Click here or above to enlarge the image

Click here or above to enlarge the image

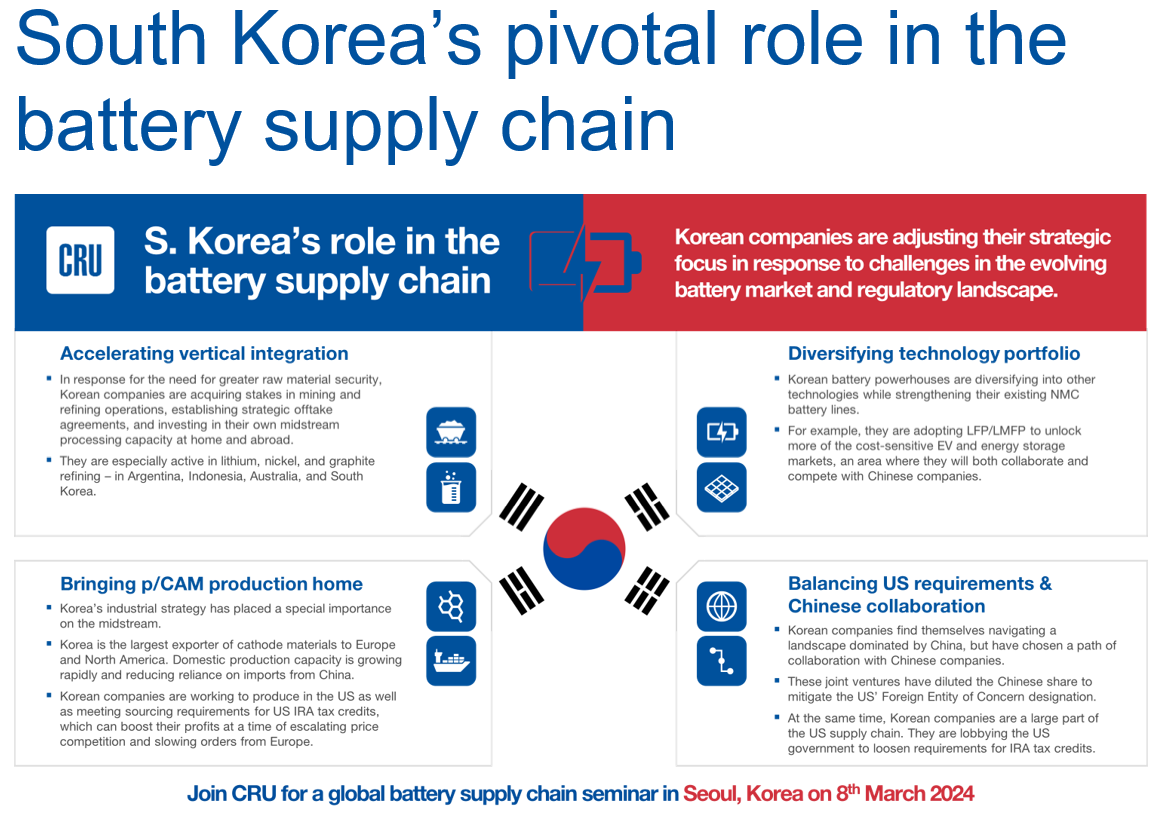

Challenges and responses

South Korea holds a significant position in the global battery and EV supply chain. Their long-term ability to compete in an industry that is dominated by China will largely be dependent on favorable policies, particularly from the US.

Tax credits under the US Inflation Reduction Act (IRA) provide Korean manufacturers with a competitive edge amid escalating price competition. Producing in the US or meeting strict mineral and battery sourcing requirements for EV tax credits can boost Korean producers' profits when they suffer from slowing battery orders from Europe.

Despite recent policy guidance on IRA rules, substantial uncertainties persist and are unsettling battery manufacturers. Potential policy shifts by the next US president, for example, could slow down electrification progress and the onshoring of manufacturing. Complexities in claiming EV tax credits through administrative actions present further challenges. Meanwhile, Korean manufacturers face intense competition from their Chinese counterparts in terms of cost and scale.

