Regulatory pressure is the single biggest driver of energy transition and decarbonisation, and governments have signalled their intent to adopt and enforce regulation designed to help them meet their decarbonisation targets. Actual regulation has been slow to develop relative to the required pace of change, and this is seen as part of the reason we are, at global level, behind a 2 C schedule. However, number of industries have adopted procurement strategies that favour “greener” materials and are willing to accept substantial premia in anticipation of future regulation, and as part of their own value proposition. These green premia have encouraged much of the early development in low-carbon production and will continue to do so while regulatory environments mature.

Author Ionut Lazar

Principal Consultant View profile

Contributor Lewis Pegrum

Senior Consultant View profile

Contributor Simona Nenickova

Research Analyst View profile

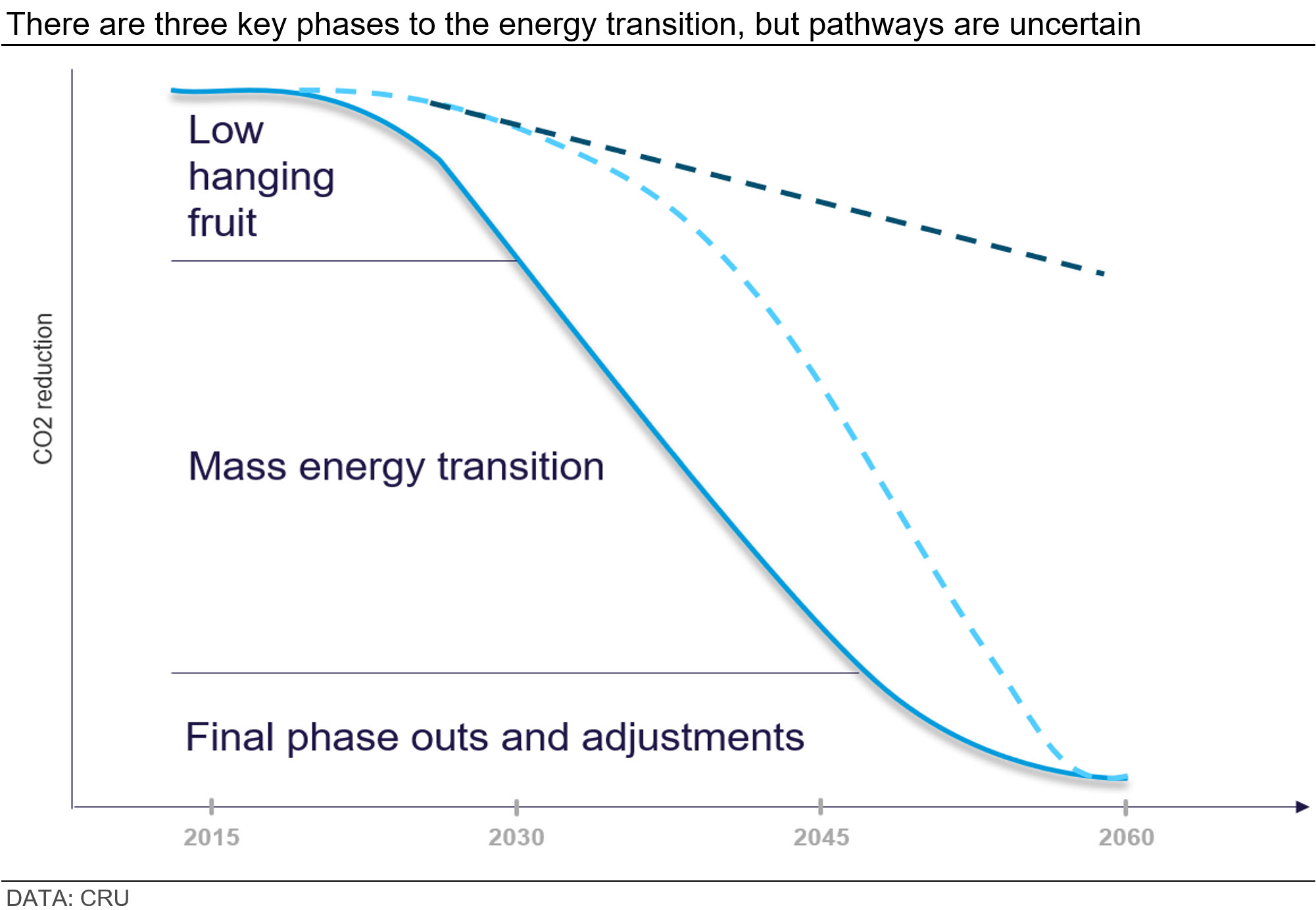

Three key phases to decarbonisation

The transition to net zero has, in theory, three key steps.

