The iron ore industry has had another strong year in 2023, as the price is set to average close to $120 /dmt for the full year. Looking ahead to 2024, CRU has highlighted three important developments that are worth keeping an eye on: a significant upside risk to prices, a turnaround in the low-grade market, and India’s rising iron ore imports.

Author Liz Gao

Senior Analyst Iron Ore View profile

Contributor Aaron Kearney-Keaveny

European Steel Sheet Analyst View profile

Contributor Erik Hedborg

Principal Analyst View profile

Contributor Lalit Ladkat

Analyst, Steelmaking Raw Materials and Thermal Coal View profile

Contributor Richard Lu

Senior Analyst View profile

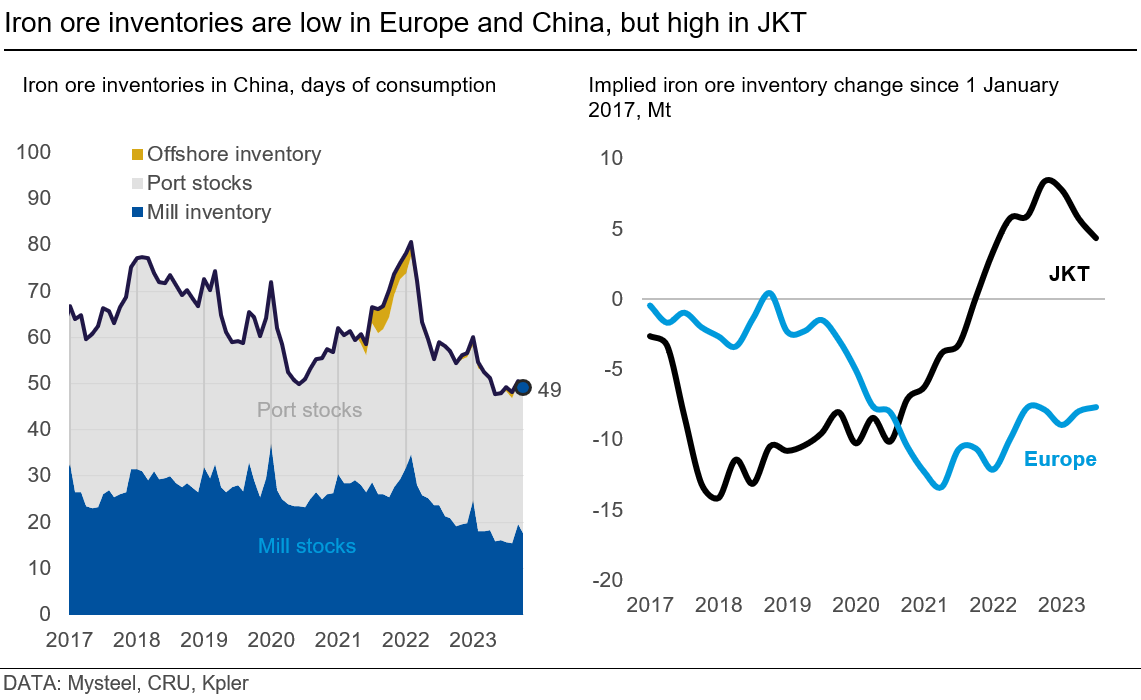

Low iron ore inventories to be a key upside risk

One reason that the iron ore price has held high is the low inventories in the supply chain.

In China, inventories have fallen steadily through the year, especially at mills, due to:

- High hot metal production (see reasonings here) leading to strong iron ore consumption;

- Mills suffering from low margins being discouraged to hold high inventories;

- Supply chains working better than in previous years, given no Covid-19 restrictions.

In Europe, steel mills have also drawn down inventories and will continue to do so to improve their balance sheets. JKT is an outlier, where inventories are reasonably high.

The low inventory level means the market is extra sensitive to supply/demand shocks and it could result in rapid price increases if steel mills intensify spot purchases or if there are unexpected disruptions to supply.

