The FY24 budget for India is overall positive for the steel sector as focus remains on investment-driven growth, with major spending plans being steel-intensive. External factors which affect global oil prices, however, may throw a spanner in the works.

While high capex allocation is a positive for the longs market, greater focus on increasing domestic manufacturing will support sheet demand. Moreover, a greater renewable push will help plate demand.

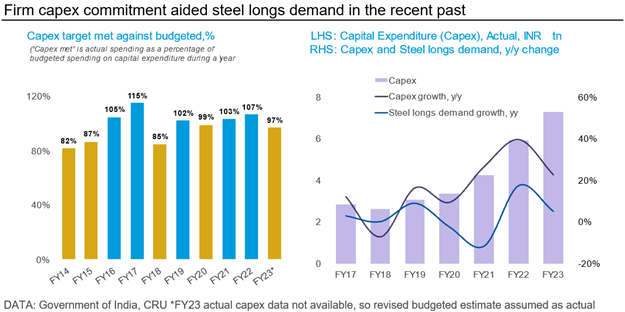

High capital expenditure to help support longs demand

In its annual budget for FY 2023/24 (1 April 2023 – 31 March 2024) the government of India allocated a capital expenditure budget of $120 bn. This is 33% higher than the previous budget and points to stronger steel demand growth. Historically, we have witnessed a strong correlation between longs steel demand and budgetary spending by the government.

As evident from the chart above, the government has been consistent in achieving its capital expenditure target since FY 2019. Barring the effect of Covid-19 and related lockdowns on Indian economic activity during FY 2021, a higher capital expenditure by the government has aided growth in overall steel longs demand. With the capital expenditure expected to rise by 33% y/y, Indian steel longs demand will rise in the range of 7–10% y/y going by past trends, compared to CRU’s pre-budget forecast of 2.1% y/y growth in FY 2024. This translates to at least 2.5 Mt increment in FY 2024 longs demand over CRU’s pre-budget forecast.

Through this high capex allocation, the government is focusing on investment-led growth. There are, however, risks to this arising from a tighter fiscal space for the country. As funding for the projects will be available provided the government meets its revenue target, there are associated risks.

This may prove to be challenging, owing to upward risks around energy (specifically crude oil) prices, and a general slowdown in global economic growth leading to slower Indian exports – of both goods and services. Limiting the increase in government debt will also depend on successfully privatising assets – an area where the government is running behind its targets.

Localisation of manufacturing bodes well for sheet demand

The focus on investments – particularly in upgrading, renovating and expanding physical assets – means that the intent of the government is to achieve a broad-based pick-up in economic activity, which is expected to lift the overall consumption cycle. This – coupled with support being provided for the manufacturing sector through various localisation measures, be it the extension of the PLI scheme or increased domestic share in defence procurement – will encourage the private sector to invest in related expansions, which is positive for sheet demand.

Emphasis on renewables can boost plate demand

The Ministry of New and Renewable Energy (MNRE) has got budgetary allocation of $1.2 bn which is 48% higher from the previous budget. In 2022, the solar capacity addition was hindered by new import tariffs on solar cells and solar panels which was in effect from 1 April 2022. India has missed the target of building 100 GW installed solar capacity by end-2022 by a large margin of 37 GW and was able to achieve only 63 GW installed solar capacity – as large projects were delayed because of higher tariffs on imports of solar cells and panels.

Higher allocation of budget for MNRE for FY 2023–24 may incentivise the delayed projects and new renewables projects, which will lead to higher consumption of steel plates.

The Hydrogen Mission requires increased focus on decarbonisation

Budget outlay of $2.5 bn has been announced for the green hydrogen mission. Its aim is to produce 5 Mt/y green hydrogen by 2030 and gradually replace the use of fossil fuels by industries like steel, transport, shipping etc. However, the immediate focus is for India to become one of the largest exporters of green hydrogen in global space. Forward plans for the use of green hydrogen technology to decarbonise the Indian steel industry are limited. The current focus is more on replacing coal-fired electricity through renewables generation.

We estimate the cost of DRI production using green hydrogen will be more than double than that of coal-based DRI. The cost of hot metal production through green hydrogen will be more than 1.5 times that of PCI injection-based hot metal.

India's Green Hydrogen Mission is ambitious, but the government support promised will not be sufficient to encourage the rapid development of green hydrogen capacity at this time. As a result, additional policy support will be required to ensure success. This could take the form of much higher levels of subsidy, mandated use of green hydrogen, or some form of carbon tax to raise the cost of traditional energy sources. The latter options would also require additional market protections. Without this additional policy support, the use of green hydrogen in difficult-to-abate industries in India will remain challenging.

You can also read India’s Green Hydrogen Mission: Practicality from a cost perspective

We will be quantifying the impact of the budget on the Indian steel supply chain – from raw materials to finished steel – in the subsequent market outlooks. Get in touch if you would like to learn more about this topic.

Explore this topic with CRU