ContributorAurelien Henry

Senior Consultant View profile

ContributorLewis Pegrum

Senior Consultant View profileInstitutional investors and asset managers – in partnership with corporate management teams as well as their suppliers and customers – have a central role to play in supporting the decarbonisation of raw materials production and processing.

Reflecting this, major institutional investors and asset managers are beginning to commit to aligning their capital allocation to the Paris Agreement goals: in January, for example, BlackRock – the world’s largest asset manager – announced sweeping changes to its investment approach in light of the climate challenge. In October, HSBC announced a commitment to enabling net zero carbon emissions across its entire customer base by 2050. To help measure progress towards greener equity and debt portfolios, CRU Consulting have developed robust, transparent and consistent emissions benchmarks relating to the mining, metals and fertilizer industries. In the case of the equity holdings in the top 15 listed steel and aluminium producers by major asset managers, we find a heavy concentration of associated emissions in the portfolios of BlackRock, HSBC and Vanguard. In addition, for a sub-sample of five major asset managers, we find somewhat mixed evidence that corporates with lower average carbon intensity of production have a greater propensity to attract capital from actively managed funds. To discuss any of these issues, or better understand their potential implications for your business, please contact us.

Climate change mitigation requires a massive shift in investment

Massive investment in the mining, metals and fertilizers industries is required to support the transition to a low-carbon economy. Burgeoning markets for green technologies, such as renewables and electric vehicles, is transforming demand for Lithium, Cobalt, Rare Earths and Graphite, as well as larger and more diversified raw materials industries, such as Copper, Aluminium and Nickel. However, at the same time, investment is also required to reduce carbon emissions directly from raw materials production and processing.

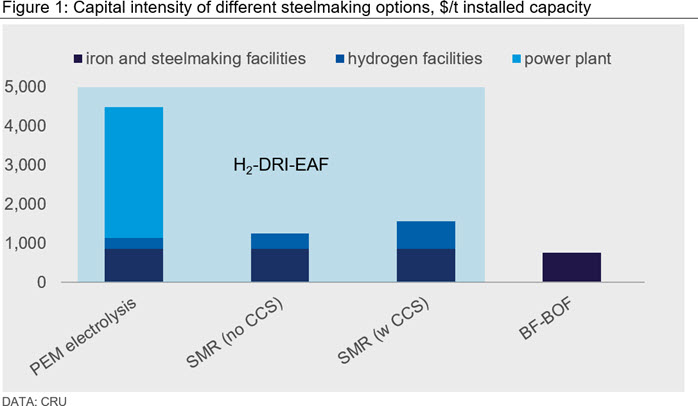

Some progress on sector decarbonisation is already evident. A recent study by CRU Consulting, for example, found that a sample of major Chilean copper mines have secured contracts to reduce emissions from power by 75 percent by 2025. However, in the case of the steel industry, for example, the capital costs associated with deploying new low carbon production technologies are currently prohibitive: CRU estimate that hydrogen-based reductants or Carbon Capture and Storage (CCS) could require 2–6 fold the investment per tonne of steel than traditional fossil-based production (see Figure 1).

The capital markets have a critical role to play in enabling energy transition

Institutional investors and asset managers have a central role to play – in partnership with management teams, suppliers and customers – in financing well designed and executed decarbonisation investment strategies by mining, metals and fertilizer producers. Such investments will be critical to the future supply of raw materials required to sustain rising living standards as well as enabling the broader decarbonisation of the economy. Importantly, adjusting the scale and composition of sector investment is also required to mitigate investment risks from associated policy and technological change (see here for a discussion of stranded asset risks in steel and aluminium industries).

This issue has shot up the agenda for institutional investors, asset managers and lenders alike in response to rapidly shifting expectations on the part of consumers and regulators. Many banks, for example, have introduced new debt instruments, such as ‘Green Bonds’, designed to lower the cost of capital for green investments. The investment community is also seeking to promote greater alignment with the Paris Agreement. In January, BlackRock – the world’s largest asset manager – announced sweeping changes to its investment approach in light of the climate challenge. In October of 2020, HSBC announced a commitment to enabling net zero carbon emissions across its entire customer base by 2050.

