Section 232 came into effect in March 2018 and added a 10% duty to aluminium entering the US. For US consumers, there is an exclusion process for those aluminium products that cannot be sufficiently supplied domestically. Canada, Mexico and Australia are excluded from the tariffs while Argentina, Brazil, South Korea, the EU, Japan and the UK have quota deals put in place. There was recently an announcement that India could have some products excluded as well.

Author Matthew Abrams

Research Analyst View profile

The initial objectives for the duty were to protect the domestic aluminium supply chain and spur on new investments within North America. It has affected every area of the industry from trade flows to premiums, including some unintended consequences.

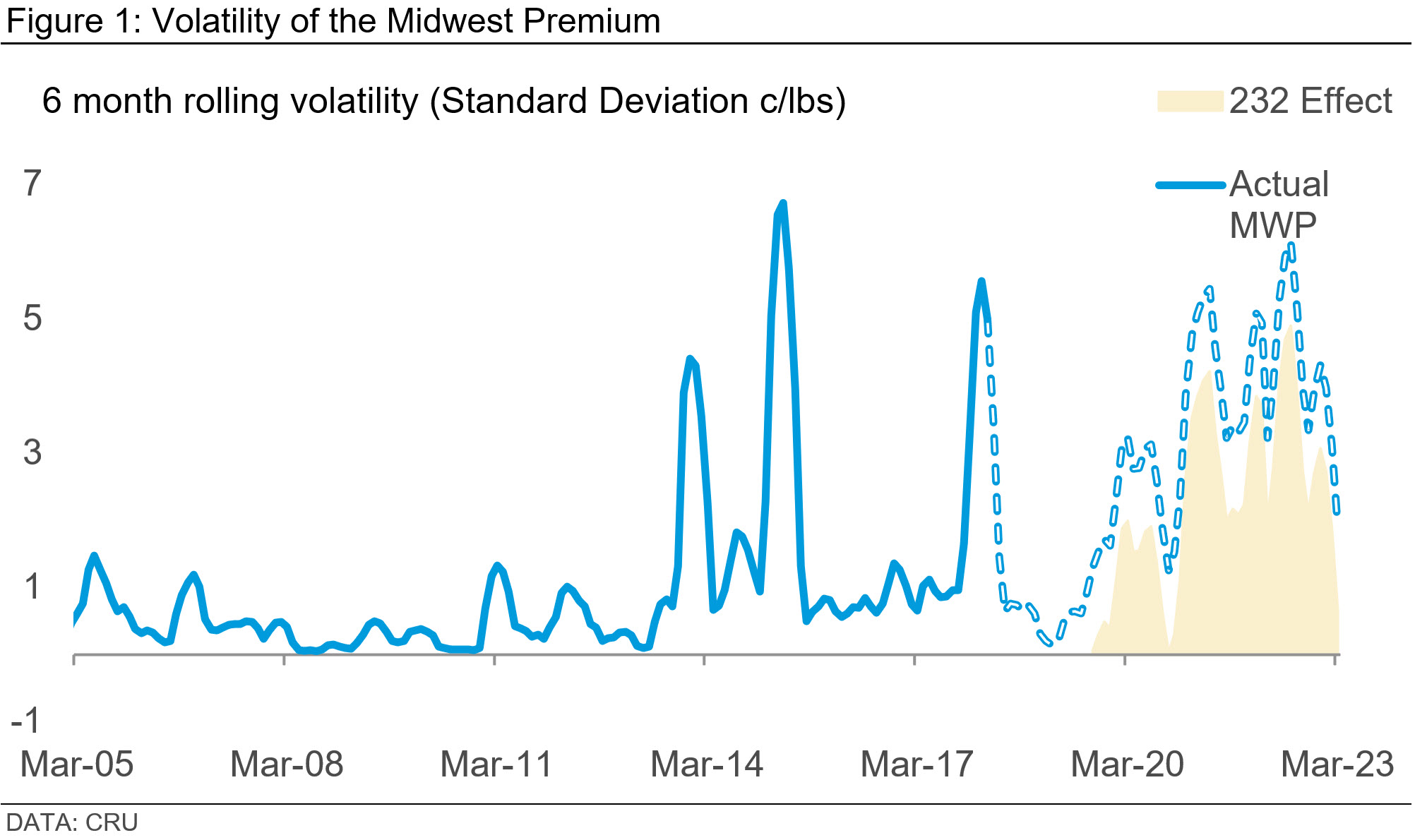

The Midwest premium is more volatile

The Midwest premium has reached historically high levels of volatility. Section 232’s role in this is twofold – it factors LME volatility, and it assesses changes in replacement costs (CIF Baltimore + Duty + Inland freight + Costs of insurance, warehousing) for North American aluminium transactions. By examining a formula for the duty: (LME Cash + CIF Baltimore) * 10%, in conjunction with that for the premium, we can see that any change in ocean freight is captured twice. CIF Baltimore is a main input to the premium and included in that calculation of the tariff.

