Global windfarm development is accelerating, and Europe has long taken a leading role in wind energy development. Wind generation is very intensive in a number of key materials, and the EU’s ambitious targets will support demand for them. However, in a number of places the relevant supply chains may come under strain, starting mid-decade, raising costs and potentially limiting investment.

Author Glen Kurokawa

Power Sector Lead View profile

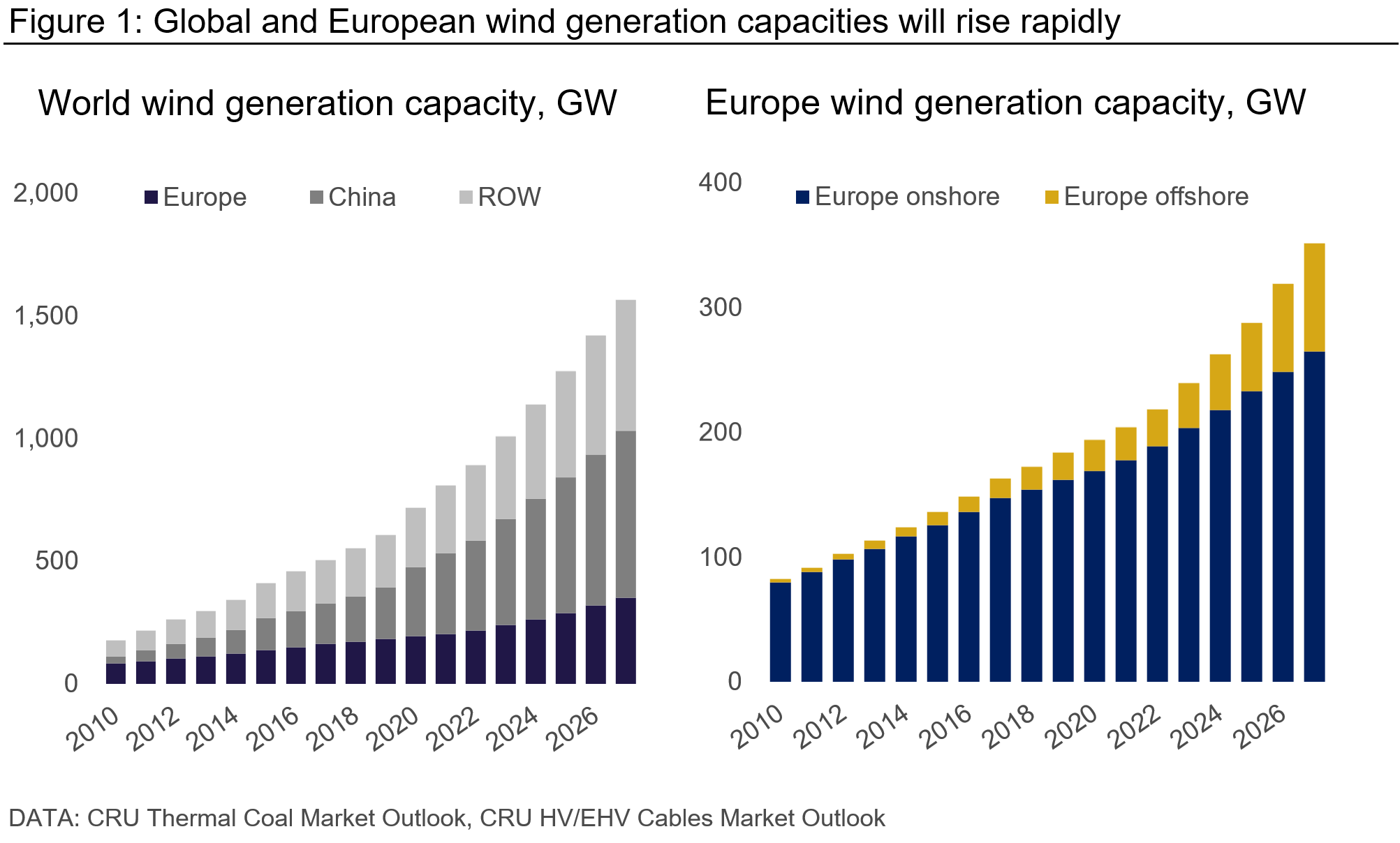

Wind power development will rise rapidly

In 2022, European wind generation capacity (excluding Turkey and Russia) accounted for ~220 GW of the global total of 890 GW. This includes 190 GW of onshore and 30 GW of offshore capacity. Due to ongoing decarbonisation efforts in the EU, coupled with declining costs and technological progress, we forecast wind generation capacities will grow over the next several years – although China will outpace Europe in adding new capacity (Figure 1).

