Author Damodharan Navaneethakrishnan

Regional Director - South Asia View profile

Co-author Alex Laugharne

Principal Consultant View profile

Co-author Rebecca Gordon

Chief Executive Officer, CRU Consulting View profile

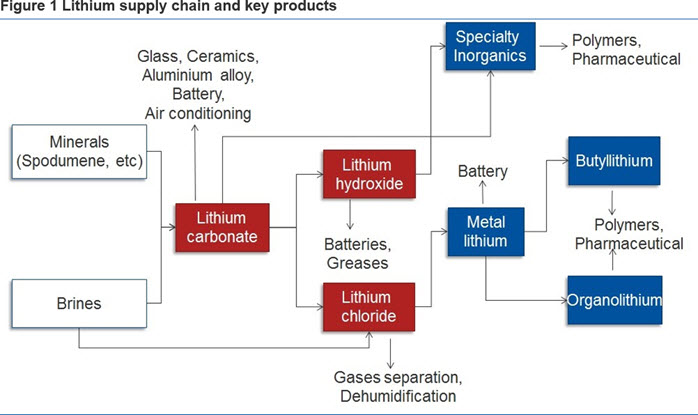

Historically, lithium carbonate has been, by some distance, the primary product form used for both industrial lithium applications and manufacturing Lithium Ion Batteries (LIBs). However, the dramatic growth in the LIB segment in recent years has led to changes in purity requirements for lithium carbonate, as well as expanded demand for other lithium chemicals, most notably lithium hydroxide. China’s importance in the lithium market is increasing day-by-day and this insight looks at the current challenges facing the sector as it strives to follow the recent policy changes. High-level flowchart of lithium supply chain is given below:

Source: CRU

Impact of recent Chinese NEV policy

The key element of the new Chinese policy entails a quota for the production of NEVs, which includes Battery Electric Vehicles (BEVs), Plug in Hybrid Vehicles (PHEVs) and Fuel-Cell Vehicles (FCEVs). The quota will be enforced through a credit score system, where automakers will earn credits for producing NEVs. In 2019, local or foreign companies producing more than 30,000 cars annually must earn NEV credits equal to 10% of the vehicles they produce; increasing to 12% by 2020. Automakers failing to hit the targets will be compelled to buy credits from others that have excess credits, or be subject to penalties – CRU believes that these penalties will be sufficiently stringent to drive automakers to largely comply with the quota system.

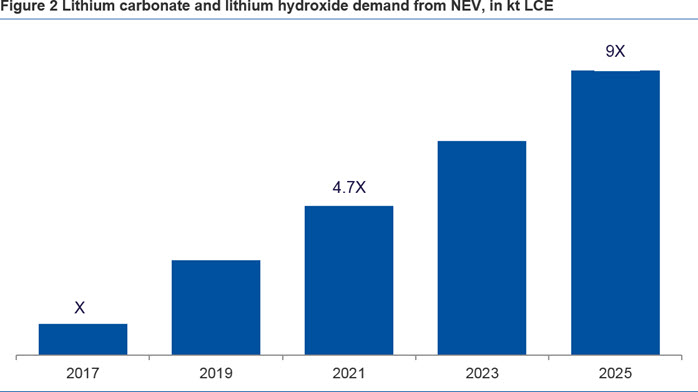

The policy described above is expected to be a major factor in driving NEV production and sales in China, and we believe that it will drive growth in PHEVs and BEVs ahead of Hybrid Electric Vehicles (HEVs). It is expected to translate into a fourfold increase in lithium demand from the NEV sector in the medium term. This in turn will have a significant impact on demand for battery grade lithium carbonate and lithium hydroxide. The combined demand for battery grade lithium carbonate and lithium hydroxide from NEV is given below:

Source: CRU

Will supply be able to catch up with demand?

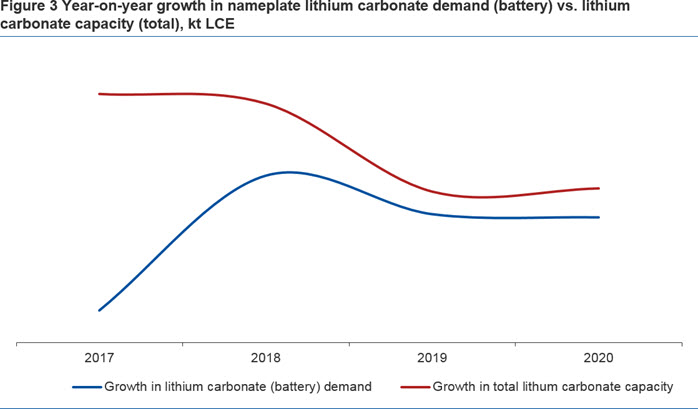

Lithium carbonate processing capacity is currently located in five countries: China, Argentina, Chile, USA and South Korea. China accounted for 40% of global carbonate production capacity, and will see this share rising to 60% in 2020. In the chart below, we compare the year-on-year (y/y) volume growth in battery grade lithium carbonate applications against additions to total lithium carbonate processing capacity. Overall, we expect a convergence in the annual growth in lithium carbonate capacity and battery grade lithium carbonate demand from 2019, as demand and supply move more closely in line with each other.