The chart employs a causal impact model that is typically used to measure the effects of government policies. We measure the pre-232 period and extend a forecast to compare to post-232 under the assumptions that trends and seasonality patterns will remain consistent. The results show that without Section 232, the cumulative standard deviation from 2018 April to 2023 March (total variation over the period) was expected to be between 52 and 102 ¢/lb using a 95% confidence interval. The actual data shows a total variation of 169.38 ¢/lb which is statistically significant and shows that the duty likely had an effect.

It is important to delve deeper into the results. Some of this excess volatility was due to the unprecedented level of geopolitical activity and supply chain disruptions over the past two years. These both directly influenced ocean freight which again, was amplified by the duty applied over that period. There were also much lower LME inventory levels which have been previously linked to higher volatility in regional premiums. While historically there have been sharp peaks and valleys, no period has mirrored the consistently elevated volatility of the last four years.

This makes measuring the exact effects of Section 232 difficult, as there was also unprecedented macroeconomic volatility over that period as well. Thus, the argument here is that the duty did not directly cause this level of volatility, it rather just amplified it.

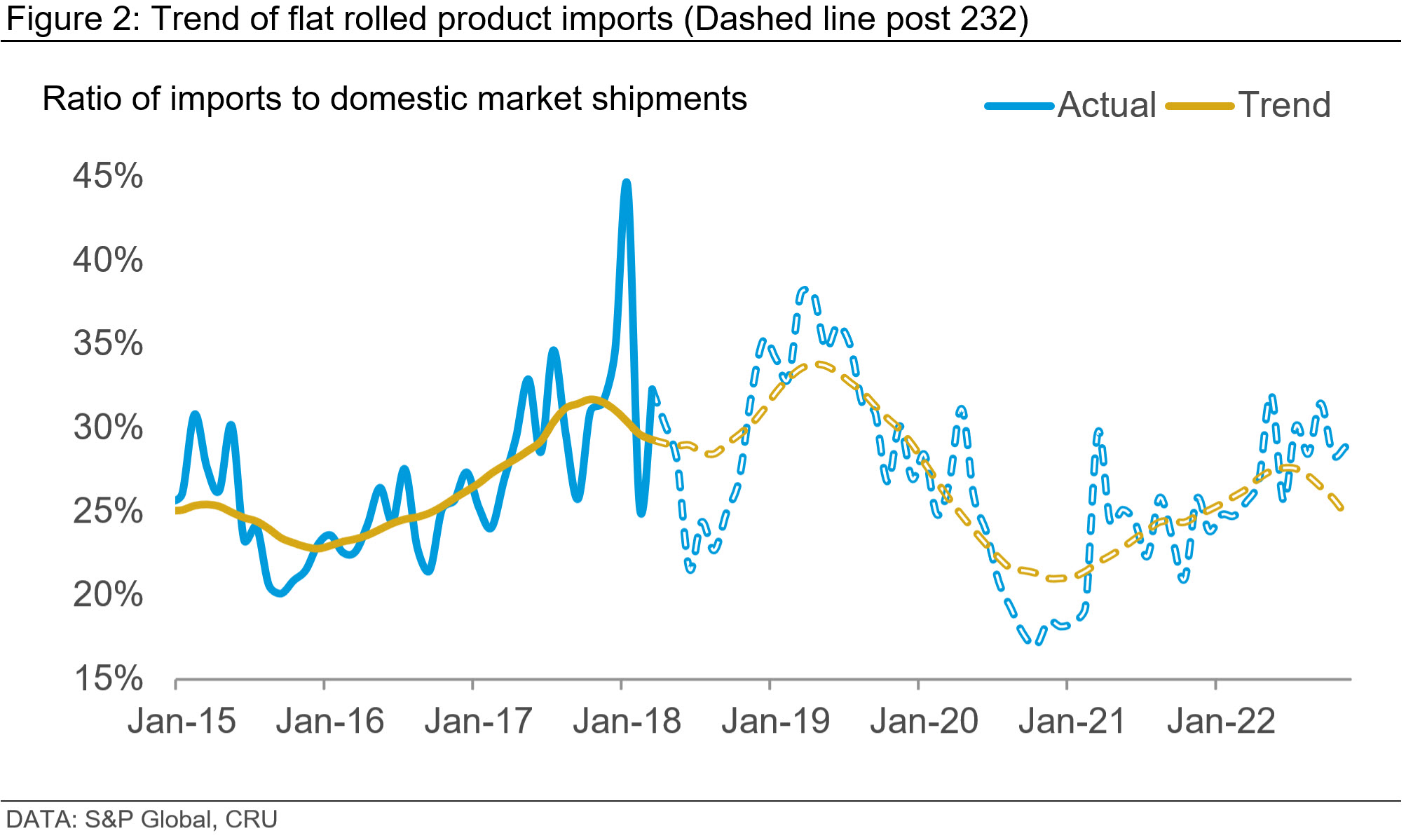

Flat rolled product imports plateaued

The protective effects of Section 232 are most obvious when looking at the flat rolled products market. This is one area of the market where there is both ample protection and an exclusion process that helps downstream domestic producers fill their metal needs. While the effectiveness of the exclusion process is still hotly debated between domestic producers and consumers, overall there was a noticeable direct effect.

Immediately after enaction, imports of FRPs dropped significantly. Even during high growth periods such as 2021–2022, import volumes have not matched the previous peaks. There is also a larger share of imports coming in from domestic producers’ overseas operations, such as Novelis, Korea to Novelis, US or between UACJ/UATH to Tri-Arrows Aluminum.

Probably the most emphatic sign of the positive effects on the domestic market are the new rolling investments. While the three new greenfield investments (the first of their kind in over 40 years) were driven by the growing demand/supply imbalance in North America, the new mills will have to earn market share away from current relationships with overseas producers. This is where the trade protection afforded to domestic producers likely helped spur on further investment.

