Increasingly, all commodity markets will be shaped by sustainability. Markets, policy, clean technologies, sustainability and the energy transition will become ever more interlinked and complex. In part two of our top 10 sustainability calls for commodity markets in 2024, we focus on the following five calls. You can read part one of this insight here.

Author Charlie Durant

Research Manager View profile

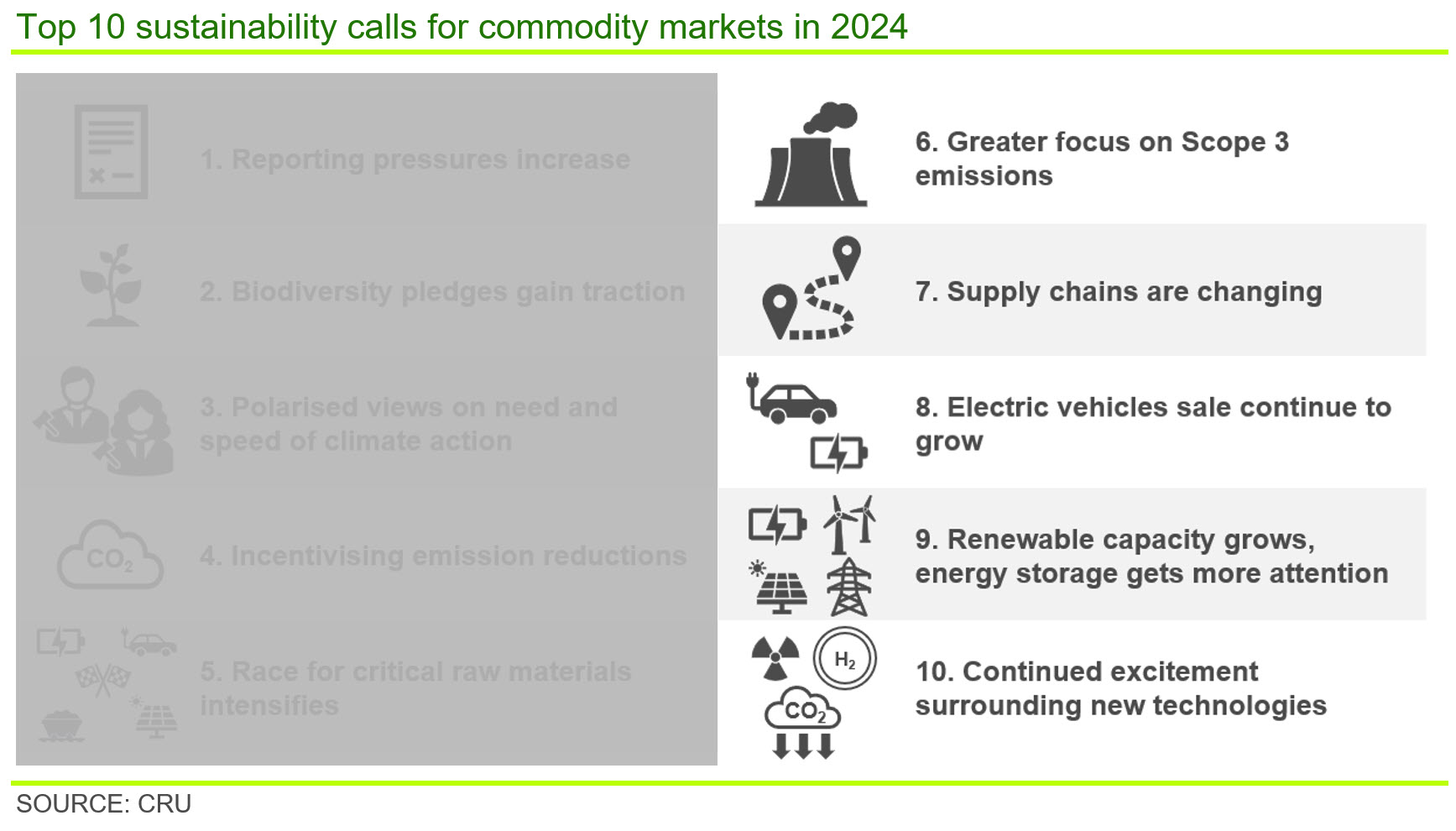