Wind generation is highly capital intensive. During the period 2023–2027, we estimate the typical capex. for onshore and offshore wind will be ~$1.5 M and ~$4 M per MW of capacity. In addition to labour, financing, administrative and other costs, capex. includes significant outlays on materials including steel, cable and rare earth elements. The availability or cost of these materials and others could limit the speed at which Europe can build wind generation capacity.

The rest of this CRU Insight considers the supply of steel, cable and rare earth elements in turn.

European steel capacity could be strained

Plate is the main steel product consumed in both onshore and offshore wind installations. For onshore installations, heavy plate and some coil plate is used for the turbine tower, typically ~75 t/MW total. Heavy and coil plate is used for offshore towers, while heavy plate is also needed for the foundations, typically equating to ~212 t/MW total.

Over 2023–2027, our forecasts of wind capacity construction imply Europe needs ~6.5 Mt (i.e. ~1.3 Mt annualised) and 11.0 Mt (i.e. ~2.2 Mt annualised) of plate for onshore and offshore windfarms respectively. This implies around 17.5 Mt of plate production, which is ~13% of European mill and coil plate capacity.

However, not all plate mills can provide supply for wind turbine monopile foundations. As windfarm construction accelerates, European producers may struggle to meet demand. Countries beyond Europe will be building more windfarms at the same time. Plate supply from South and Southeast Asia may tighten as increasing urbanisation consumes more plate in those regions, and Northeast Asian plate supplier capacities are set to decline. If Europe needs much more plate than expected, it may start to face tighter plate import supplies by 2027.