Source: CRU

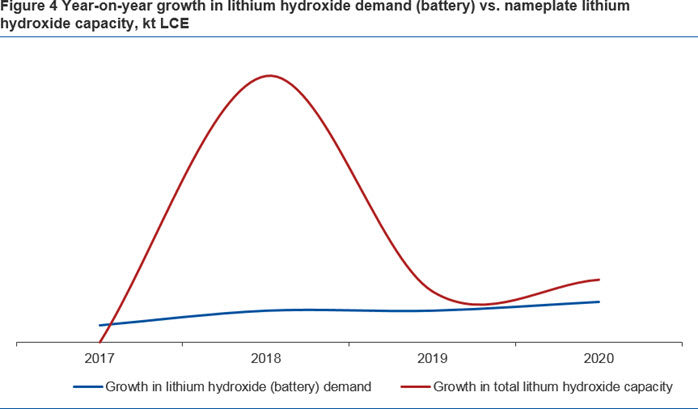

Lithium hydroxide processing capacity is expected in seven countries by 2020, including China, Australia, Argentina, Japan, USA and Canada. Almost every major lithium chemical producer has announced a timeframe to expand lithium hydroxide capacity in anticipation of demand growth for NEVs containing higher nickel chemistry batteries which require lithium hydroxide instead of lithium carbonate. While the capacity growth in 2018 far outstrips annual demand in that year alone, we believe this is to fill a lithium hydroxide deficit that could have emerged as early as 2016 for parts of the market, as well as being constructed in anticipation of future demand growth in 2019 and beyond. Going forward we expect continued investment in lithium hydroxide capacity.

Source: CRU

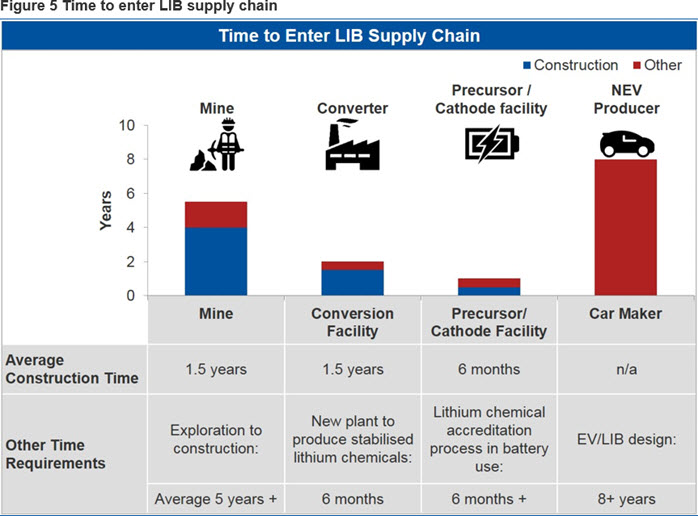

Development time mismatches lead to bottlenecks

There are a variety of potential bottlenecks along the lithium supply chain from raw materials to battery manufacturing and eventual end use in NEVs or other applications. Evidence for this comes from the supply deficit that has emerged and caused lithium hydroxide prices to increase sharply. Lead times and potential bottlenecks at each stage are described below:

- Spodumene mine: it takes on average more than 5 years for a lithium deposit to go from exploration (JORC estimate) to construction; and a further 16 months to complete construction and commence production. Once construction has been completed commissioning can take 6 months or more to achieve consistent, high quality production.

- Lithium conversion facility: It takes over 6 months to be able to optimise production of battery grade lithium chemicals from a new conversion plant, and a further 6-8 months to accredit this product for use in the battery value chain in China; and as much as 14-18 months outside of China.

- Precursor manufacturing: The construction time for a precursor and cathode facility is only 6 months, as such they have greater flexibility to respond to changing demand.

Source: CRU

Typically, the NEV producers place orders for battery cells a year in advance and demand then trickles down to the cathode and lithium chemicals manufacturers. This is then the trigger for the upstream sectors of the supply chain to securing funding and commission capacity expansions.

While the time requirements for capacity building are not too mismatched, it is the time to reach the required product quality and get the products accredited in the supply chain that leads to mismatches in capacity during times of aggressive capacity ramp up and supports prices and premia even when at first sight mine capacity is sufficient to meet demand.

In conclusion, the supply chain for lithium is considerably more technically challenging than many other traded commodities CRU analyses. The number of completely new participants and unproven mines adds complexity. The interrelationship between the processing steps and the ongoing technological difficulties of processing variable raw material sources with their diverse chemical compositions is leading to delays in delivering quality product to the end consumers.

It is important to consider all stages of the supply chain to identify potential bottlenecks as both miners and NEV manufacturers strive to be able to meet policy mandated production targets.

Our team in China tracks development in NEV closely and its implications on lithium market. We believe enforcement of NEV policy will be the predominant factor to determine the lithium demand for next three to five-years timeframe. In addition, timely completion of processing facilities to match the growing demand will ease pressure on battery grade lithium compound supply. NEV producers have to be cognisant on potential bottlenecks in their supply chain and the risk to price volatility that this represents.

Author Damodharan Navaneethakrishnan

Regional Director - South Asia View profile

Co-author Alex Laugharne

Principal Consultant View profile

Co-author Rebecca Gordon

Chief Executive Officer, CRU Consulting View profileThe Latest from CRU

Decarbonisation will reshape global steel trade flow

CRU’s Steel Long Term Market Outlook presents comprehensive analysis of global steel trade flows until 2050. Decarbonisation will play a significant role in redefining...