6. Greater focus on Scope 3 emissions

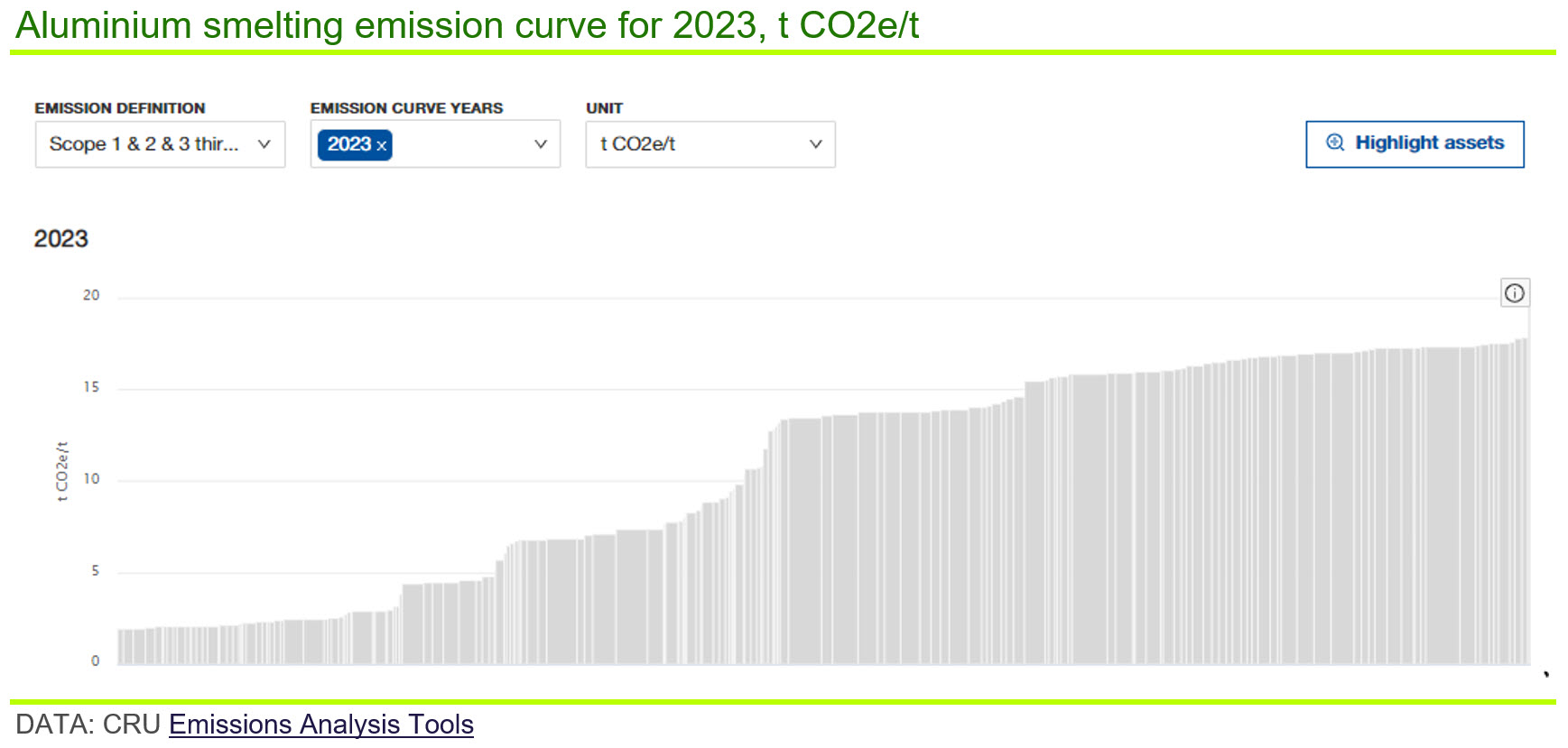

Indirect emissions through the value chain, or Scope 3 emissions, will be the subject of increased attention starting in 2024. This will happen on a national scale through trade legislation, stricter laws and regulations, including more stringent disclosure requirements. The first stage in reducing Scope 3 emissions will be their disclosure.