Considering these uncertainties and the substantial investments required overseas, Korean firms are proactively adjusting their strategic focus with the evolving battery value chain by:

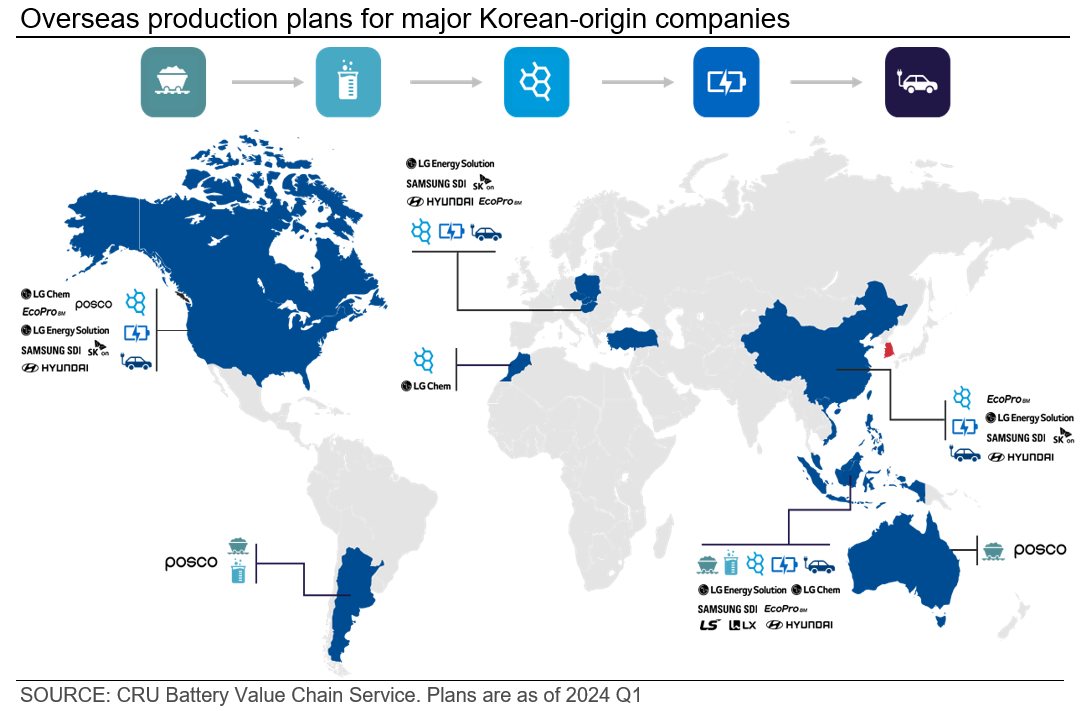

- Accelerating vertical integration – as a response to the need for raw material security

- Bringing precursor and cathode (p/CAM) production home – to reduce reliance on China and to meet IRA-compliant demand

- Diversifying technology portfolio – to drive cost reduction and access to more OEM customers amid intense competition from Chinese counterparts

- Balancing US requirements and Chinese collaboration – by collaborating with Chinese companies for strategic advantages, diluting the Chinese share in joint ventures to meet US IRA requirements, and making targeted expansions to serve overseas customers

Accelerating vertical integration

Korean companies face the need for a secure raw material supply and to avoid a bottleneck in the intermediate chemicals stage. As a result, they have embraced vertical integration, acquired stakes in mining and refining operations, and established strategic offtake agreements. They have also invested in their own midstream processing capacity at home and abroad.

They are especially active in lithium, nickel, and graphite refining in Argentina, Indonesia, Australia, and within their own borders. Korea’s industrial strategy has placed an importance on the midstream and has facilitated the expansion of energy-intensive production facilities.

