We have investigated this intriguing question using consumption data from our HV and EHV Cables Market Outlook, and the latest information on subsea cable capacity planned and under construction from 2023 out to 2030. We have divided the data into MV & HV subsea cables and EHV subsea cables.

MV & HV subsea cable refers to voltages of usually around 33 kV for array cables for MV and >37.5 kV and up to ≤245 kV for HV, with most of the units using catenary continuous vulcanisation (CCV) technology. EHV cable in this report is from >245kV onwards and production at these plants is usually via vertical continuous vulcanisation (VCV) technology.

It is common to install two VCV lines per tower, while certain towers at the newest units in China can accommodate up to eight VCV lines per tower, which can increase EHV cable production at each plant substantially. However, it has to be noted that in China some producers frequently use VCV towers designed for subsea EHV cable production to make HV cable, both for subsea and land use.

The analysis below is on the basis that all subsea HV & EHV capacity expansions and new plant announcements will come to fruition. This includes new units announced by XLCC in Port Talbot, Wales, Rise Light & Power and Delaware River Partners (DRP) in New York, which might not be built due to various uncertainties.

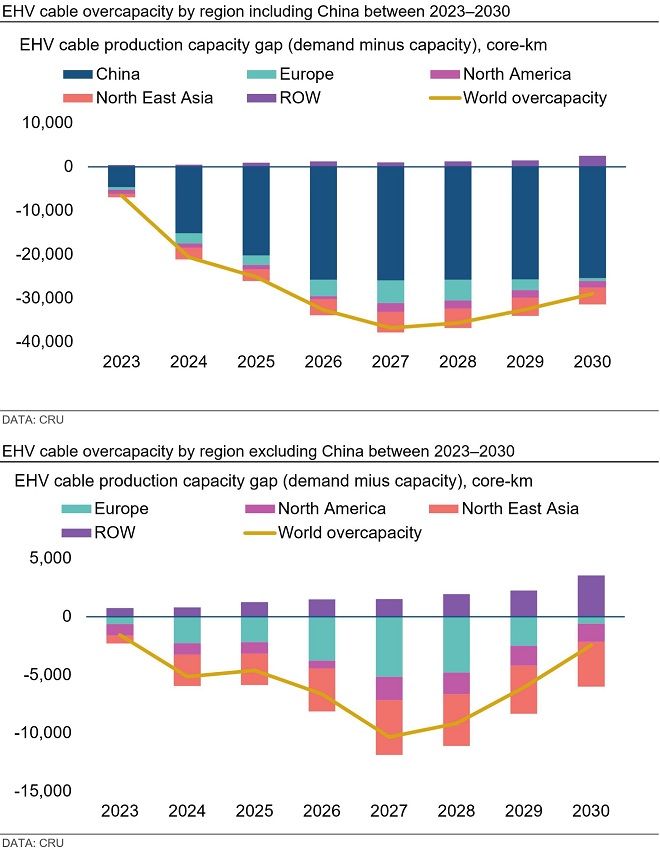

EHV subsea cable capacity will notably expand from 2024 to 2026

What we have discovered is that globally EHV subsea cable overcapacity will peak in 2027 and remain high until 2030. The main reason for this is that China is adding a huge amount of capacity between 2024 and 2026, while domestic demand over that period is expected to be lacklustre but pick up again from 2027 onward. If we were to remove China from the picture, global overcapacity would still peak in 2027, but reduce substantially toward 2030.

Overcapacity will reach new highs in 2027 for Europe, North America and Northeast Asia as producers complete expansions and new builds. In Europe, overcapacity will normalise towards 2030 mainly because a significant amount of capacity will come onstream in 2024, 2026 and 2027, but will be met with a surge of demand between 2026 and 2030.

The situation is similar in North America, where overcapacity in 2027 will be offset to some degree by a surge of demand, particularly from offshore wind; while Northeast Asia will see a large increase in capacity between 2024–2027, which will be offset by strong demand from 2027 onwards.