The first involves the setting of successful precedents in “easy to abate” areas to create momentum and establish confidence in economic viability. Some of these early precedents have, indeed, been set mainly in areas that combine the key necessary conditions – maximum renewable energy potential; easily reachable power consumption markets; and crucially, transition-friendly jurisdictions able to provide quick regulatory and financial incentives.

Once momentum has been established, the second step would involve mass transition to renewable energy, where a combination of solar and wind energy would be installed globally in large volumes. Energy storage would have to be deployed on a mass scale to counter the variable and interruptible nature of most renewable energy, with fossil fuel capacity used to balance the grid while storage is fully installed. In this step, electric vehicles would pass the hockey-stick moment and take a majority of the global market share, and heat pump installation would become widespread.

To drive mass transition, huge governmental intervention is needed. This will be in the shape of implicit or explicit carbon prices, but these are slow to develop, uneven in implementation geographically and extremely difficult to enforce effectively. Governments will also turn to mandated change and mass subsidies – both of which also have their strengths and weaknesses.

The third and final stage would, in theory, cover the final decade, and involve final adjustments to an overwhelmingly renewable grid and final phase-outs of fossil fuel capacity, as well as changes in the wider economy to include “greener” infrastructure and agriculture.

Hesitant start in regulatory pressure

While consensus is in short supply on many of the moving parts of the energy transition, most market observers would likely agree that we are still in the first step, well short of the progress thus far required. While electric vehicles are rapidly taking market share (helped by high fuel prices and government incentives in many parts of the world), progress in installed renewable energy has been inconsistent at best. The implementation of regulatory measures designed to phase out fossil fuel energy have stumbled, and in some cases stalled. Some of this is attributable to the energy crunch brought about in Europe by the war in Ukraine. More broadly, support for decisive regulatory action has not been universally embraced either electorally, socially or economically. For it to be successful, regulatory action needs to be wide-ranging, predictable, clear and relatively easy to enact and enforce. So far, this has proven very difficult to achieve.