Corporates will need to prioritise supply chain collaborations and pay more attention to how their goods and services are utilised in 2024. Financial institutions will also be paying more attention to Scope 3. As regulations tighten, portfolio managers across many jurisdictions will need to obtain additional data on emissions.

CRU has seen a huge increase in interest from consumers, producers and financials looking to get a complete value chain understanding of emissions. More companies are looking to map ‘cradle to gate’ emissions and make greener sourcing decisions to reduce their Scope 3 exposure.

See CRU’s Emissions Analysis Tools for more information.

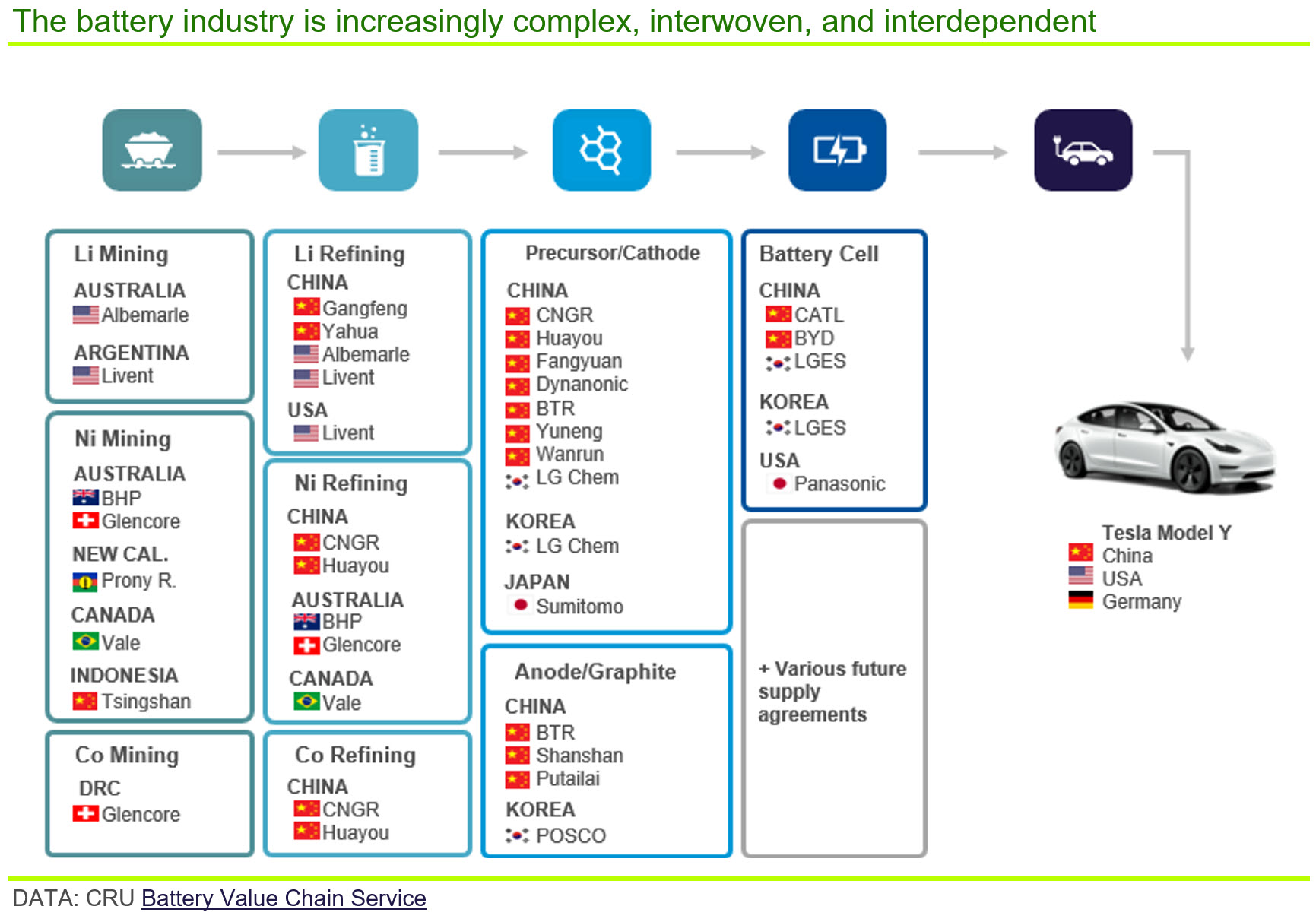

7. Supply chains are changing

Supply chains are in a period of significant change, with regionalisation growing as a trend. As supply chain sustainability and resilience come under greater scrutiny, there is likely to be a shift towards greater self-sufficiency, diversification and reshoring. This trend could create new opportunities for local suppliers and manufacturers but may also lead to higher costs and reduced efficiency.

Chinese companies are increasingly intertwined in the complex global battery supply chain as they continue to expand production at home and overseas. Western policymakers are attempting to onshore a battery supply chain and this is already initiating a shift in regional supply and demand. Despite this, the efforts to exclude Chinese content will incur an overwhelming cost at a time when cost is the most important metric for battery producers and end users.

Due to a multispeed transition, we are seeing a greater interaction of climate and trade policy. The most noticeable development over the last year was in the EU, which brought in the first phase of the Carbon Border Adjustment Mechanism (CBAM), designed to address carbon leakage and incentivise policymakers elsewhere to introduce their own carbon pricing schemes. Or indeed their own version of CBAM, with both Australia and the UK contemplating their options. ‘Climate clubs’ – however they become named – will be a defining aspect of trade policy discussions in 2024, as they were in 2023.

