Activity on the European scrap market has not picked up significantly since our last report. Demand remains weak across all end-use sectors and even the automotive market is showing signs of weakness. As for scrap availability, it is limited by the fact that many semifinished producers are operating at lower rates, which means less scrap is coming back to the market. However, this does not translate in higher prices due to the weak demand.

Author Guillaume Osouf

Head of Aluminium Prices Development View profile

Now we are in the middle of Q2, there is limited hope that a recovery will take place before the summer. As demand is rarely buoyant in Q3 due to the many maintenance closures, the demand recovery has been pushed back to Q4 and even some are now questioning whether demand could improve substantially this year. Under this context, it is difficult to expect scrap and secondary prices in Europe to show any clear trends in the weeks to come. This consolidation pattern in prices is well set to last for a bit longer.

Weak demand continues to weigh on key sectors

Q1 results confirm challenging markets in packaging and B&C

Last week, Novelis released its 2023 Q1 results and as one of the biggest buyer of aluminium scrap in Europe, what the company is seeing is reflective of the market as a whole. The company reported a drop of 5% in total flat rolled product shipments versus last year and the drop was even more severe in Europe, with a decline of close to 10% y/y. The decrease, Novelis said, was mainly driven by lower beverage can shipments as can makers are still working through their inventories and the weak demand for specialties products used in the construction sector. The company did highlight the good demand from aerospace and automotive but this was not sufficient to offset the lost volumes in other sectors.

As one of the major can makers in the world, Ball confirmed the same trend with a drop of 5% of shipments in Q1 in Europe versus last year. This excludes its former Russian business, which was sold in 2022 Q3, as otherwise the drop would be even steeper. Ardagh Metal Packaging Europe also blamed lower volumes for a 3% y/y drop in revenue in Q1. Finally, Crown Holdings reported a decline of 5% in revenue at the group level in Q1, as higher beverage can shipments in the US were not enough to offset lower volumes in other regions, which include Europe.

