In March 2019, after the merger of Barrick Gold and Randgold Resources was completed, CRU analysed what appeared to be the beginning of a new era of consolidation in the gold industry. With the recent announcement of a proposed deal for the takeover of Newcrest Mining by Newmont, the M&A trend continues. CRU has taken a further look into this potential merger and the potential implications for the future of the industry.

Author Alex Christopher

Senior Analyst - Aluminium View profile

Author Kirill Kirilenko

Senior Analyst View profile

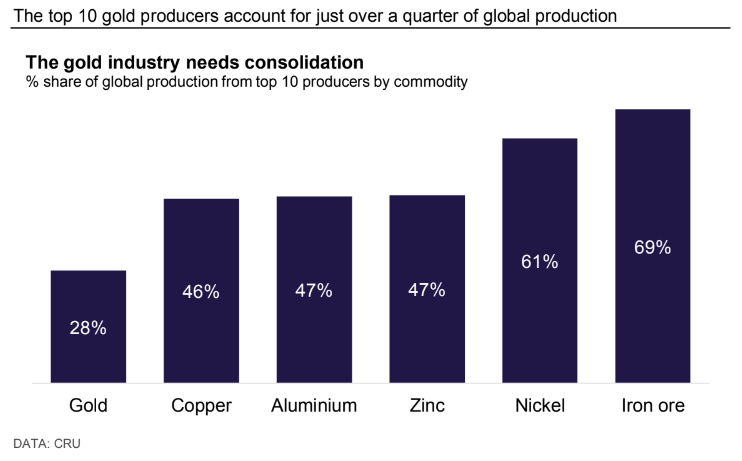

Gold mining is a highly fragmented industry

Gold is one of the most fragmented mining industries. Low barriers to entry, technological innovations to process difficult ores at economical costs, and the ability to remain profitable at small scales have allowed for many companies to enter the industry with relative ease. In most mining and metals industries, the top 10 producers account for nearly 50% of global production – for gold, the top majors produce less than 30% of total global output.

Major gold producers look to grow and expand in different ways. While many favour organic growth by financing exploration endeavours – using capital to explore for new resources which can potentially be developed into the next big gold project – this can be a risky and expensive venture. This is particularly true in times of market volatility, geopolitical uncertainty and increasing resource nationalism.

Hence, many gold producers look towards mergers and acquisitions. Industry consolidation allows miners to increase their production share, replenish depleting gold reserves, and improve synergies between operations to lower production costs through relatively less risk. Additionally, there are cases where M&A also leads to metal diversification, as the acquired/merged mines contain mineral by-products. Ultimately, the goal of M&A will be to add value by increasing revenue, particularly in high price environments, and extend a portfolio’s mine-life.

In the last five years, the gold industry has seen a number of large deals which have helped consolidate the industry. In 2019, the two current largest gold companies were formed when Barrick merged with Randgold and shortly after Newmont acquired Goldcorp. In the same year, Newcrest entered a JV with Imperial Metals to own 70% of the Red Chris copper-gold mine in BC, Canada. Since then, we’ve seen the $10.6 bn Agnico Eagle and Kirkland Lake merger completed in 2022, which created the current third largest gold producer. In early 2023, Pan American Silver’s approved acquisition of Yamana Gold will see Pan American Silver acquire Yamana’s LATAM assets, while Agnico Eagle will acquire the 50% share of the Canadian Malartic gold mine which it didn’t already own. Yet perhaps the biggest deal announced since the 2019 mergers of majors is Newmont’s potential acquisition of Newcrest.