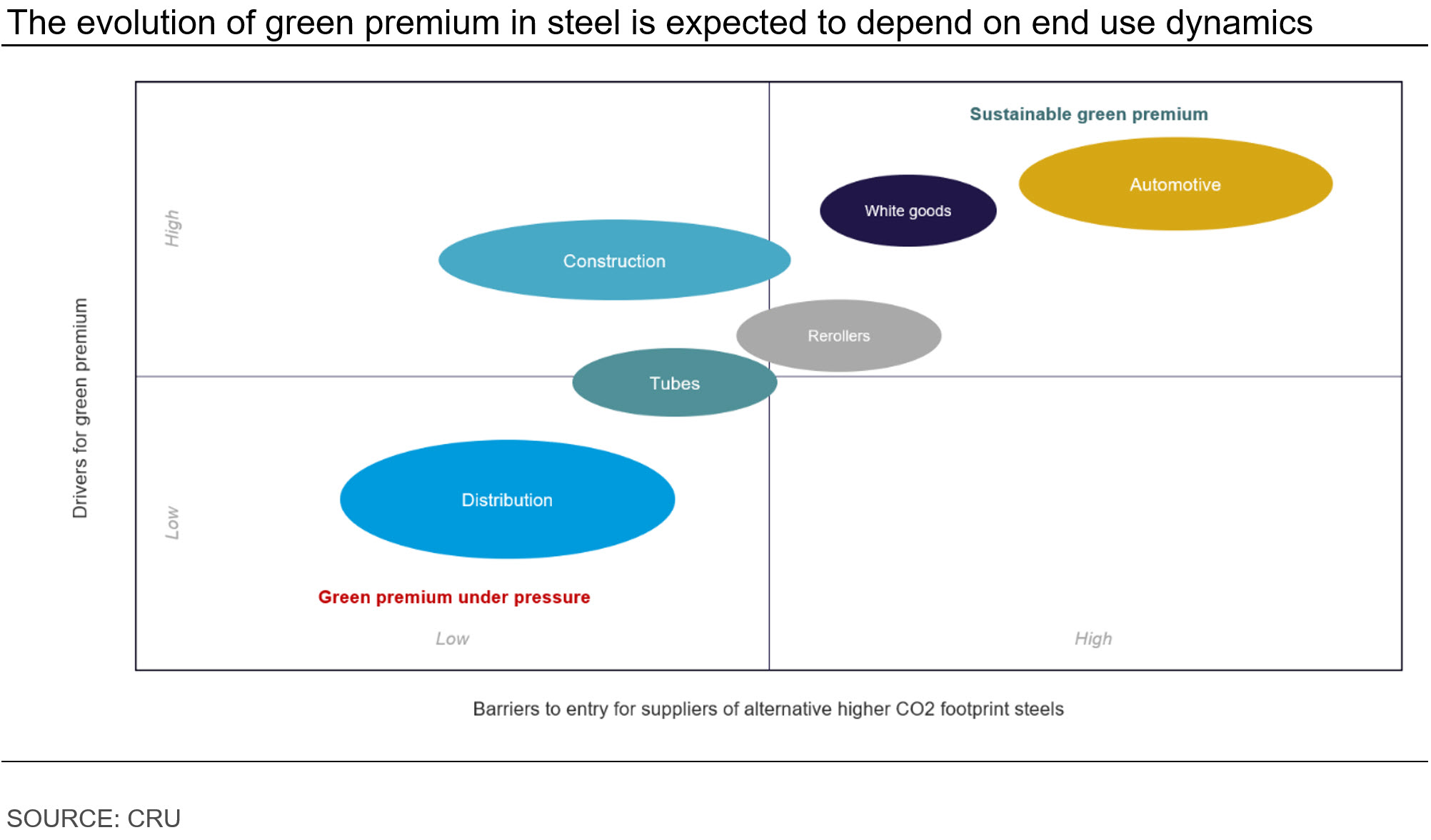

“Green” premia as the engine of low hanging fruit-picking

Without clarity on carbon pricing and the future of the regulatory framework, what can drive the setting of successful precedents? Thus far, the most promising of existing projects have relied on a permissive regional regulatory environments and incentives to develop, primarily originating from progressive end-use sectors. “Carrots” in the shape of governmental incentives and market-driven “green” premia have attractive traits in sharp contrast to regulation – they develop more organically in specific segments of the industrial sector and provide greater precision with regard to application and timing that is much more reassuring to all stakeholders, including project promoters, lenders and strategic partners.

Partly because of this need for reassurance, “green” premia have become established in mainstream industries, which are well understood by stakeholders and have experience in, such as aluminium, steel and ammonia. Work is still in progress in each of these industries to develop and maintain transparent premium benchmarks at specific emission levels, as well as to define the standards and process for certification. However, there is substantial evidence that “greener” material is already procured preferentially in the automotive, aerospace, machinery and household goods sectors. The premium is negotiated bilaterally and directly between producer and consumer and strategic partnerships are often involved. This makes sense, as it affords each side a period of guaranteed volume with predictable values – particularly important for the credibility of financial models covering the pay-back period of any finance deal.

The quality of the long-term agreements and partnerships is dependent on a number of factors, including the exposure of the parties to the same target markets, the ability of buyers to pass costs onto their client base, and/or the availability of regional incentives from the state or other stakeholders to establish “greener” procurement. CRU has carried out a number of assignments profiling and recommending partnership options and models, which allow rapid development at a time when first-mover advantage is essential. Throughout these assignments, one thing has been clear – in core industry sectors, strategic partnerships are widely available and vastly preferable to exposure to the open market.

By contrast, it is much harder to establish and demonstrate the existence of similar appetite for premiums in smaller, more niche markets that emerge as bottlenecks in the path of energy transition. This is somewhat paradoxical, since these materials form a smaller proportion of the overall production cost of the end application, and so in theory, the price resistance should be smaller.

In niche markets like high purity quartz for solar wafer crucibles or needle coke for electrodes, there is some evidence that existing players can indeed charge substantial premiums without demand destruction. In 2018, graphite electrode prices spiked abruptly without any resulting change in steel production. However, it is proving difficult for new entrants to demonstrate that they can achieve the same results. Part of the problem is naturally the opacity of the sectors, where incumbents keep pricing points well hidden from the broader market. Partly, lenders, traders and other stakeholders are wary of supporting sectors they know little about. Finally, in some cases Chinese domestic overcapacity represents a risk that cannot be immediately offset by the hope of future demand.

The solution in these cases is to provide information on new critical commodities in a way that is accessible and certifiably objective. The language has to be adapted to accommodate a wider audience, and the importance of each material in the energy transition value chains has to be carefully articulated. The supply and net trade situation in China needs to be well understood and transparently reported, and the threat of substitution from technical innovation has to be acknowledged and assessed. CRU, together with Exawatt, are ideally placed to do this, combining expertise in technology and the realities of mass volumes, so that market players can confidently make the most of the first step of the energy transition.

Long-term, and in particular during the mass transition second step, the “stick” of actual regulatory pressure will have the decisive role in driving the pace and nature of the energy transition. Regulatory environments need time to gain momentum and mature, but they also require precedents to evaluate and calibrate against. Right now, the best way to develop early movers is to target industry segments that are willing to accept “green” premia and seek partnerships with downstream stakeholders eager to secure low-carbon material.

Explore this topic with CRU

Author Ionut Lazar

Principal Consultant View profile

Contributor Lewis Pegrum

Senior Consultant View profile

Contributor Simona Nenickova

Research Analyst View profile