Since copper prices’ spectacular rally to new market highs in 2024 Q2, more focus than ever has been on downstream demand of this commodity, of which ~70% is used for metallic wire and cable applications for energy and communication. Aluminium has also moved into the spotlight since the topic of cost-based substitution has been reignited, as manufacturers look to increase optionality of materials amid these record-high prices.

Author Aisling Hubert

Senior Analyst View profile

Over the past year, metallic wire and cable demand has been tumultuous. In the west, many major economies have continued to grapple with inflation, which saw high interest rates subdue construction levels. Europe in particular has been hit hard.

The US has sought to counteract a similar downturn with large-scale public spending programmes, which have seen huge increases in construction of manufacturing facilities amid the Build America, Buy America initiative. This has helped to counteract the wider slowdown but has come at the cost of protracted high inflation. In China, which alone accounts for over 40% of global cable demand, the beleaguered residential property sector continued to struggle as housing completions fell and new starts floundered. Government spending via state-owned enterprises in renewables and grid demand helped to support cable demand, but questions about the viability of this strategy long-term abound.

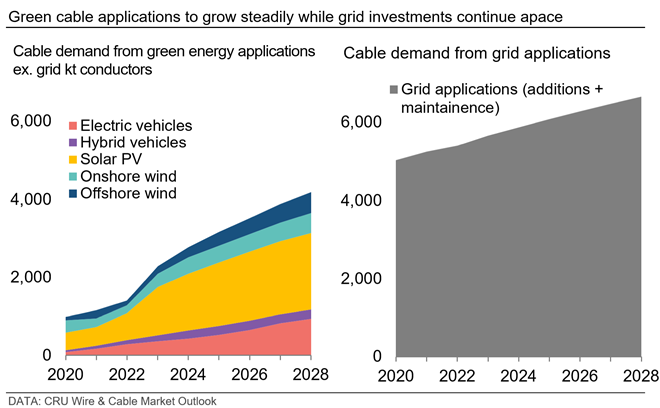

Despite the challenges, there have been positive developments in cable demand, not least of which are the collective green applications we define as cable demand from renewables, new energy vehicles (electric vehicles and plug-in hybrids) and grid applications. In June 2024, CRU added new insight into renewable and automotive cable demand into the Wire and Cable Market Outlook service.

Renewable demand steadily increases

In 2023, utility applications – predominantly power transmission and distribution – accounted for 26% of total global cable demand. The past few years have seen the monumental rise in renewable energy installations in many countries around the world due to a rising desire for energy autonomy, maturing supply chains and record-low costs of installations. In 2024, renewable energy applications account for 8% of total wire and cable demand.

Solar PV installations account for 70% of total renewable-derived cable demand in 2023, representing the current largest source of demand in this sector. The cost of solar installations has dropped dramatically in recent years as a glut of Chinese production has led to record levels of exports. Solar cable demand also represents the forefront of the substitution discussion, where aluminium cables are much preferred compared to their copper counterparts due to their cheaper costs and lighter weights.

Offshore wind installations are also a key focus of the wire and cable industry as these high-voltage, submarine cables represent the cutting-edge of cable technology, therefore commanding the best margins for manufacturers. These projects also open the option for greater levels of involvement in the cable installation and servicing business. This is an attractive option for many companies who seek to diversify away from pure-play manufacturing companies.

Due to the large-scale and nationalised nature of many offshore projects, the pipeline is highly dependent on individual projects and a handful of countries where offshore wind is cost-effective. By 2030, CRU forecasts that the demand for high-voltage submarine cables will be as large as demand for insulated high-voltage cables for land-based applications.

Automotive demand experiences some short-term headwinds

In 2023, transport applications accounted for 10% of total global cable demand, with the majority coming from light duty automotive manufacturing. Electric vehicles (EVs) are twice as cable-intensive than their internal combustion engine counterparts – hybrids are two thirds more intensive. Though 2024 has been a disappointing year for new energy vehicle sales, overall, CRU does forecast the total share of these vehicles to increase steadily, which – given these higher cable intensities – is positive for overall automotive wire and cable demand.