Prices for mill and packaging scrap remain subdued

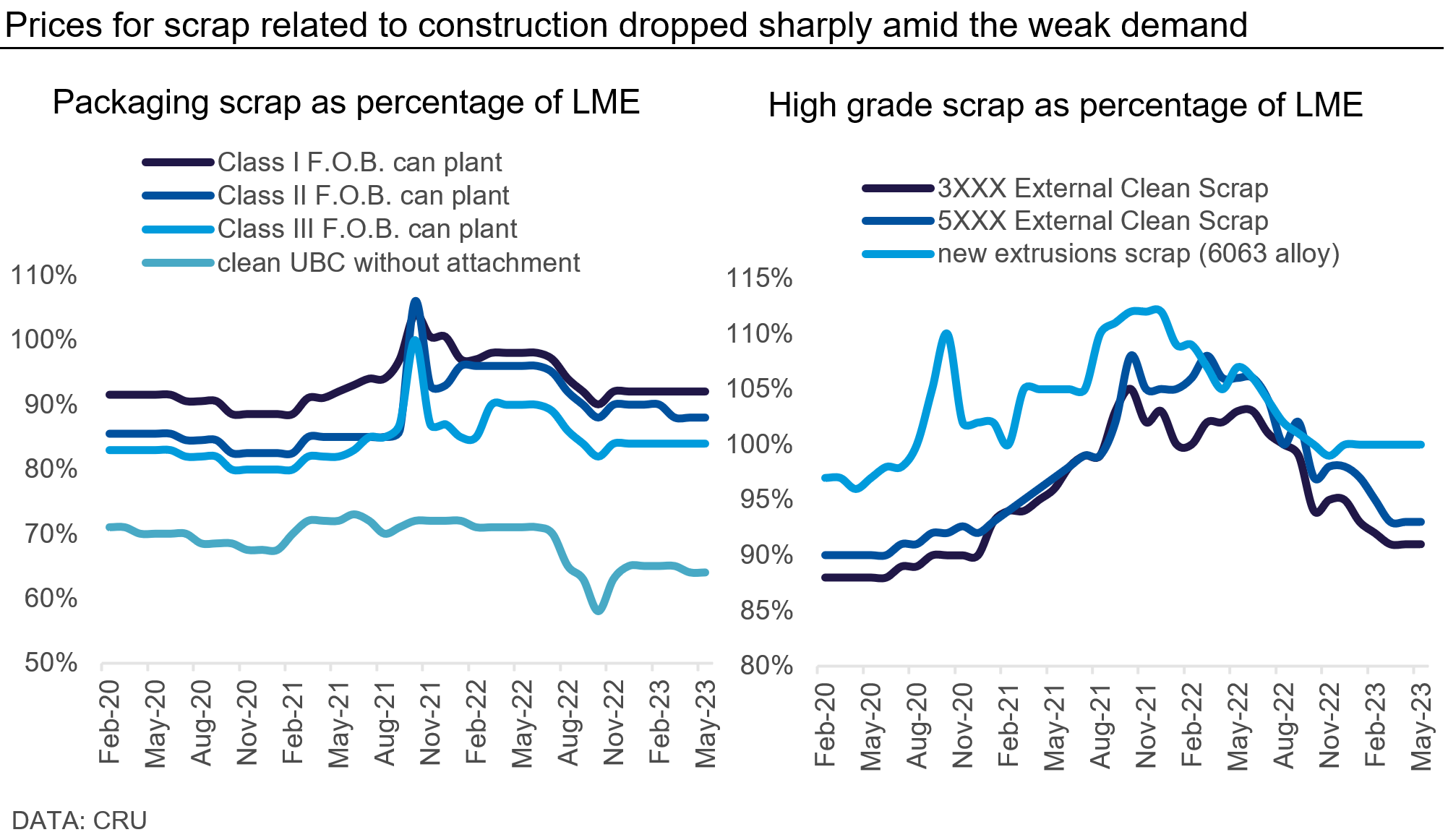

Demand for packaging has been hit by two factors. The high level of stocks at can makers and the weaker end-consumer demand due to inflation. At the start of Q2 there was hope that demand could pick up as the destocking phase comes to an end, and the quarter usually sees a seasonal boost in can production.

So far, we hear feedback that demand has not picked up substantially as can makers are still running high on stocks and the views on consumption for the summer remain bearish. As a result, aluminium semis producers in Europe are not actively buying UBCs; and other packaging scrap and prices for these grades have stabilised. UBC was last seen trading at 64% of the LME price. This is to be compared with over 70% only a year ago. The prices for class scrap have also dropped from last year’s levels, but to a lesser extent than UBC as a lot of these grades remain in closed loop, meaning pricing is less volatile.

The darkest spot remains the demand from building and construction. With demand usually slower over the summer, this means no recovery will take place before Q4 at the earliest. As high inflation and interest rates are set to persist, hopes for a recovery even later this year have faded. This is putting particular pressure on prices for mill scrap. 3XXX series and 5XXX series scrap were last priced at 91% and 93% of the LME price, which is stable from last month but down nearly 10 percentage points from the same time last year.

One last grade of scrap closely linked to construction activity is extrusions scrap, which has remained at LME flat since October last year. As extruders are still running at reduced capacity, less scrap is returning to the market, and we have been told that availability of extrusions scrap is actually tight. The fact that prices are not reacting to this is clearly a sign that demand remains weak, and it is not expected to pick up any time soon given the widespread maintenance closures over the summer.

Sentiment is becoming more mixed for automotive

Recovery continues at full speed, according to association data…

In Q1, the EU car market saw a substantial increase in new car registrations, with almost 2.7 million units sold, as reported by ACEA. This marks a 17.9% increase compared to 2022 and in March alone sales of passenger cars were up by 28.8% y/y. As for market feedback, it has been overall positive, with many car makers having sufficient backlog orders to keep their operating rates intact for the rest of the year. However, it is uncertain what will happen when that backlog gets worked through as new car sales have been hit by the high inflation.

The reality seems slightly different when moving down the value chain as financial results for some automotive part suppliers have been more mixed in Q1.

…but Q1 results and price action tell another story

Superior Industries, a leading manufacturer of aluminium wheels, reported a net loss of $4 M in Q1 after a profit of over $10 M last year. What’s even more surprising is that cost of sales were actually down nearly 4% from last year. This was all driven by the lower shipments, down 4% in North America and down over 7% in Europe. Back in 2022 Q1 supply chains were disrupted, preventing cars from being built, but this is not the case this time around. Moreover, shipments are down from last year. Although this might not be representative of the entire market, this clearly highlights the weaker European market. Indeed, Nemak, which also supplies aluminium components to OEMs globally, reported higher shipments compared to last year but the growth in Europe was limited to 4.7% versus an increase of 12.1% in North America.