Newcrest acquisition targets safe investment over low cost

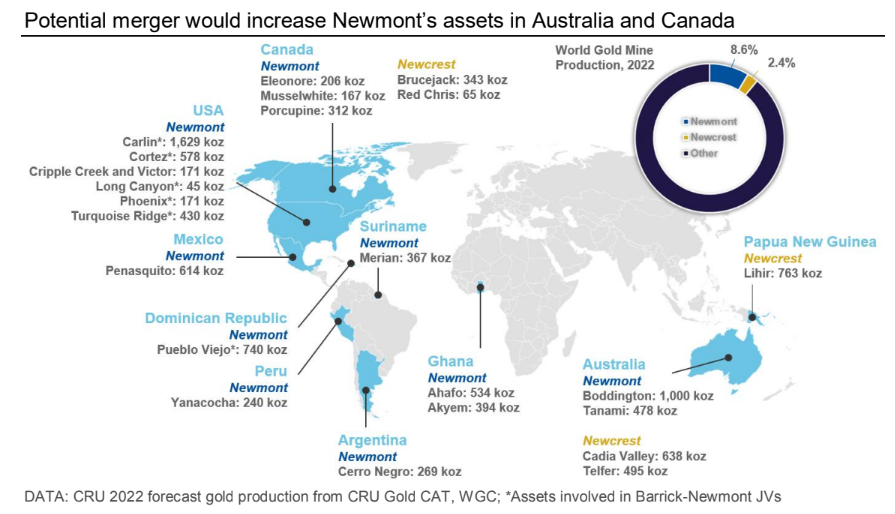

The potential $17 bn acquisition of Newcrest by Newmont would create a gold mining company with global reach that includes 23 mines in 10 countries. If successful, the acquisition would increase Newmont’s production base by 48% to ~9 Moz of gold per annum and, through assets like Cadia Valley, Telfer, and Red Chris, the company would expand its access to copper, a metal highly in demand due to its key role in the green energy transition.

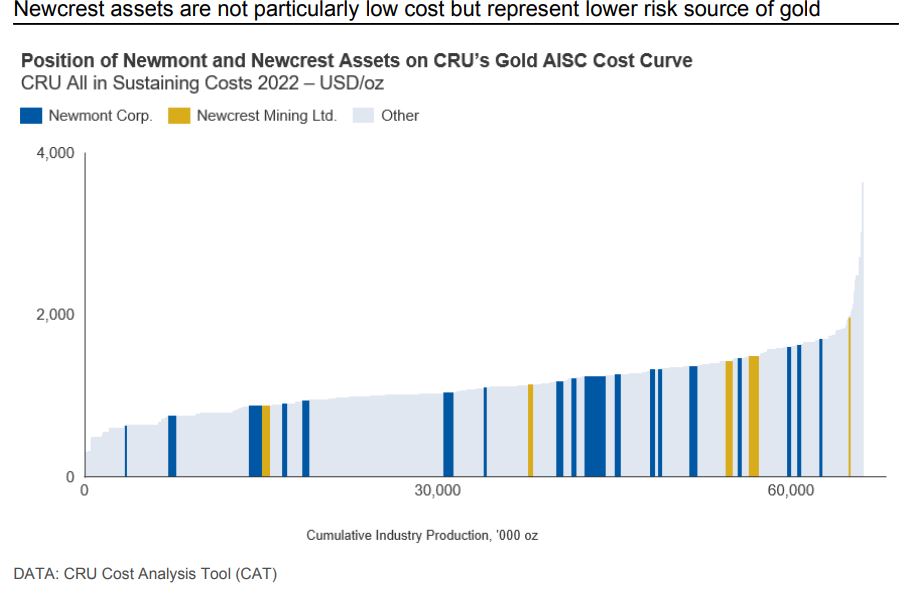

Newmont’s interest in Newcrest appears to stem from the location of their assets and size of their resources. Four of Newcrest’s five producing assets are in Australia and Canada, traditionally considered Tier 1, safe mining jurisdictions. Recent years have seen increasing geopolitical tension, resource nationalism and social licence issues which complicate operations for international mining companies. Acquiring companies and assets in safe jurisdictions makes business sense for larger companies that can cope with the slightly higher costs these jurisdictions entail.

