Author Paul Butterworth

Research Manager View profile

In this series of Special Features we have explored the structural changes in the Chinese steel sector brought about by the central government’s supply-side reform drive, the impact of these changes on steel industry profitability and production, in China and elsewhere, and on exports of steel and the price of these exports. In this, the fifth and final Special Feature in the series, we turn our attention upstream to explore the impact of supply-side reform on bulk raw materials demand and prices. Our analysis shows that, whilst the restructuring of the Chinese steel sector will lift profitability of the steel sector itself, both in China and elsewhere, it will have little impact on average prices of raw materials. However, overall, mills are likely to favour higher-grade ore and coal to support higher operating rates, but this relationship is weak and other factors can have a more significant influence on grade premia.

Steel sector profitability and raw material prices

When bulk raw material prices move significantly, up or down, we are often asked “how will this movement impact steel industry profitability?” Equally, when the steel industry is performing well – that is, when operating rates and steel prices are high and profitability good – there tends to be an expectation that this should give greater scope to steelmakers to pay more, often willingly, for raw materials. However, our position is that, beyond short-term, sentiment driven impacts, bulk raw material prices and steel industry profitability are not connected, at least not directly. Even for scrap, which was discussed more fully in the previous Special Features in this series, where there is a much closer relationship between scrap price and steel price, there is not necessarily a direct correlation between profitability of the steel sector and input costs. This note sets out our reasoning for this view.

Based on our understanding of the cost structure of steelmakers globally, coupled with weekly price assessments of the key steelmaking raw materials, CRU is able to track the cost of producing steel on a weekly and monthly basis.

Paul Butterworth Research Manager, Steel Raw Materials and Steel Costs

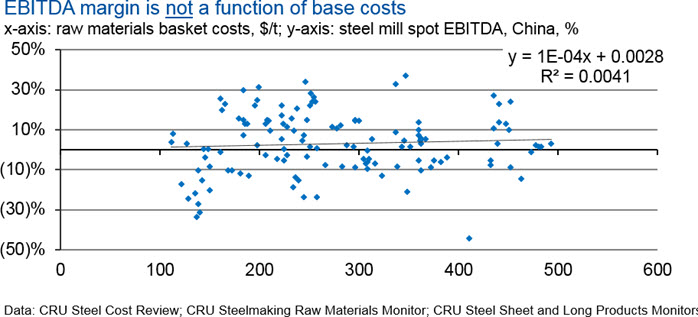

Based on our understanding of the cost structure of steelmakers globally, coupled with weekly price assessments of the key steelmaking raw materials, CRU is able to track the cost of producing steel on a weekly and monthly basis. Furthermore, our comprehensive coverage of steel prices allows us to track the profitability of steelmakers in the key producing regions. Using the Chinese steel sector as a basis, the following graph sets out the relationship between steel mill profitability and raw material prices, the latter given by the cost of the ‘raw materials basket’ required to produce 1 tonne of steel.

The statistics for the above data indicate that there is no relationship between raw material prices and steel mill profitability (i.e. the gradient of the best fit line is close to zero/correlation coefficient is very low). This graph shows that raw material prices can be high or low, whilst profitability in the steel sector can also be high or low. That is, raw material prices have little relevance to the performance of the steel sector and vice versa. But why is this?

Broadly speaking, all steelmakers are exposed to the same raw material markets. Some, individual steel mills may, by virtue of location, have access to lower priced raw materials, but are likely to face the same market movements, and some mills have captive raw materials supply, but this is not common – and the Chinese steel sector is no different in this respect. Thus, as raw material prices move up and down, this lifts or lowers the costs of the entire steelmaking population, but says nothing about the strength of the steel sector itself. That is, the Chinese steel sector is performing well today simply because the underlying supply/demand dynamics of the sector are favourable, as a result of supply-side reform, but demand for steel and, therefore, raw materials has not changed, so the prices for raw materials should not be affected.

Having said the above, there will be an indirect link between raw material prices and steel sector profitability that, arguably, is perceptible in the above graph (i.e. the very lowest profitabilities occur when raw material prices are also at their lowest). That is, a well-performing steel market is more typically associated with periods of high steel demand (i.e. rather than supply constraints, as today) and high steel demand translates into high demand for raw materials. That is, at the peak of the steel cycle, all other things being equal, both steel prices and raw material prices will be elevated – one does not affect the other directly, both are the result of high steel demand. However, as recent history has shown, the specific supply/demand characteristics of each sector are far more important in determining the prices achieved at different points in the steel cycle.

A further conclusion of the above analysis is that the cycles of the bulk raw materials and steel sectors are not aligned. If they were, there would be a much stronger correlation between steel sector profitability and raw materials prices but, again, both would be driven primarily by steel demand conditions.

Short-term factors

Although, at a fundamental level, supply/demand dynamics in the raw materials sectors will have the much greater influence on raw material prices than profitability in the steel sector, short-term factors can be important, as we have seen in recent months.