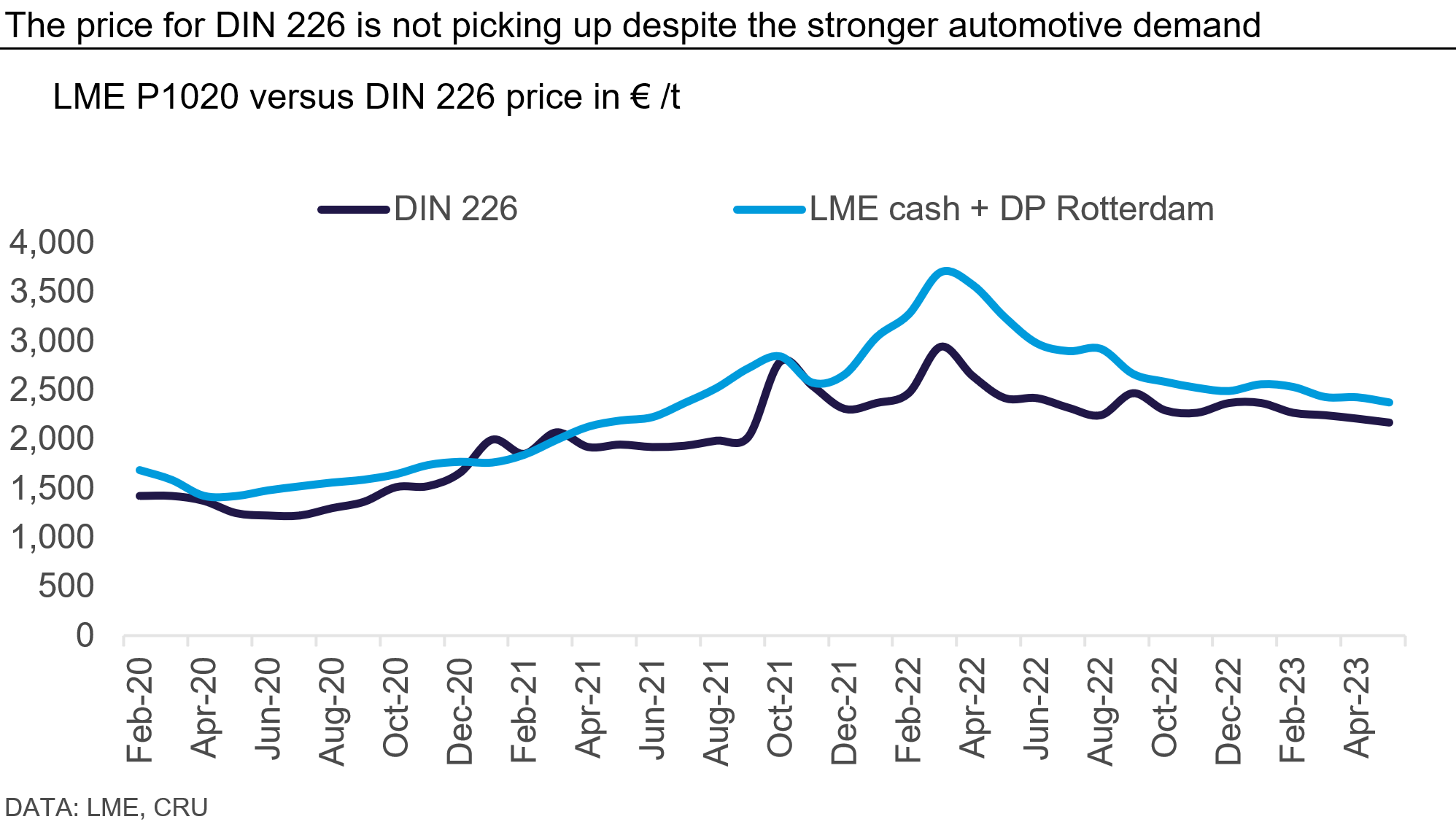

The latest price action on the DIN 226 ingot serves as a counterpoint to the optimistic findings of the ACEA report, casting doubt on the overall health of the automotive sector. The price has slipped gradually since the start of the year and the latest assessment was €2,150–2,200 /t, with some mentioning that most of the deals are being made now at the lower end of this range.