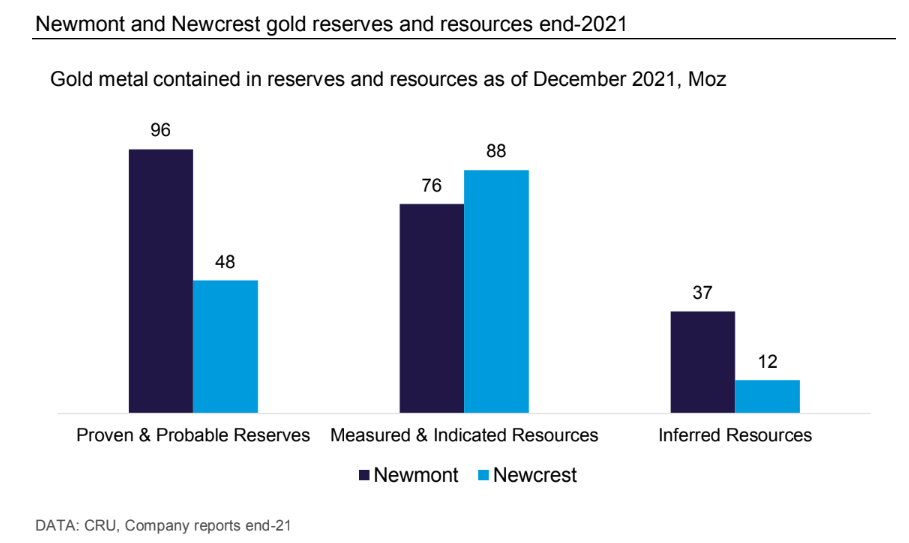

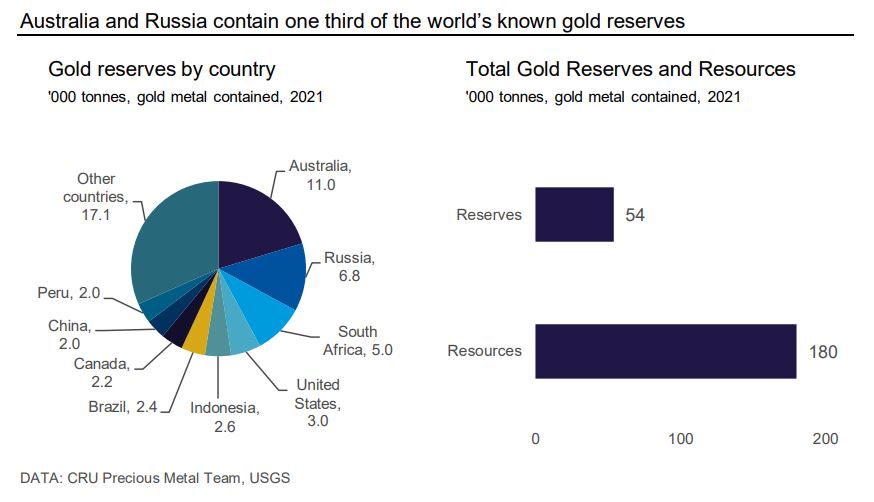

On top of this, Newcrest’s gold tenements and reserves would increase Newmont’s operational Proven & Probable gold Reserves by 50% to 144 Moz, based on 2022 Reserves and Resources statements. Meanwhile, the enlarged gold miner would see its Measured, Indicated and Inferred gold Resources almost double from 113 Moz to a total of 213 Moz. Newmont will also be interested in Newcrest’s Measured and Indicated copper Resources rising from 19 Mt at the end of 2021 to 25 Mt reported in August 2022.

Gold reserves and resources are globally spread with the top four countries with the largest known gold reserves including Australia, Russia, South Africa and the USA. Geopolitical issues complicate or bar investment in Russian gold production while continued power availability and political issues continue to hinder South African gold resource development. Large Australian gold reserves, therefore, are a relatively safe investment for a gold mining company looking to secure its project pipeline and future gold production.