For commodity traders these emerging new trade policies might offer interesting opportunities as well as challenges.

Supply chains are also changing because of increasing transparency requirements. Businesses, and the supply chains they rely on, should be cognisant of consumer behaviour, litigation, investor demands as well as just changes driven by policy and regulation.

8. Electric vehicle sales continue to grow

During 2023, electric vehicle (EV) sales saw less profound growth rates than in recent history but proved resilient against macroeconomic headwinds in all markets. Globally, just over 12% of light vehicle sales in 2023 were full battery electric vehicles (BEVs). We expect this share to grow to over 16% in 2024. By 2025, one in five new car sales will be BEVs and our forecasts have penetration rates approaching 50% in 2030.

BEV demand in China is making a steady comeback from the drop at the start of the year, although it has seen much slower growth than last year. However, one of the notable shifts has been the growth in Chinese BEV exports. Over the first nine months, these grew 123% y/y, totalling 855,000 units. Tesla vehicles continue to comprise most of these, but Chinese brands are aggressively expanding overseas, especially in Europe. So far, the EU’s anti-subsidy probe has yet to have a profound impact on these plans.

In the US, sales did not boom and were very much underpinned by Tesla. However, the US BEV market continues to make solid progress and, in terms of y/y growth rates, is outperforming both Europe, where growth slowed, and China.

CRU’s forecast for battery demand remains strong, driven by a positive outlook for EV sales and growth in stationary storage markets.

See CRU’s Battery Value Chain Service for more information.