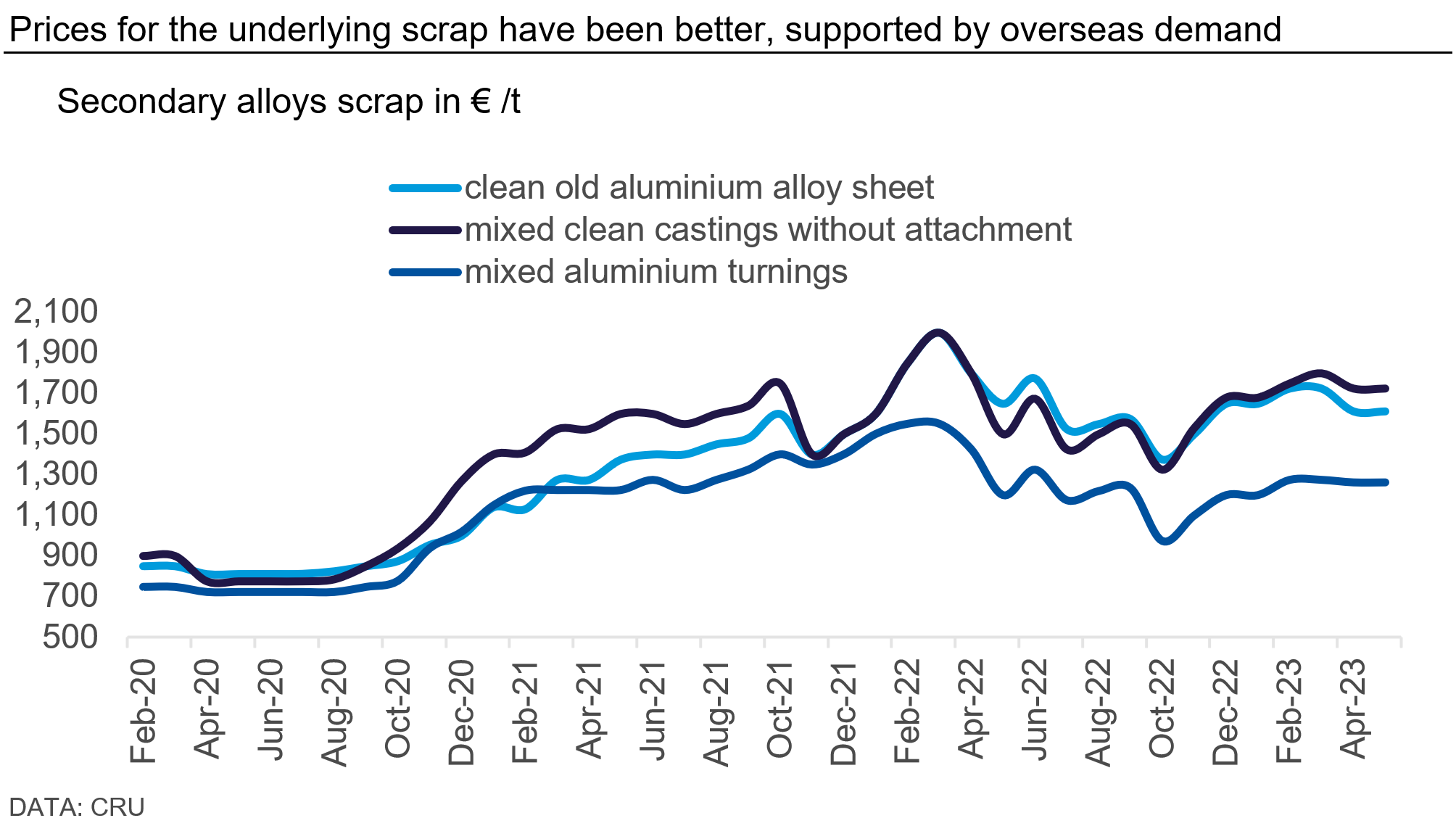

As for the underlying scrap grades, prices have been better supported. Mixed turnings are holding firm at €1,262.5 /t and old alloy sheet and mixed castings are priced at €1,612.5 /t and €1,725 /t respectively, broadly stable since the start of the year. While the secondary ingot market in Europe has become very competitive – with some producers ready to sacrifice some of their margins to win market shares – the underlying scrap grades have benefited from overseas demand, mainly from Asia.

What’s next for European scrap prices?

Availability of scrap should continue to tighten. This is driven by two factors. As demand is not improving, semis producers continue to operate at lower rates and less scrap is coming back to the market. Furthermore, this should be amplified during the summer season as many manufacturers will close for maintenance. Another factor is the low LME price – since it broke an important support line last week, the possibility to see an even deeper correction has increased. In times of lower aluminium prices, scrap dealers are typically not incentivised to offer too much volumes to the market. This also should reduce the availability of scrap.

Nevertheless, the impact on prices should be limited as demand is set to remain weak for some time. Scrap is becoming rarer but so is demand, and it is unlikely that demand will pick up fast enough to spur any tightness in the market any time soon. That extended period of consolidation that we have been seeing for European scrap prices looks well set to continue for a little longer.

Explore this topic with CRU

Author Guillaume Osouf

Head of Aluminium Prices Development View profile