Mine supply growth has been limited since 2001

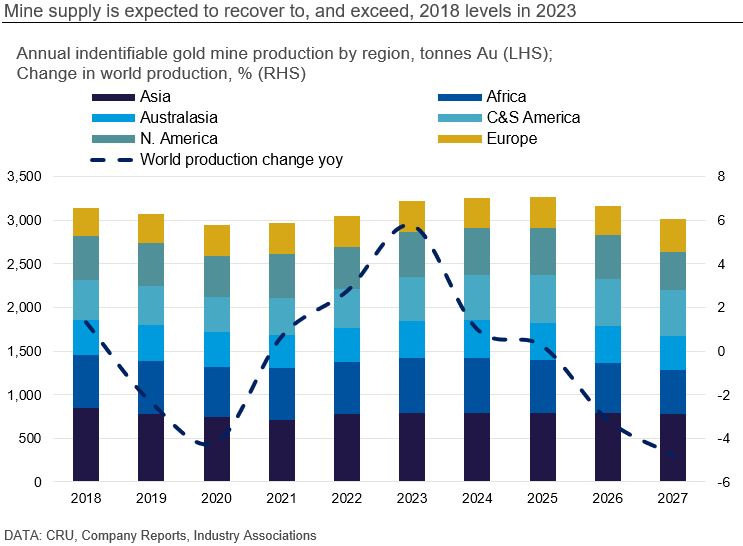

According to CRU, total world identifiable mine supply (mine supply which excludes artisanal, illegal, and state secret gold mining) increased from 2,547 t in 2001 to 3,045 t in 2022. This equates to a CAGR of 0.9% over the period. Most importantly, growth was driven by net increases in Chinese, Russian, and Kazakh production whilst South Africa and the US registered the largest country production declines.

As a group, Chinese, Russian, Kazakh gold production as share of global output increased from 14% to 24% during this period whilst US, Canadian, Australian, and South African supply has fallen from 46% to 26% over the same period.

It is difficult for investors to gain access to Chinese and Russian gold exposure, and mining companies with operating assets in Rest of World jurisdictions have become larger players in a smaller pool. This issue has been compounded by the ongoing Russia-Ukraine war.

CRU expects this to continue in the medium-term

Geographically speaking, gold mine production is particularly diverse. Given the global spread of gold mining, supply is less susceptible to regional shocks and is therefore far more stable than several other metals. For example, in 2020, the top ten gold producing nations only accounted for ~56% of global gold production – this is a relatively small figure compared to metals like copper and zinc which source around 80% of their supply from the top 10 producing countries.

CRU forecasts identifiable gold mine production to reach 3,045 t in 2023, a 2.85% y-o-y production increase from 2022. This is due to combined increases in output from Latin America, Australia, Russia, and Africa, offsetting declines from Asia. CRU expects mine production to grow for three more years, rising to a peak of peak 3,261 t in 2025, before falling back as growth in North America and Australia gives way to contraction, while the downtrend in African production accelerates.

Indicators are flashing green for the gold price

After a sharp surge in 2020, gold price performance was muted in 2021 and remained essentially flat in 2022. However, bullish sentiment is expected to return to the gold market as soon as this year.

Against the backdrop of the weakening US$, high (but not red-hot inflation), rising recession risks and simmering geopolitical tensions, gold is likely to boost its safe-haven appeal and embark on an upward trend in 2023. The prices are expected to continue to rise in the short to medium term on the back of anticipated cuts in interest rates as the Fed is expected to reverse course on its monetary policy, from contractionary to expansionary, sometime next year, according to CRU’s senior precious metals analyst, Kirill Kirilenko.

Gold prices are an important driver of M&A activity in the gold mining industry. Strong prices provide a favourable backdrop for prospective buyers as they tend to boost their cash flows and improve profitability which in turn increase their financial power and investment appeal. However, transaction prices also begin to rise along with valuations of prospective targets, meaning that the companies keen to secure reserve growth and future production through M&A transactions, need to make their move long before a new bull market is in full swing.

More in-depth analysis on gold price expectations can be accessed by subscribers to CRU’s Precious Metals Service here.

Successful mergers will further drive asset sales and pressure for consolidation

Shareholders will decide the future of Newmont and Newcrest over the coming days and weeks, but many others will watch the companies and structures that emerge with interest.

In all scenarios CRU expects asset sales as non-core assets are removed. This will create opportunities for other miners to add to their gold portfolios. More importantly investors will look for evidence that the gold sector can optimise operational costs, deliver sustainable margins, and increase shareholder value through consolidation. If this were proven, expect further pressure to consolidate in the gold sector.

Explore this topic with CRU

Author Alex Christopher

Senior Analyst - Aluminium View profile

Author Kirill Kirilenko

Senior Analyst View profile