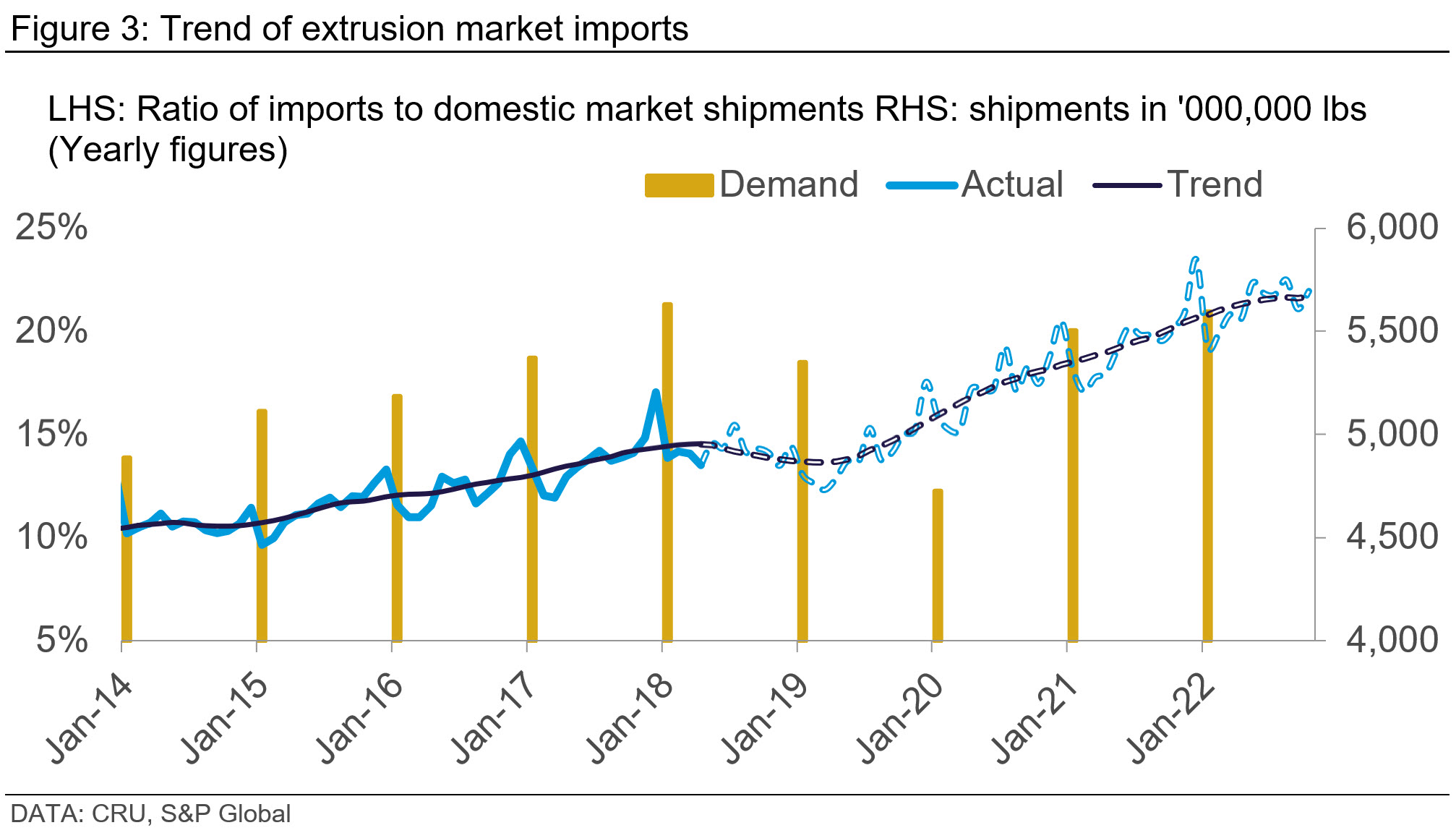

Imports of extruded products gained market share

The juxtaposition of trade flows for extrusions and flat rolled products is immediately apparent. The easy explanation is that extrusions are currently excluded from the Section 232 duty. Instead of the immediate decline as seen above, there was an acceleration of import growth

To understand the total effects of Section 232, it is worth examining the supply and demand landscape. Historically, the last time shipment volumes were as high as last year’s 2,500 kt was 2006. Imports totalled 356 kt that year which is well below the 578 kt seen in 2022. Moreover, almost half of 2006’s import tonnage came from China before trade protections were put into place. There were 50+ more presses in operation at the time domestically.

With the GFC reset of the market in 2008, consumption climbed steadily before peaking again in 2018. Despite demand pulling similar volumes as 2022, imports totalled just over 380 kt. In the 2019–2021 environment with elevated shipping costs, geopolitical uncertainty, and supply chain disruptions, import volumes started to gain market share. This was, of course, directly after Section 232 was put in place. Imports also now come from a wide range of producers and are continuing to gain market share. The largest increases were from Colombia, Vietnam, Turkey, China and Mexico.

