The steel sector has identified ways in which decarbonisation can occur. Consumers who have set decarbonisation targets have demonstrated willingness to pay a premium on genuinely green finished steel and iron ore products to secure future supply and ensure these targets are met. For producers, a green premium will likely be needed in addition to the incentive created by increasing carbon costs for conventional steelmaking, through regulation such as the EU-ETS and CBAM, in order to be competitive in the market. Nevertheless, there remains a high degree of uncertainty among buyers, producers and investors surrounding how any such green premium will be determined.

In this insight, CRU explores the various drivers of the green premium and how it may vary across different end-use sectors.

Author Matthew Poole

Associate Managing Consultant View profile

Callum Ross

Consultant View profile

Kostiantyn Golovko

Principal Associate Consultant View profile

Later in this series, we will explore how the green premium might evolve over time and to what extent any green premium can pass upstream to intermediate and raw materials products.

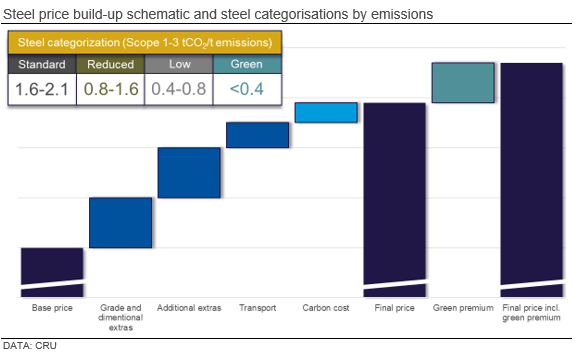

Green premia will be paid over and above existing steel prices – including carbon costs

There is currently no legally accepted definition for low carbon emissions steel, and it is likely that a range of these steels will emerge with different levels of CO2 emissions associated with their production. However, the top end of the spectrum - genuinely green steel - is likely to be associated with emissions of below 400 kg CO2/t of finished steel for Scopes 1, 2 & 3 (or 200 kg CO2/t of finished steel for just Scopes 1 & 2). Consequently, low-carbon emissions steel could attract a premium over conventional steel prices – including carbon costs – and will otherwise become known as the green steel premium.

A green premium is ultimately derived from the additional value the customer perceives or attributes to the green credentials of the commodity. The level of premium is not necessarily limited to any additional costs associated with producing the green commodity vs. low-carbon, reduced-carbon or standard equivalents. This characterisation has been borne out of research CRU has conducted with potential buyers of green commodities. As a result, the green steel premium is paid over and above: (1) all other price/grade, width, gauge extras and cost surcharges; and (2) any current and future carbon costs or surcharge’ that may be levied on conventional, reduced-carbon or low-carbon commodity producers by virtue of any carbon taxes/emissions trading schemes.

Our research has shown that the market pull and cost of decarbonising will primarily determine the range of green premium observed by product and region. The upper bound for the range of the green premium observed within any one region for a singular product is set by the market pull.

As with all commodities, the relative supply/demand balance within the specific commodity market or eco system will be a factor in determining the premium. If demand runs ahead of available supply, the premium will be considerably higher than the additional costs (if any) of producing the green commodity. Conversely, if there were to be an excess of supply, it is likely the green premium would be at risk of being eroded or destroyed.

The lower bound is set by the cost of decarbonising the preferred technology routes in each region. This is result of the fact that green demand will be met primarily by existing producers who transition to low-emissions steelmaking. In Europe, the BF/BOF is currently the dominant technology, and the greening costs are considered with respect to this technology. Green steel suppliers will then keep producing as long as they can sell the good for a price that exceeds the costs of producing steel using low-emission technologies.

Within the cost of decarbonisation, it is possible to define what the market will deliver on its own and what requires further incentive. CRU has recently launched its Steel Abatement Value (CRUsteav), which defines how the market alone will currently value abatement for a range of existing steelmaking technologies.

If the CRUsteav value is equal to the cost of decarbonisation to a given level of CO2 intensity, then the market is providing sufficient incentive to deliver low-emissions steel. If CRUsteav is less than this cost – as is the case today – then the market requires some additional top-up incentive. This can be considered as the lower-bound green premium.

The chart below displays where some of the largest steel-producing regions fall within these criteria. In Europe, the rise in Scope 3 decarbonisation commitments by the major steel-consuming segments provides significant impetus for market pull. However, conversion from the predominant BF-BOF steelmaking route to H2-DRI-EAF, as is preferred by many incumbents, will likely be expensive.

Conversely, in regions such as the GCC, producers are already utilising NG-DRI-EAF technology, with sizeable opportunities for carbon utilisation and storage in the oil fields. Steel producers in this region are likely to have lower decarbonising costs than other regions, which could be covered by a carbon cost surcharge. However, the demand pull is relatively minor, with most projects being export-orientated. As a result, the green premium in this region is expected to be low compared to other regions.

The segmented nature of sophisticated steel markets will result in a wide range of green steel premia

The willingness of consumers to pay a green premium varies by geography, end use and product type. The EU steel market in particular contains a wide range of sectors that are typically segmented in terms of the end market (e.g., automotive, construction) or supply chain position/activity (e.g., distribution, rerollers). These segments have distinct product and service requirements. This segmentation means that the EU market for green steel will be heterogeneous with different green products satisfying different customer needs and commanding different green premium.

The value a company will place on a green steel is highly dependent on the proportion of both cost and carbon footprint that the steel contributes to the final product. For example, in automotive, CRU research indicates steel accounts for only 0.7-1.5% of the final product cost, but between 10-27% of carbon footprint depending on the model. Therefore, automakers will be prepared to pay a higher green premium than in the manufacturer of lower added-value commodity steel items such as office furniture and shelving. This is because the use of green steels will further help them to market themselves to customers as low-carbon companies.

However, these leading OEMs also recognise that once they commit to sourcing 100% green steel, they are committed forever. Their own marketing campaigns and new market image will not allow them to move back to even reduced-carbon steels. A key challenge for steel suppliers wanting to benefit from these companies' green steel demand will be successful homologation of their new green steels into making the final product.

A final consideration is the different purchasing strategies and contract types that various steel customers pursue. Large OEM’s (e.g., automotive, domestic appliances) secure annual contracts, with a limited number of suppliers to maintain bargaining power and reduce the risk of disruption to their inbound supply chains. In contrast, smaller companies that buy from service centres will purchase small quantities on a spot price basis. This difference in behaviour will drive a different premium in the different sectors.

Ultimately, in negotiating green premia, it is important that both buyers and sellers are clear on what is and is not within the green premium definition, as well as the drivers behind the range of green premium observed by sector. A more robust understanding will allow financiers and producers alike to rely on the resultant cash flows as bankable. If you would like further insight into the fundamentals behind which the green steel premium is likely to be determined, please reach out to CRU Consulting’s Matthew Poole and Callum Ross.

Please also join our upcoming webinar; "Preparing for a world of green steel", taking place on Thursday 4th April at 10.00BST

Explore this topic with CRU

Author Matthew Poole

Associate Managing Consultant View profile

Callum Ross

Consultant View profile

Kostiantyn Golovko

Principal Associate Consultant View profile