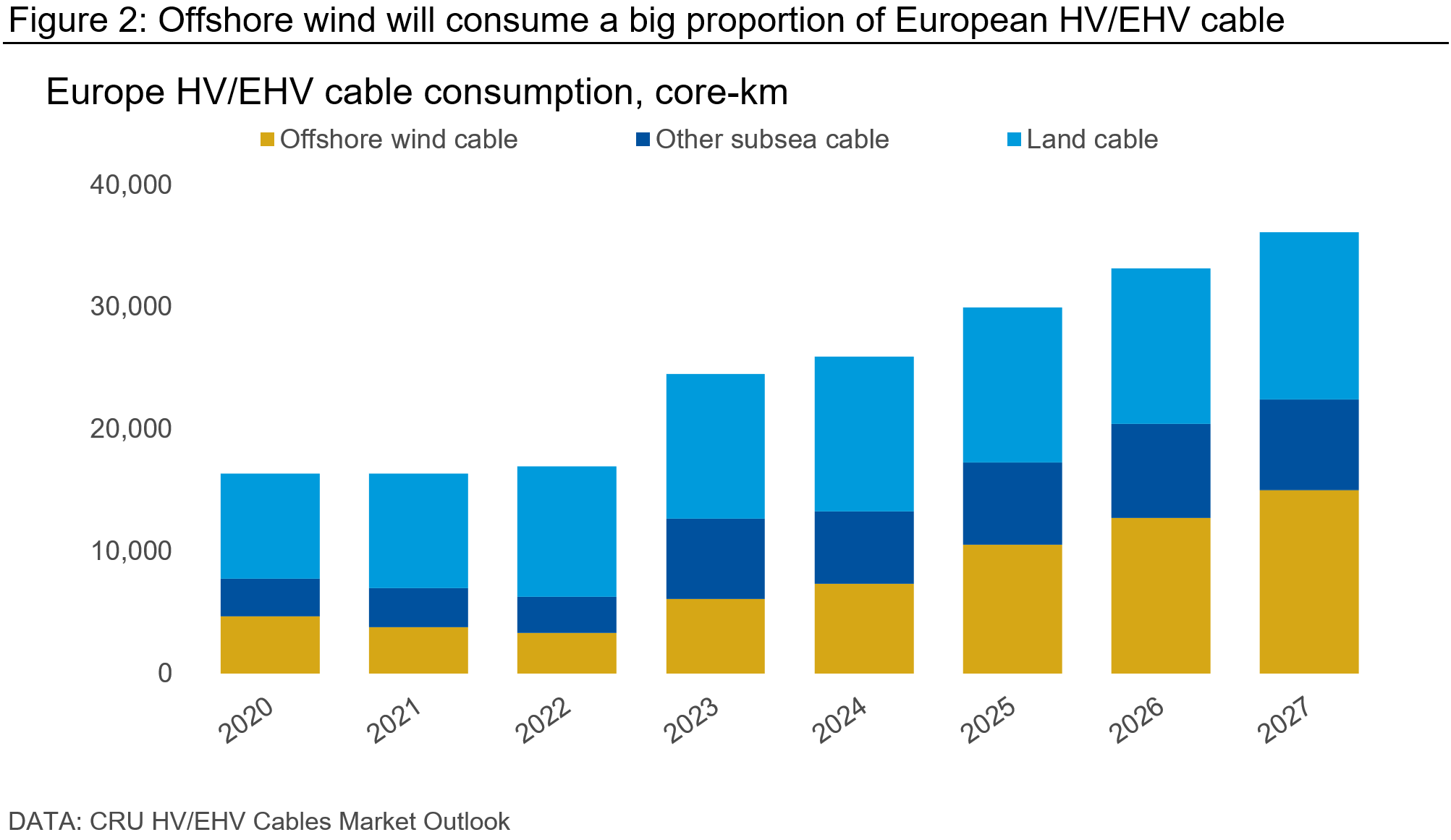

Cable supply will be tight

In March 2023, the European Commission (EC) proposed measures for securing access to aluminium (Al), copper (Cu) and other minerals. However, aluminium and copper are unlikely to present major risks to European windfarm construction over the period 2023– 2027.

Aluminium plate, extrusions, wiring and motors are used for windfarm construction. However, the ~300,000 t of aluminium demand for windfarms over the period in question is just a fraction of the ~18 Mt that Europe is expected to produce. As for copper, Europe needs ~950,000 t of copper to 2027 for windfarm construction, which is only a small portion of expected European refined copper production over the period.

Some of the aluminium and much of the copper in windfarm construction are consumed as wire and cable. Onshore and offshore windfarms will need wires and lower voltage cables, but these are not expected to be bottlenecks in Europe. However, offshore windfarms require subsea HV and EHV export cables and delivery of these cables might face long lead times. As noted in the recently published CRU HV and EHV Cables Market Outlook, offshore windfarm export cables accounted for ~10% of HV/EHV cabling globally in 2022. The proportion in Europe, while smaller, will grow rapidly this decade. Onshore windfarms require little HV and almost no EHV cables.

Cable manufacturers in Europe prioritise the highest-margin EHV cable over other cable supply, effectively causing shortages. Delivery times for export and array cables for offshore windfarms can be around four to five years in Europe, which can complicate Europe’s desire to reduce renewable project commissioning times. China has some excess production capacity currently but Europe is hesitant to buy Chinese cables for specification, quality, future maintenance, and perhaps security reasons. If cables are ordered late in an offshore wind project timeline, commissioning delays are likely.