Against this backdrop of high-profile, and ever more prevalent, strategic commitments to greening major loan and equity portfolios, it is also important to recognise that industry players are currently moving at different speeds, with some major investors continuing to limit the role of climate change in shaping investment decisions. This renders tracking and monitoring of progress against such commitments particularly important, both to help early adopters drive strategic decision-making across their organisations, but also to facilitate greater differentiation between asset managers in the eyes of investors.

Significant obstacles exist to Paris-aligned capital allocation

The practical obstacles to more ‘sustainable’ capital allocation should not be underestimated. The asset management industry is itself under massive structural pressures to reduce management fees and operating costs, resulting in a large-scale shift towards passive investment structures. Firms that align their business models to the energy transition are likely to achieve progressively higher index weightings over time, and thus access steadily more capital. However, this shift may also limit the potential for asset managers to proactively direct financing to firms and investments that develop and adopt clean technologies.

Even where funds are actively managed, substantial institutional and informational barriers persist. Fund managers face day to day pressures to grow assets under management, commonly linked to short term financial performance, in a way which may conflict with longer-term goals such as investing for a more sustainable future. Perhaps more fundamentally, many investment managers are under pressure to divest from the most carbon intensive sectors and firms. The cost of divestment in terms of the potential loss of strategic influence over the investment strategies of major corporates is well known and risks limiting access to capital for sustaining and decarbonising economically critical industrial sectors.

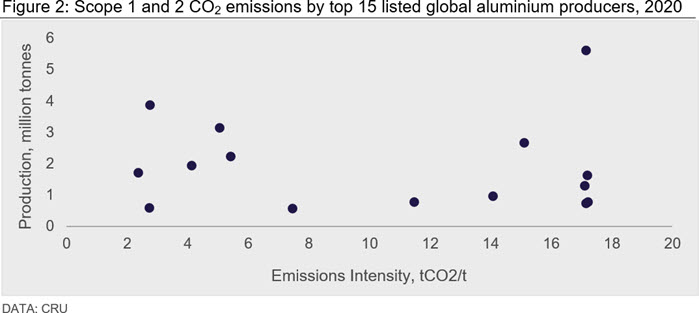

To date, carbon disclosure issues have focused principally on the energy sector. But these issues present quite differently in the mining, metals and fertilizer industries; in particular, there is commonly much wider divergence of emissions intensities within a given industry or segment. Take aluminium smelting as a case in point, where there is roughly 15 tonnes of CO2 difference in the volume of emissions per tonne of metal produced between the most and the least carbon-intensive producers contained within CRU’s aluminium cost model (see Figure 2). This means that institutional investors and asset managers have greater potential to mitigate carbon emissions associated with their industrial portfolios, thereby also strengthening decarbonisation incentives in order to ensure sufficient access to low-cost capital.

Robust benchmarking is a key enabler in climate-aligned portfolios

Robust emissions benchmarking is, thus, likely to be a key enabler of a structural financing shift, by tracking the allocation of capital towards the least carbon-intensive industrial producers and investments. The importance of this goal was clearly recognised by major banks – including BBVA, BNP Paribas, ING, Standard Chartered and Société Générale – which agreed, as part of the ‘Katowice Commitment’ in 2018, to measure the climate alignment of their lending portfolio. However, this has proved challenging to achieve in practice often because self-reported emissions numbers, even if accurately measured, are not always reported on a like-for-like basis; nor are they provided at a sufficient level of granularity to help with investment decisions. These are some of the challenges that our emissions analysis and resources – including the Emissions Analysis Tool – aim to overcome.

A debate is rapidly emerging regarding the relative emissions intensity of different asset and portfolio managers and their consistency with both science-based targets and stated institutional objectives. CRU do not take a view on the merits or particularities of incorporating strategic goals relating to climate change into investment or portfolio allocation policies. However, we do recognise that given this emerging priority among investors, governments and civil society, there is a critical need for robust, comparable and transparent emissions reporting analysis on this important topic, which takes proper account of the specificities of key carbon-intensive sectors such as mining, metals and fertilizers.