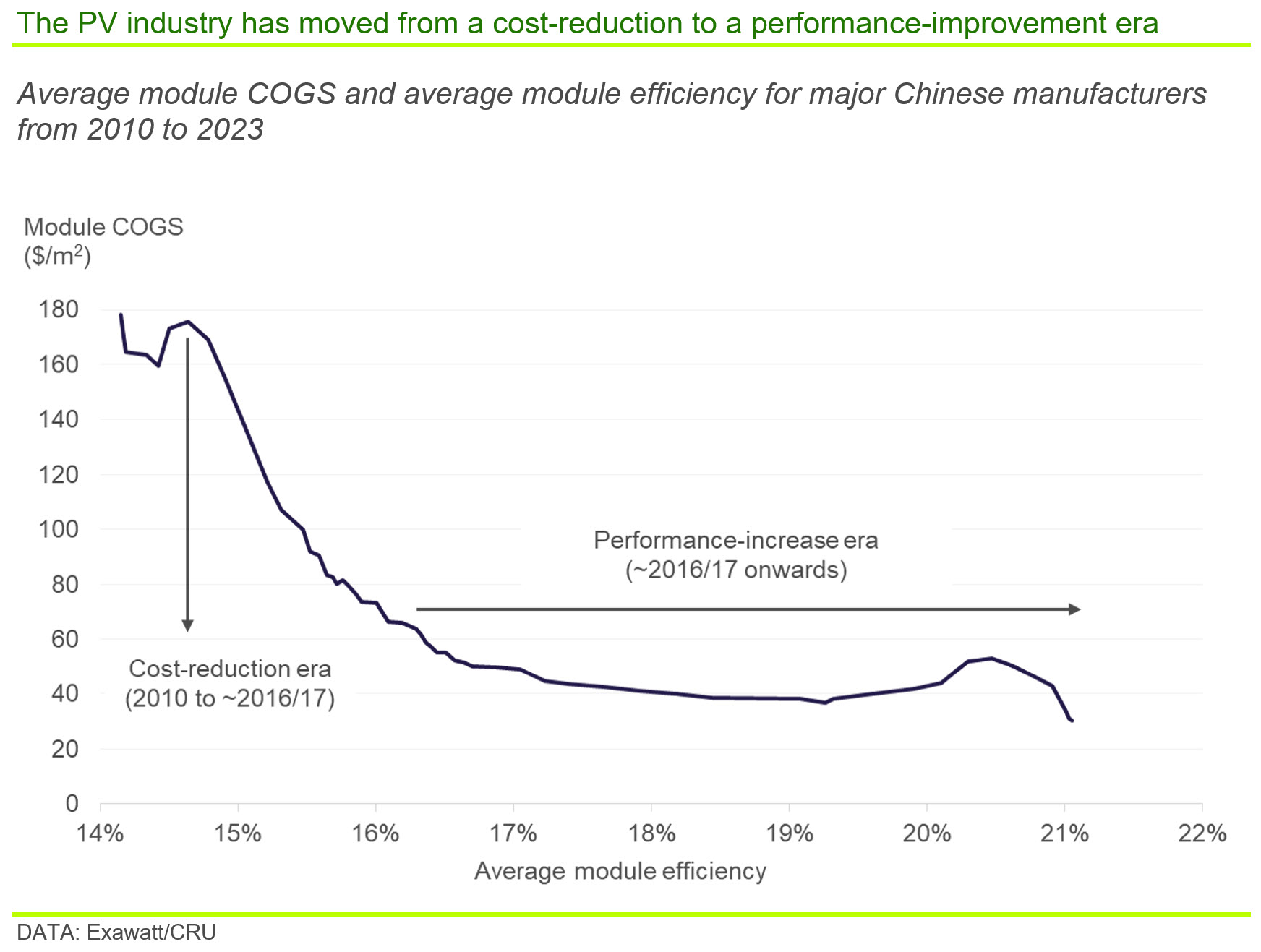

9. Renewable capacity grows, energy storage receives more attention

2023 saw a notable increase in renewable energy installations, with over 500 GWs of solar and wind capacity installed, with huge increases in Chinese deployment of solar. We forecast 2024 will see double digit percentage growth on this. However, in some regions, such as Europe, planning laws, labour shortages and higher financing costs are holding back deployment.