In EVs and hybrids, enamelled winding wire is used in vehicle motors and power generators. High-voltage cables rated above 60 V are used for battery harnesses, HV auxiliaries, recovery systems and in AC/DC charging. Low-voltage cables <60 V are found in both new energy vehicles and conventional vehicles and supply power to a wider variety of systems in the form of wiring harnesses.

Economic factors, policy changes and a lack of affordability have slowed EV growth rates and pulled-back of adoption targets and supply chain projects. Meanwhile, competition continues to intensify in China, perpetuating price wars as automakers battle for market share. The removal of subsidies in Germany has slowed uptake with overall European demand stagnating, many EVs in the US have also seen subsidy removals. In most regions, charging infrastructure is also a bottleneck to growth. Overall, CRU is optimistic about the new energy vehicle segment, though growth rates may be throttled by other factors in the short term.

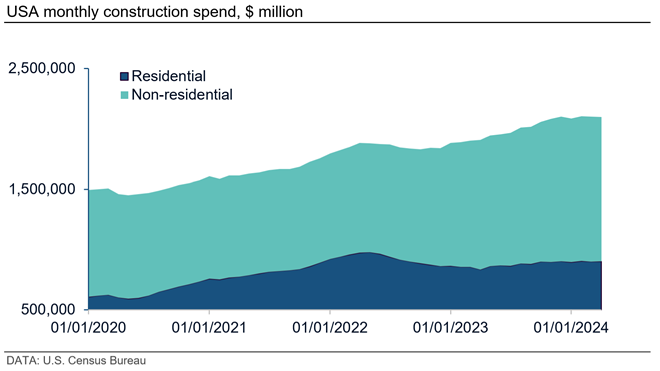

Construction and manufacturing struggle in major economies

Over the past year, the traditional segments of construction and manufacturing have both experienced macroeconomic headwinds in several major economies, slowing these key sectors that account for 39% and 25% of global cable demand, respectively.

In China, residential construction has been contending with structural challenges due to highly indebted development and falling demand. In 2023, the industry still managed to push through building completions, but this is tapering off as new starts have stalled. Despite this, non-residential construction has been strong, with manufacturing and office space growing solidly. Manufacturing is the stand-out performer of the Chinese economy and represents a strategic thrust of the country in the wake of the recent Third Plenary meeting, which concluded on 18 July 2024 and reiterated the focus on high-value technological innovation.

In Europe, high interest rates drove construction rates down as borrowing costs increased and mortgage rates became more expensive. Though interest rates have begun to fall, inflation is not falling as quickly as was hoped, and a true construction sector recovery is unlikely in 2024. Manufacturing has also been hit hard, as high energy costs in key countries such as Germany and a lowered appetite for goods consumption has seen demand fall.

In the US, though interest rates rose similarly to Europe, huge levels of national spending via the country’s many initiatives such as the Inflation Reduction Act, Infrastructure Investment and Jobs Act etc. have led to stronger economic performance than Europe but at the cost of more persistent inflation. Cable demand for construction has remained strong overall as huge levels of non-residential construction have been undertaken, cancelling out any slump in the residential side. As for manufacturing, the Build America, Buy America initiative has so far seen large amounts of manufacturing capacity increase announcements which will be long-term beneficial for cable demand, though output has remained steady since mid-2022.

Overall, global cable demand for 2023 was one of mixed performance. 2024 is largely more of the same with few stand-out topics bar higher commodity prices. We forecast a better 2025 as interest rates are lowered in many regions of the world. This year, over half of the global population will be voting in elections, so there is still considerable scope for large policy announcements and change, although manufacturing autonomy as well as grid and energy investments are key themes to be prioritised across the political spectrum.

Explore this topic with CRU

Author Aisling Hubert

Senior Analyst View profile