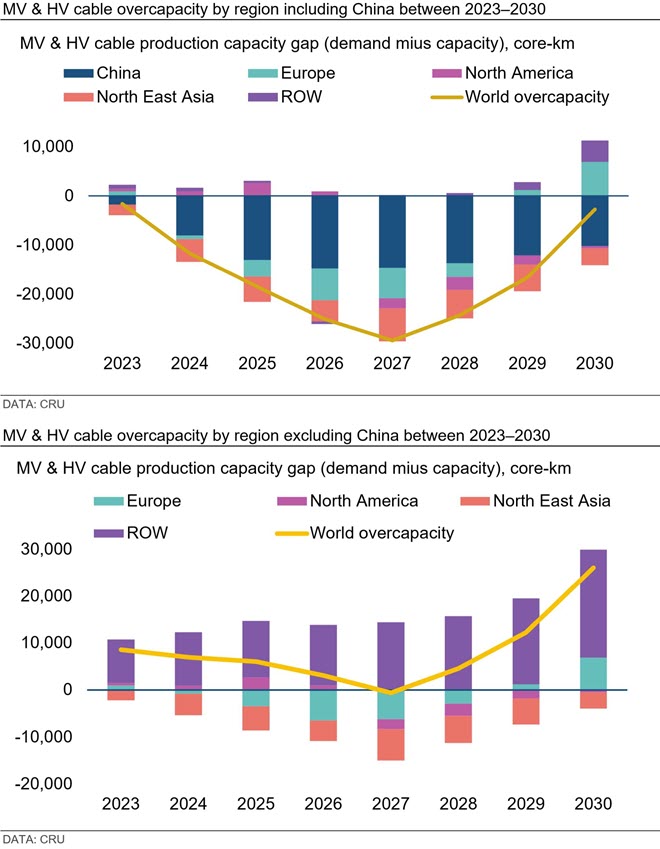

China tips MV & HV cable into overcapacity from 2024

For MV & HV cable, global overcapacity will also peak in 2027, driven predominantly by China, but also Northeast Asia. However, from 2028 overcapacity will drop off substantially, nearing 2023 levels. If we remove China from the picture, the situation could not be more different, with a trivial amount of overcapacity in 2027, mainly due to startups in Europe, North America and Northeast Asia, which will be significantly reversed the following year.

With or without China, what is noticeable is that in 2029 and 2030, Europe and the Rest of World (ROW) region will be short of cable. Demand in the ROW region during that period will come predominately from India and Southeast Asia, Australasia and Africa.

Are producers’ expansion and new build strategies correct?

When we examine where capacity is being added and which producers are involved, it becomes evident that the correct strategy is being implemented. Notably, Northeast Asian producers such as South Korea’s LS Cable & System and Japan’s Sumitomo Electric Industries (SEI) have recently announced plans to establish EHV subsea cable plants in the UK. These plants will primarily produce cables for major projects that require EHV DC technology, connecting the UK’s islands or other European countries like Iceland. China’s Ningbo Orient has also taken the opportunity to invest in the UK by signing a technology agreement with HV & EHV cable industry disruptor XLCC. The output from this unit is linked to the UK to Morocco EHV DC interconnector.

As we have seen, the Northeast Asia and Asia Pacific region will be well supplied by Chinese, South Korean and Japanese producers, but Europe will require both HV and EHV cables – particularly towards the end of the forecast horizon – and this is when the plants from SEI (2026), LS Cable (2027) and XLCC (2028–30) will come onstream according to CRU’s estimates.

Likewise in the US, new capacity is needed to cater to the burgeoning offshore wind industry, as seen by recent announcements by LS Cable to set up a unit there. Similarly, there are plans by Greece’s Hellenic Cables for an array cable unit at Wagner’s Point, Maryland; and the construction of a HV and EHV cable unit at Brayton Point, Massachusetts by Italy’s Prysmian. During the latter part of our forecast period, we anticipate overcapacity in North America to be absorbed by demand from South America (part of the RoW region in the charts), where offshore wind projects are under consideration in Brazil and Colombia.

Since Europe will be out of the overcapacity phase for MV & HV subsea cable from 2029 and will see reduced overcapacity for EHV subsea cable also in 2029, it is likely that the trend for Asian producers offering cables into Europe will increase. LS Cable, ZTT, Ningbo Orient and SEI for instance are increasingly involved in European subsea cable projects, with many of these won over 2023. LS Cable has been the most prolific with the most recent award being by Belgium’s Elia to connect the manmade Port Elisabeth Island with an offshore wind farm. Ningbo Orient Cables was also awarded the contract to supply 33 kV cables for the UK’s Pentland Firth interconnector and 275 kV export cables; as well as 66 kV array cables for Poland’s Baltica 2 OWF with ZTT.

How about China?

The overcapacity for both EHV and MV & HV subsea cables in China cannot be ignored. However, in China the picture might be somewhat blurred as some producers are using subsea cable lines to make land cables. Additionally, it is understood that authorities have almost stopped approving new HV and EHV land cable plants. CRU anticipates this could make it likely for producers to eventually use the new subsea HV and EHV cable plants to make land cables due to limited domestic demand, and the subsea cable overcapacity situation. It is likely that in future there will be consolidation among Chinese producers and streamlining of production.

In Europe and the US, the need for governments to fulfil their environmental and energy security targets and obligations, while at the same time ensuring low energy prices for consumers, is likely to make it difficult for locally based producers to fully control the market. However, the high level of technological expertise for making EHV cables, particularly for interconnectors, could result in the tightening of investment screening mechanisms and the blocking of foreign takeovers of European or US companies.

Emerging markets could also provide a wildcard for future offshore wind and interconnector demand. There are many that have yet to fully develop, particularly in Southeast Asia, South Asia, Australasia and South America; and these could potentially provide valuable opportunities for cable producers in countries with overcapacity.

Feel free to contact us if you would like to discuss these topics further or subscribe to the HV and EHV Cables Market Outlook, soon to be renamed Electricity Transmission Market Outlook, which forecasts HV & EHV cable consumption and production up to 2030.

Explore this topic with CRU