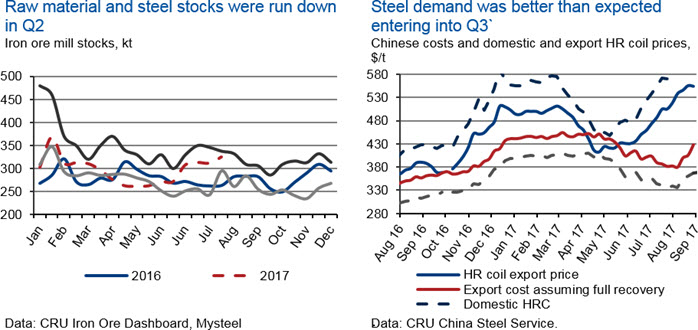

The left-hand graph below sets out domestic and export HR coil prices and steelmaking costs in China over the last year. This shows that, in March and April this year, steel prices fell rapidly and export prices were close to variable costs for a short period. At this point, the market generally was uncertain about the future and, as the right-hand graph shows; steelmakers began to run down raw material stocks, but also started to plan for major maintenance. We also saw steel inventories pull back, as the market prepared for a period of uncertainty, and expectations were that 2017 Q3 was not going to be strong. However, in June, interest rates were reduced and this provided a fillip to the economy and steel prices began to lift and were driven to very high levels by constrained supply and capacity utilisation was pushed to a high level. Steel makers were not prepared for this and, after maximising scrap use in the process, mills re-entered the raw materials markets to restock and take advantage of the high steel prices.

Restocking demand from June onwards lifted raw material prices, thus, in the short-term, elevated profitability in the steel sector did, essentially, drive raw material prices upwards (n.b. admittedly, prices were also helped by a poor export performance by the iron ore majors, as well as constrained supply of coal both inside and outside China). But this price effect was more a function of the very rapid transition in the Chinese steel sector over the previous months, as a result of a very successful supply side reform, and of demand exceeding expectations. In our view, neither of these situations was likely to last for long and it has been our expectation that steel demand would pull back seasonally in Q4, steel mills that were now well-stocked would withdraw from the raw materials markets, raw material supply would continue to expand and that prices would fall, a situation that is playing out currently.

Impact of Chinese supply-side reform on quality premia

So, supply-side reform is not expected to have an impact on the average level of raw material prices, but they can impact quality premia. In recent weeks, the premium for higher-grade iron ore has been at a record level, with the price of 62% Fe material more than 50% above that for 58% Fe material, when a more typical level might be 18% above at today’s iron ore price. A similar, but less pronounced, situation exists in the coking coal sector, with premium hard coking coal prices currently above their steady-state value over standard hard coking coal prices. But to what degree is structural reform in the Chinese steel sector responsible for this?

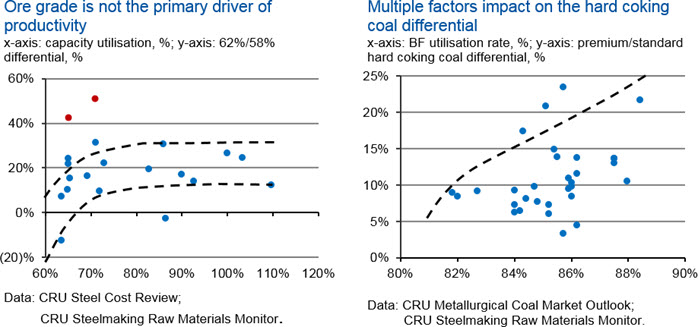

The graphs below show the relationship or otherwise between capacity utilisation in the Chinese steel sector and quality premia in the coal and iron ore sectors.

The left-hand graph sets out the 62%/58% differential versus capacity utilisation in the steel sector and, in fact, suggests that there is no clear relationship between the two – the statistics for the data certainly don’t suggest a significant correlation. That is, higher operating rates and, by default, higher productivities are not necessarily a key driver of the grade premium, which is not current consensus. In fact, the red outliers in the left-hand graph show that high ore grade premia can occur at relatively low capacity utilisation levels but, interestingly, both of these data points relate conditions immediately prior to rapid increases in capacity utilisation (n.b. one also occurs during the ramp up of output at FMG). This suggests that, when the steel market is at a turning point and operating rates are just beginning to lift, steelmakers appear more willing to pay for high-grade material but, subsequently, the premium settles back down to a high, but more normal level. This is likely to be indicative of mills locking in high-grade supply in the early days of a market upturn, perhaps as a de-risking measure, but then returning to a more normal procurement strategy once conditions are more certain.

The second graph shows the price differential between premium and standard hard coking coal under different operating rates and, again, indicates no significant relationship between the two variables. The manually drawn line does suggest that the upper limit to the premium lifts with capacity utilisation, but the spread of data below this line implies that other variables can impact on this value, although a general upwards trend can be determined. Having said this, it is noteworthy that the premium/standard coking coal premium remains below 10% at utilisation rates below 84% and above 10% at rates of 86% and higher, suggesting a threshold operating level at which procurement decisions switch.

So, the above graphs suggest that there is a relationship between operating rates and grade premia, but this relationship is not strong, either in coal or iron ore, and other factors will be important in the pricing decision. In other words, there is more than one way to achieve higher productivities and each mill will make its choice based on the best economic and technically feasible alternative before it.

Conclusions

Whilst the restructuring of the Chinese steel sector will lift profitability of the steel sector itself, both in China and elsewhere, it will have little impact on average prices of raw materials. Mills, however, are likely to favour higher-grade ore and coal to support higher operating rates, but this relationship is weak and other factors can have a more significant influence on grade premia.

Author Paul Butterworth

Research Manager View profileThe Latest from CRU

Decarbonisation will reshape global steel trade flow

CRU’s Steel Long Term Market Outlook presents comprehensive analysis of global steel trade flows until 2050. Decarbonisation will play a significant role in redefining...