Accounting for carbon in major industrial portfolios

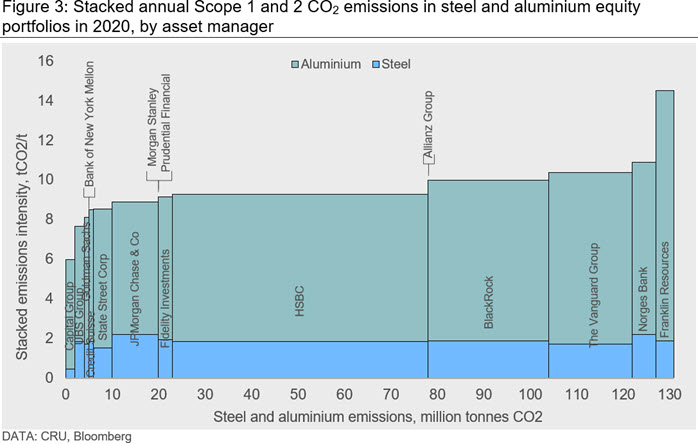

To this end, CRU Consulting have estimated the CO2 emissions associated with the equity portfolios of a selection of major asset managers in the steel and aluminium sectors. This is undertaken by calculating the level and intensity of carbon emissions for the 15 largest listed steel and aluminium producers recorded within CRU’s steel and aluminium cost models. Production and emissions covered by CRU’s Steel and Aluminium Cost Models are attributed (on an equity basis) to individual fund holders managed by a selection of leading asset management firms (data sourced from Bloomberg). These metrics are then aggregated by asset management firm, differentiating according to whether the funds are actively or passively managed.

Figure 3 below, for example, charts the level and intensity (i.e. as a ratio of total production) of CO2 associated with these portfolios. It reveals a heavy concentration of emissions among particular portfolios: for example, the top 3 asset managers, namely HSBC, BlackRock and Vanguard, in terms of total emissions account for ~100 million tonnes annually, equivalent to around three quarters of the sample. However, probing more deeply, we find a substantial difference in the carbon intensity of individual segments of these portfolios. For example, the emissions intensity of State Street and Capital’s steel holdings are lower than the rest of the sample. By contrast, aluminium stock holdings of Franklin Resources are significantly higher than others’ major funds.

Can we identify ‘green shoots’ in capital allocation?

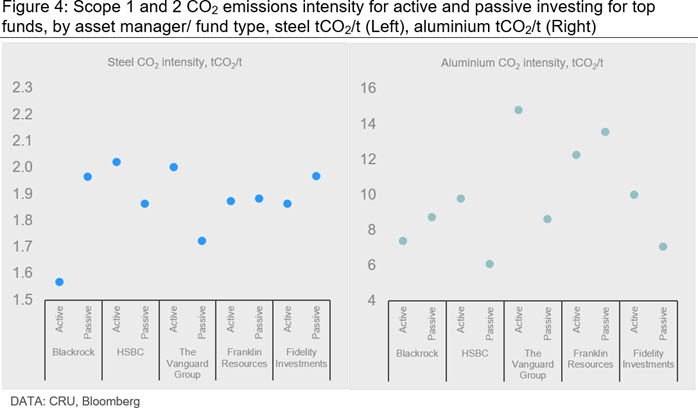

Evaluating capital allocation in such large and diverse portfolios is complex. One possible indicator of behavioural change among financial investors, in response to emerging strategic priorities relating to climate change mitigation, is to explore differences in emissions associated with active versus passively managed funds. Although recognising the broad range of likely factors driving such active investment decisions, and thus the need to interpret any results with care, this approach can nonetheless potentially cast preliminary insights on whether capital is being proactively channelled towards low emissions sectors and firms as part of an inevitably long-term process of portfolio alignment.