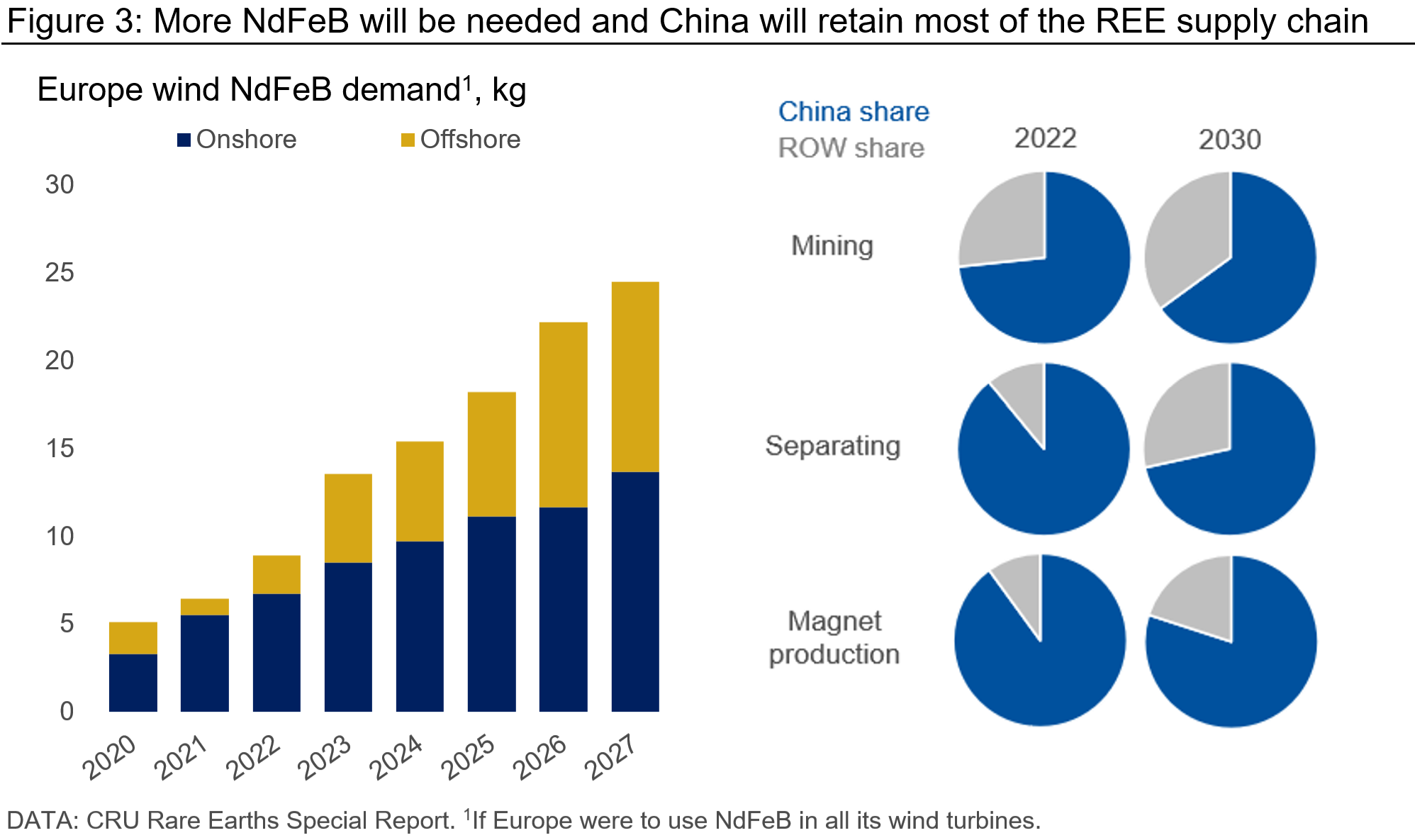

REE supply will remain concentrated in China

Wind turbines generally use rare earth elements (REE) for permanent magnets, particularly neodymium iron boride (NdFeB). As noted in the recently published CRU Rare Earths Special Report, offshore wind turbines often use low-speed direct-drive technology with very high NdFeB intensities, whereas onshore wind turbines most commonly use highspeed gearboxes, which have much lower intensities.

The highly concentrated REE supply chain – including mining, separation and REE magnet production – in China is an obvious geopolitical risk for European wind to the extent REEs are used. Due to technical challenges and the time required to develop an REE supply chain, China will remain dominant in all of these aspects to 2030 and beyond, though there are some limited efforts by western governments to reduce this share. China has recently considered possible restrictions on rare earth exports, illustrating the risk. Rising tensions between the US and China over trade, technology and geopolitics highlight this risk further.

Energy storage facilities also require commodities

Windfarm construction is exposed to other potential commodity bottlenecks, including supply of nickel, lithium, cobalt, manganese and graphite for energy storage, though we do not discuss them in detail here for brevity. Energy storage is an underestimated topic, but these minerals will be important for wind energy because of intermittency. Each appears in one or both of the EU’s strategic and critical raw materials lists, and the accelerating energy transition will create more demand for these materials.

Further acceleration will exacerbate supply risks

The commodities discussed here and used for windfarm construction will be costly, with a GW-scale offshore windfarm requiring hundreds of thousands of tonnes of steel as well as large amounts of cable and expensive REEs. That is a benefit for metal producers in Europe and elsewhere, as it will provide a structural source of demand growth. If supply risks materialise, those extra costs will slow Europe’s ability to meet its goals on decarbonisation. Steel plate supply might be strained, cables have long lead times, and REE supply is subject to geopolitical risks. Bottleneck risks across all commodities for windfarm construction will likely become more important beyond 2027 when installation is expected to accelerate further.

Contact us for analysis and commentary about this and more.

Explore this topic with CRU

Author Glen Kurokawa

Power Sector Lead View profile