The effects of 232 reach beyond just the lack of protection for domestic extruders. Currently extruders outside of the US, such as Mexico, can import billet without the duty applied and then turn around and export finished extrusions into the US again duty free. Other forms of trade protection also tend to miss extrusions. For example, the recently put in place rules of origin for the Build Back Better act do not cover aluminium, with B&C being one of the largest end use markets.

Again, the most visible indication of the policy’s potential effects is the increase in new domestic investments. While there has been a host of new announcements, extruders are choosing to invest in the Southwest region of the US with several potentially moving further into Mexico.

Section 232 unlikely to be removed

Since 2018 aluminium consumers have had to factor this pass-through cost into their supply expectations. For large volume consumers, as the aluminium beverage can value chain, exclusions have buffered the net effect. These economic effects of 232 have been analysed extensively since its inception and each Congressional hearing concludes that the benefits for domestic producers outweigh the costs. These benefits, however, are not shared equally domestically speaking, and have spillover effects on importers and costs too.

With the war in Ukraine and other regional tensions growing, geopolitical risk remains elevated. Adding strategic supply chain security and supply chain disruptions during the pandemic gives more weight to the focus of onshoring or friend-shoring. Adjustments, however, are still on the table similarly to the recently announced easing of duties on aluminium coming from India and potential changes to the exclusion process.

Explore this topic with CRU

Author Matthew Abrams

Research Analyst View profile