Figure 4, for example, compares the emissions intensity of steel and aluminium portfolios for a subsample of 5 major asset managers by fund type, distinguishing between those that are actively managed and those that passively track particular indices. Overall, across the subsample, we find quite limited evidence that corporates with lower average carbon intensity of production have a greater propensity to attract capital from actively managed funds. In the case of the steel sector, for example, only BlackRock and Fidelity, have actively managed funds which have lower carbon intensities compared to their passive counterparts. Looking at the aluminium sector, the results are once again mixed: only BlackRock and Franklin Resources have lower carbon intensities in their actively managed funds.

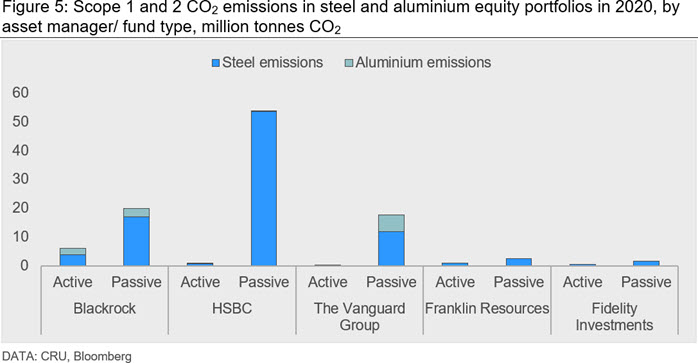

Figure 5 shows total, as opposed to intensity-based, emissions from Steel and Aluminium sector holdings for these asset managers. We see a heavy concentration of emissions in Steel, particularly among passive funds (reflecting its typically larger index weighting). As noted above, emissions are concentrated in BlackRock, HSBC and Vanguard, reflecting their heavy aluminium and steel sector exposures. However, for a fuller perspective, it would be important to adjust for the scale of these funds in order to ascertain whether actively managed funds have the tendency to direct capital away from emissions intensive industries.

Such a “normalisation” for funds of different sizes and structures is a rather involved exercise, which largely lies outside the scope of this Insight. By way of illustration, however, based on a highly aggregated analysis of assets under management by fund type, it is perhaps possible to suggest that, in the case of BlackRock, for example – whose passive holdings are roughly 2.5–3.0 times greater than actively managed assets – that the latter are not systematically unweighted in the steel and aluminium sectors relative to index funds.

Towards more robust benchmarking of climate-aligned investment portfolios

Expectations on asset managers and institutional investors to achieve climate-aligned portfolios are high and rising, not least given pressures from governments, civil society and their customers. Robust emissions benchmarking is a key enabler of this structural shift in capital allocation, but is often challenging because self-reported emissions numbers, even if accurately measured, are not always reported on a like-for-like basis; nor are they at a sufficient level of granularity to help with investment decisions. Yet another challenge CRU's emissions analysis services and new Emissions Analysis Tool overcome by providing verifiable, standardised and readily available data on an intuitive interactive platform. Further support from CRU Consulting allows for robust benchmarking of the equity and debt portfolios of major asset managers and banks across the metals, mining and fertilizer sectors.

In the case of the equity holdings of a sample of 5 major investment funds in the top 15 listed steel and aluminium producers, CRU Consulting find that emissions are heavily concentrated in the portfolios of a subset of asset managers, such as BlackRock, HSBC and Vanguard, reflecting their heavy equity exposure to aluminium and, particularly, steel producers. We also find that corporates with lower average carbon intensity of production do not (yet) clearly have a greater propensity to attract capital from actively managed funds. However, a fuller assessment would ultimately be required to understand whether actively managed funds are systematically less heavily weighted in these sectors, and whether the level of emissions associated with these exposures is having a bearing on these capital allocation decisions.

How will you be impacted? To discuss any of these issues further, or to understand the potential implications for your business, contact us below.

Explore this topic with CRU-

Caroline Alglave

Senior Analyst London -

Francisco Acuna

Principal Consultant Santiago -

Sam Adham

Head of Battery Materials London -

Jessica Alves

Consultant Sydney -

Joan Arratia

Base Metals Emissions Lead London