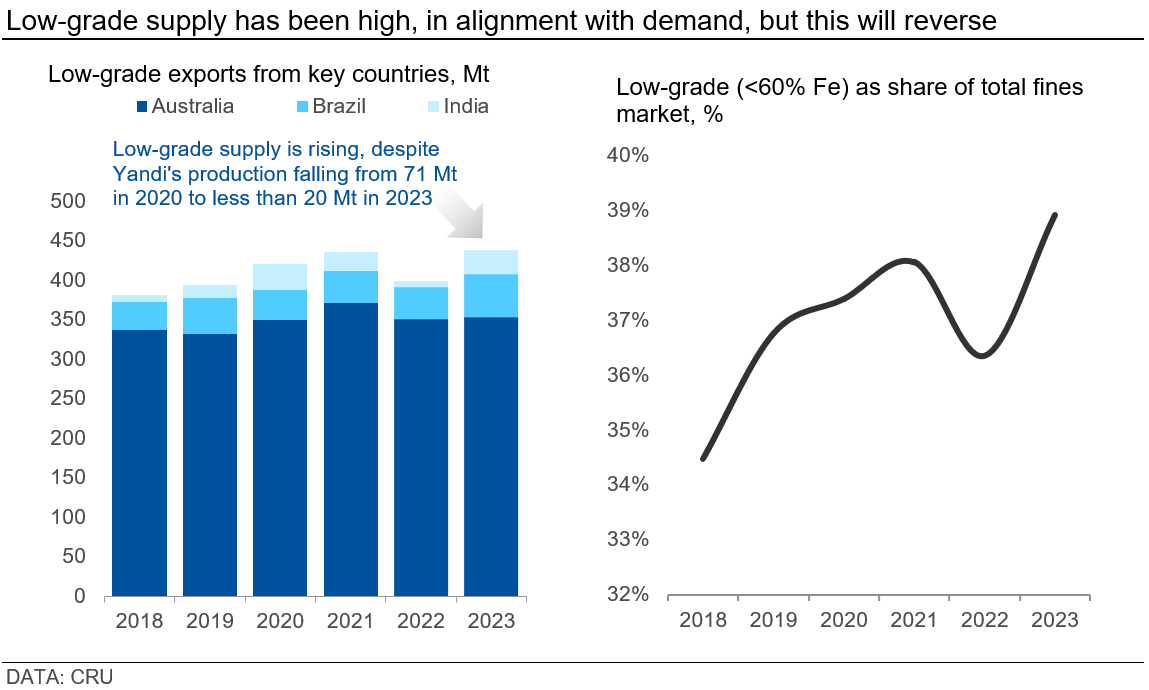

Low-grade market facing oversupply

In 2023, steel markets have seen weak demand and poor margins in most regions, so mills prefer low-grade materials for cost reductions.

In China, we expect the preference for low-grade ore to continue next year as steel margins will remain low. However, there are two key developments to keep an eye on:

- Total hot metal production will fall next year, meaning overall demand for iron ore and low-grade ore will decline slightly.

- As the low margins persist throughout the year, some mills will eventually leave the market, which could rebalance supply and demand of steel, resulting in a slight margin recovery in 2024 H2.

While demand for low-grade ore will remain steady, supply is expected to increase. Rio Tinto’s quality struggles will persist and Mineral Resources’ Red Hill project will add new low-grade volumes from the Pilbara. In our view, low-grade supply will rise more than demand and result in low-grade discounts rising from the current low levels of 6%.

During 2018–2022, the 58% Fe fines price was on average 14% below the 62% Fe price. In other words, the low-grade market will not be as strong as it is in 2023 Q4, and we see a high chance that discounts could be rising in 2024 H2.