Increasingly, everyone involved across commodity markets will need to understand the costs and technical strengths and weaknesses of the new technologies that are shaping the outlook for both demand and supply.

Renewable energy has seen significant cost declines. Photovoltaic (PV) solar manufacturers have been highly effective at driving down manufacturing costs over the past decade. However, the era of “easy wins” has ended. Gains will now be harder fought, likely relying on either alternative materials or new technologies.

We remain bullish on the outlook for solar, with rapid increases in capacity forecast through to 2030 and beyond. However, this will not be without its challenges. Stationary storage applications will be increasingly essential to ensure grid stability as renewable sources grow in significance. This will receive more attention in 2024 than it has before.

Battery energy storage systems (BESS) will be the major source of short-duration (defined as 1-4 hours) energy storage. They are required for ‘load following’ and ‘peak shaving’, needed in combination with intermittent renewable energy sources.

To understand where and how batteries with competing chemistries will be deployed, we must look to their costs but also examine factors such as the security of their supply chains, recyclability, cycle life, etc.

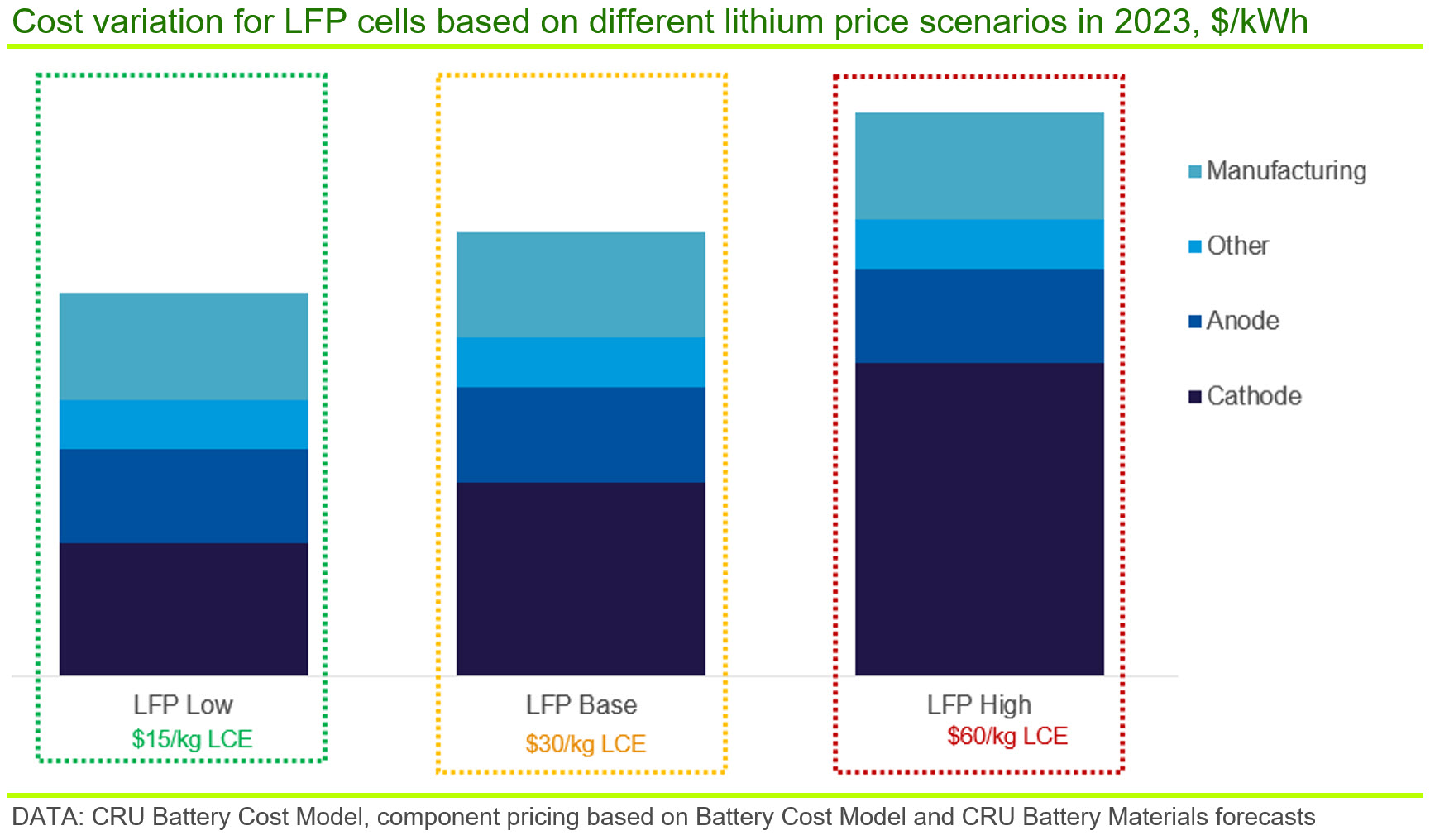

BESS is currently dominated by Lithium iron phosphate (LFP) batteries. Materials and components constitute 75% of the entire manufacturing cost of a LFP battery cell. The cathode accounts for more than 50% of the LIB cell cost and is comprised of the cathode active material (CAM), current collector foil, binders and conductive additives.

2024 will see more discussion of Sodium-ion batteries (NIBs), which are an emerging battery technology, which, in many instances, could replace lithium-ion batteries (LIBs) without much change in configuration of manufacturing or use.

Ultimately, sodium-ion technology will progress to a point where it has a performance close to some current LIBs, such as those with lithium iron phosphate (LFP) chemistries. Importantly, it could offer this but at lower costs and, despite its worse energy density, could see mass penetration into BESS markets.