Data from CRU Battery Value Chain Service

Data from CRU Battery Value Chain Service

Click here or above to enlarge the image

Bringing p/CAM production home

Korea is the largest exporter of cathode materials to Europe and North America, playing a major role in the US IRA-compliant supply chain. To keep up with this demand and achieve self-sufficiency, Korea’s domestic precursor and cathode production capacity grew rapidly in 2023 and reduced reliance on imports from China.

Although China will continue to be the leading consumer of battery chemicals, Korea is at the epicentre of a gradual re-focus of regional precursor and cathode production capacity. In turn, this is initiating a shift in regional raw material demand.

Data from CRU Battery Value Chain Service

This shift is influenced by the IRA’s sourcing requirements, which have spurred a response by producers in US Free Trade Agreement (FTA) countries such as Korea and Morocco. Additionally, downstream customers are urging that Korean suppliers localise plants to their regions.

Diversifying the technology portfolio

Many Western cathode and battery manufacturers do not see a strategic advantage in adopting lithium iron phosphate given China’s dominance in the sector. However, Korean companies are quickly developing their LFP and lithium manganese iron phosphate battery lines in prismatic form factors, once again by collaborating with Chinese companies.

Their goal of pursuing LFP is to unlock contracts with more automakers and capture more of the cost-sensitive EV segment, since cost reduction is now the highest priority. It would also facilitate Korean expansion in the battery energy storage market, particularly outside China. This sector is dominated by Chinese LFP producers, and there are growing concerns that they could corner the global market in the absence of strong competition.

At the same time, Korean companies are enhancing their existing lithium-nickel-manganese-cobalt technologies by pushing the nickel content to new highs. This is being done to enable more energy density and driving range, in addition to researching manganese-rich chemistries to deliver cost and environmental advantages.

The focus on diversification also extends to their geographic strategy. The three Korean battery powerhouses – LG Energy Solution, SK On, and Samsung SDI – have years of experience in producing at scale, but battery cell manufacturing capacity in Korea is lagging behind domestic demand. However, companies are instead focusing on localisation in overseas markets. For example, Korean battery joint ventures dominate the landscape in North America.

Data from CRU Battery Value Chain Service

Balancing US requirements and Chinese collaboration

Korean companies are navigating a landscape dominated by China but have chosen to collaborate with these companies and share many of the same operating practices and strategies. At the same time, Korean firms are a large part of the US battery supply chain. Therefore, Korea is a major focus for automakers seeking supply of critical minerals and battery components that comply with the criteria for IRA EV tax credits.

Data from CRU Battery Value Chain Service

Data from CRU Battery Value Chain Service

Chinese-Korean joint ventures extend overseas, and such operations are now diluting the Chinese ownership share to below 25%. This is done to mitigate the US’ Foreign Entity of Concern (FEOC) designation, which would otherwise exclude the joint venture company from being able to contribute towards IRA tax credits.

Additionally, they plan to further reduce this percentage by introducing another company, preferably from an FTA country, into the partnership and safeguard their investment. However, this may not be enough to avoid the FEOC designation, as US legislators are likely to uphold the spirit of the law to cut out Chinese companies from the US supply chain.

Korean producers are also lobbying the US government to loosen the requirements for EV tax credits. They are requesting concessions on what they believe to be unrealistic FEOC rules in addition to the increasingly stringent thresholds for sourcing critical mineral and battery components.

Policy is a major influence on Korean companies’ competitiveness and global footprint

Data from CRU Battery Value Chain Service

Korean companies have chosen a path of diversification and strategic collaboration with competitive Chinese counterparts, while leveraging South Korea’s role as a geopolitical ally to the US and Europe. Their success and ability to hold on to a significant share of the global battery market is dependent on policy and, to a lesser extent, their ability to innovate. As long as policies such as the IRA are favorable – which is not guaranteed – Korean companies will be able to compete in an industry dominated by China.

Join CRU for a global battery supply chain seminar in Seoul, Korea on 8 March 2024.

Explore this topic with CRU

Click here or above to enlarge the image

Click here or above to enlarge the image