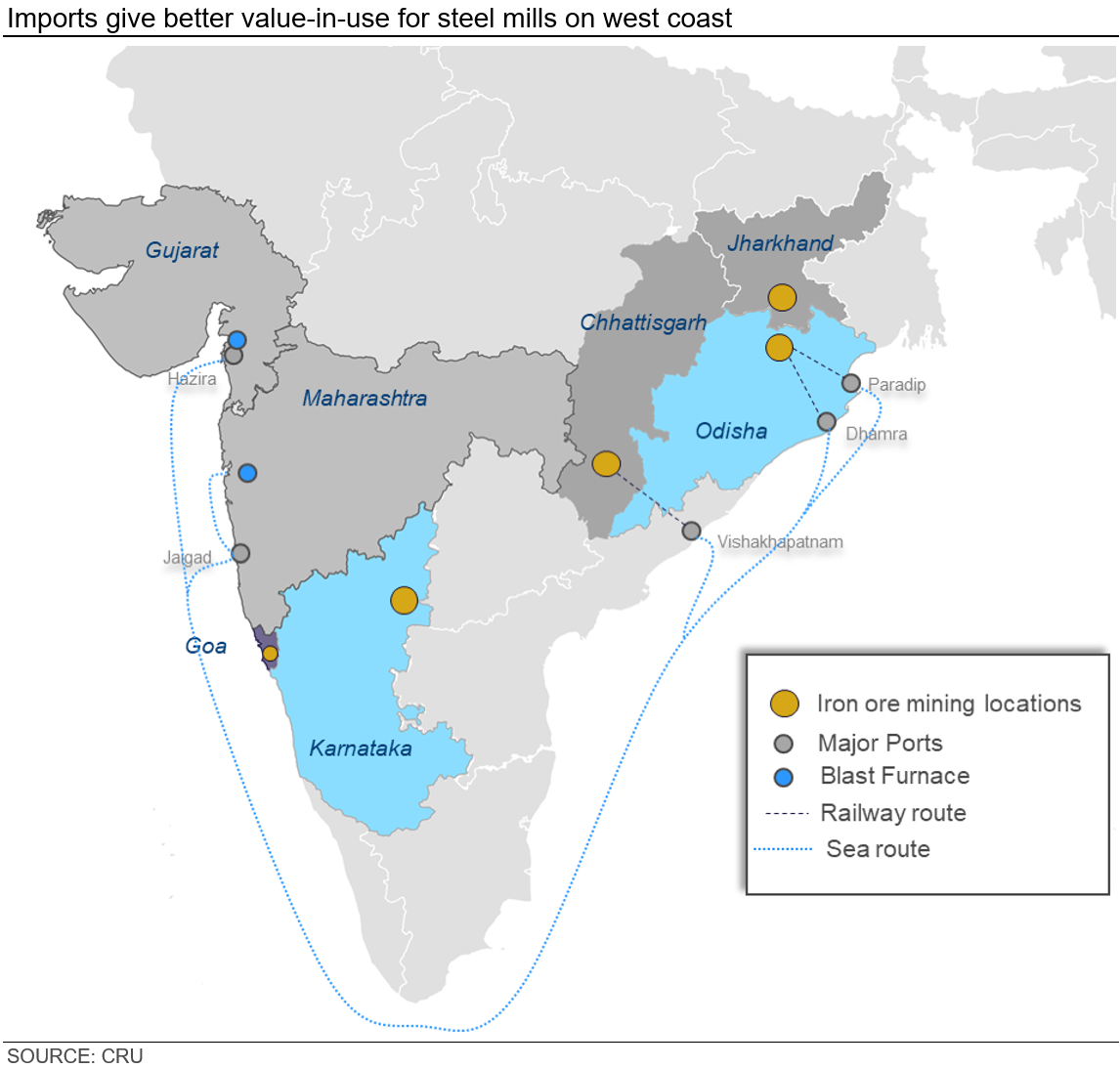

India starts to import iron ore

In 2024, Indian iron ore demand will continue to grow due to expanded BF-BOF capacity. However, slower growth in domestic supply, high inland transportation costs and concerns over supply from NMDC (the largest iron ore producer in India with an annual production of 40 Mt), will prompt steel mills to further explore opportunities for importing iron ore. The severe logistics disruptions at NMDC mines in September and the possibility of increased supply to NMDC’s captive mills that were commissioned this year, are accelerators to this transition. We have seen Australia exporting iron ore to India since June while hearing from contacts that Vale will supply BRBF from their blending facilities in Oman. We expect this trend to persist into 2024.

Author Liz Gao

Senior Analyst Iron Ore View profile

Contributor Aaron Kearney-Keaveny

European Steel Sheet Analyst View profile

Contributor Erik Hedborg

Principal Analyst View profile

Contributor Lalit Ladkat

Analyst, Steelmaking Raw Materials and Thermal Coal View profile

Contributor Richard Lu

Senior Analyst View profile