See CRU’s Power Transition Service, Solar Technology and Cost Service, Energy Storage Technology and Costs Service, and Battery Cost Model for more information.

10. Continued excitement surrounding new technologies

The excitement surrounding some low-carbon technologies will continue to grow, with green hydrogen and ammonia, carbon capture and storage (CCS) and small modular reactors (SMRs) likely to receive much of this focus in 2024.

CRU believes, despite technological improvements and falling costs, there is not a panacea to solve decarbonisation. These technologies will, nearly always, require significant policy support or high carbon prices to be cost competitive compared to traditional, fossil alternatives. The EU, Japan and Australia are just three regions where policymakers are pushing green hydrogen production by offering financial incentives. Many solutions still need to be proven at commercial levels.

We expect the hype and hope to continue in some quarters but there will also be more realism surrounding where and when to deploy available technologies. Our abatement curves show that the lowest cost decarbonisation options are generally those where systems can be electrified (EVs, renewables, heat pumps, etc.). High production costs mean that green hydrogen and ammonia will be nearly always used in hard-to-decarbonise areas, where cheaper solutions are not feasible.

Small modular reactors received more attention in 2023, with 2024 likely to see this grow further. At COP28, 22 national governments signed a declaration aiming to triple nuclear energy capacity by 2050. In the US, at least ten different SMR technologies are being developed at various companies. South Korean companies are also developing technologies in this space, as are companies in China, France, and the UK. SMRs could see some deployments in the 2030s but will see a more rapid uptake in the 2040s due to cost reductions following the completion of various nuclear developers’ first SMR projects. However, compared to the impact of renewables, the impact of SMRs on energy systems will be modest, even in our long-term forecasts.

See CRU’s Low Emissions Ammonia Service, Power Transition Service, and Sustainability and Emissions Service for more information.

Author Charlie Durant

Research Manager View profile