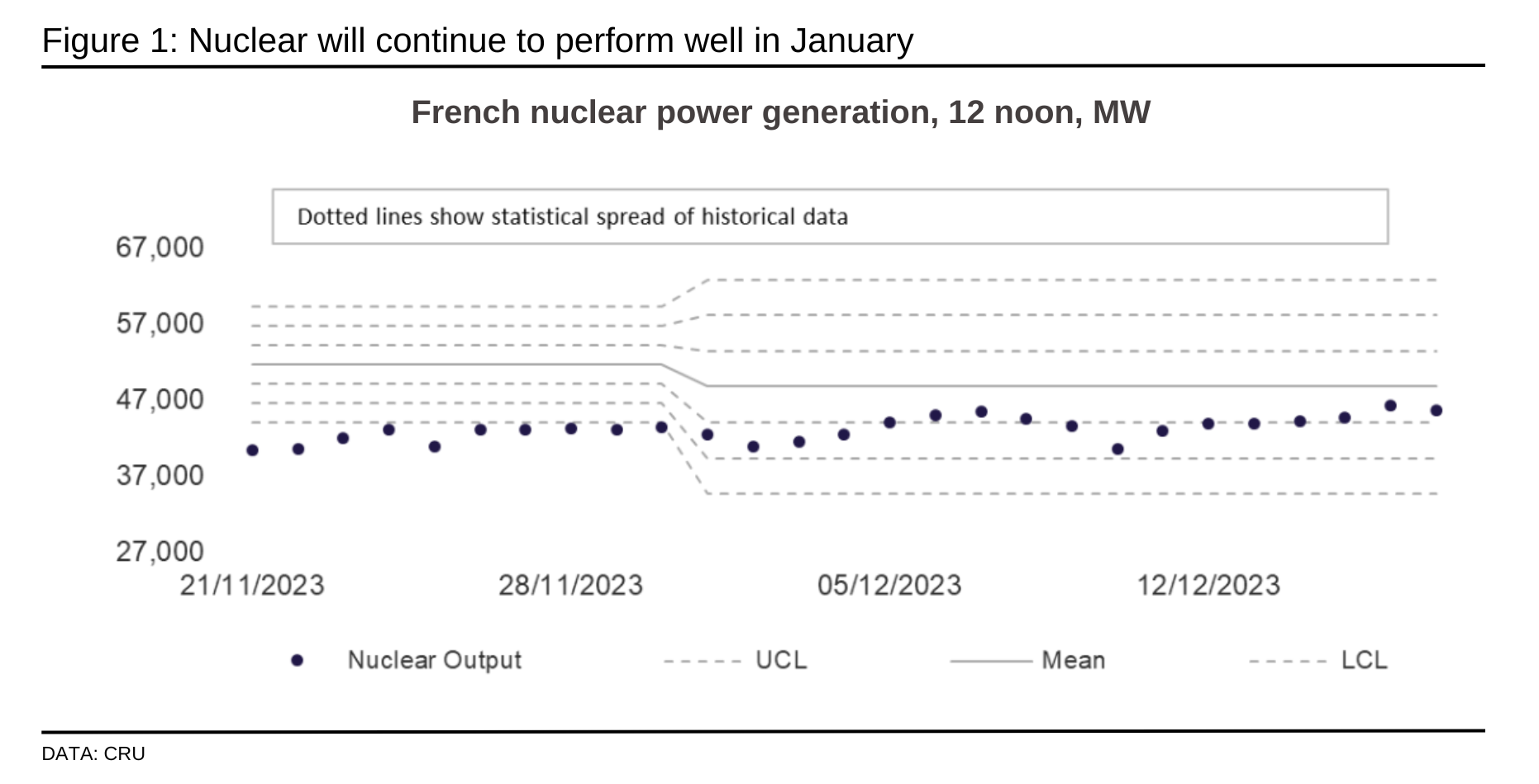

Nuclear outlook is good for January

The French nuclear fleet underperformed in November but, with reactors back online, there was strong output in December. With no major openings/closures planned for end-December/January, the outlook for nuclear is good. Our base case view is that nuclear will be stable in January and will have minimal additional impact on the carbon price.

Outlook hasn’t changed for the economy and industry

As the economy continues to struggle, the outlook for industrial output remains weak. Power demand has been up m/m due to seasonal heating demand, but warmer than average temperatures are forecast for the next month and energy demand from industry will remain low. Energy demand from industry has the potential to drop further over the holiday period, if holiday stoppages are extended, which poses a downside risk to EUA demand. Overall, industrial output and the economy will be stable over the next month and will have little differential impact on carbon price, with downside risks.

If you want to hear more about carbon market developments and our short-, medium- or long-term carbon price forecasts that are provided as part of CRU’s Sustainability and Emissions service, please email us at sales@crugroup.com, we’d be happy to discuss this with you.

The cut-off date of the data is 18 December 2023.

These and other economic developments that impact commodity markets are discussed with CRU subscribers regularly. To enquire about CRU services or to discuss this topic in detail, get in touch with us.

CRU experts discussed the impact of the war in Ukraine on commodity markets in a recent webinar. Experts from all major commodity areas joined CRU’s Head of Economics and an energy specialist to discuss markets one month on from the invasion of Ukraine. The webinar is available to watch on-demand here.

Explore this topic with CRU