Coal mining heavyweights have been busy optimising their coal holdings to reflect desired exposure to coal. In recent weeks, Glencore has proposed to merge with Teck Resources, pitching its plan as a superior alternative to Teck’s own demerger plans for its coal and metals businesses. This offer has been swiftly knocked back by Teck’s board and major shareholders.

Apart from creating synergy and shareholder value, Glencore seeks to elevate its position in both base metals and metallurgical coal supply through this proposed merger. Meanwhile, metallurgical coal majors Teck Resources and BHP are independently charting their own paths to align their metallurgical coal portfolio with their energy transition strategy.

Metallurgical coal M&As fuelled by high profits and ESG pressures

At the start of 2023, BHP confirmed it was seeking potential buyers for its Blackwater and Daunia mines, which exist within the BMA portfolio. This decision is likely driven by the desire to continue reducing BHP’s exposure to coal, prioritise higher coking coal grades within its steelmaking coal portfolio, and simply a well-timed divestment at the top of the business cycle.

Metallurgical coal-heavy business model drives portfolio polarisation at Teck Resources

In February, Teck Resources announced its intent to split the company into two new independent companies focused on different commodities:

- Teck Metals Corp. – focused on base metals to serve the energy transition

- Elk Valley Resources Ltd. – focused on steelmaking/metallurgical coal

This development has been years in the making. Teck Resources CEO Jonathan Price cited a ‘strategic and financial focus’, ‘ability to pursue tailored capital allocation strategies’, and that the company is providing shareholders choice in an ‘evolving investment landscape’.

Teck’s split was scheduled to go to a shareholder vote on 26 April, but this vote was cancelled at the last minute. CEO Price cited shareholders preference for a ‘simpler and more direct separation’ as a key reason to cancel or postpone the shareholder vote. This is in reference to the original separation plan whereby the proposed coal business (Elk Valley Resources) would continue paying royalties to the metals company (Teck Metals).

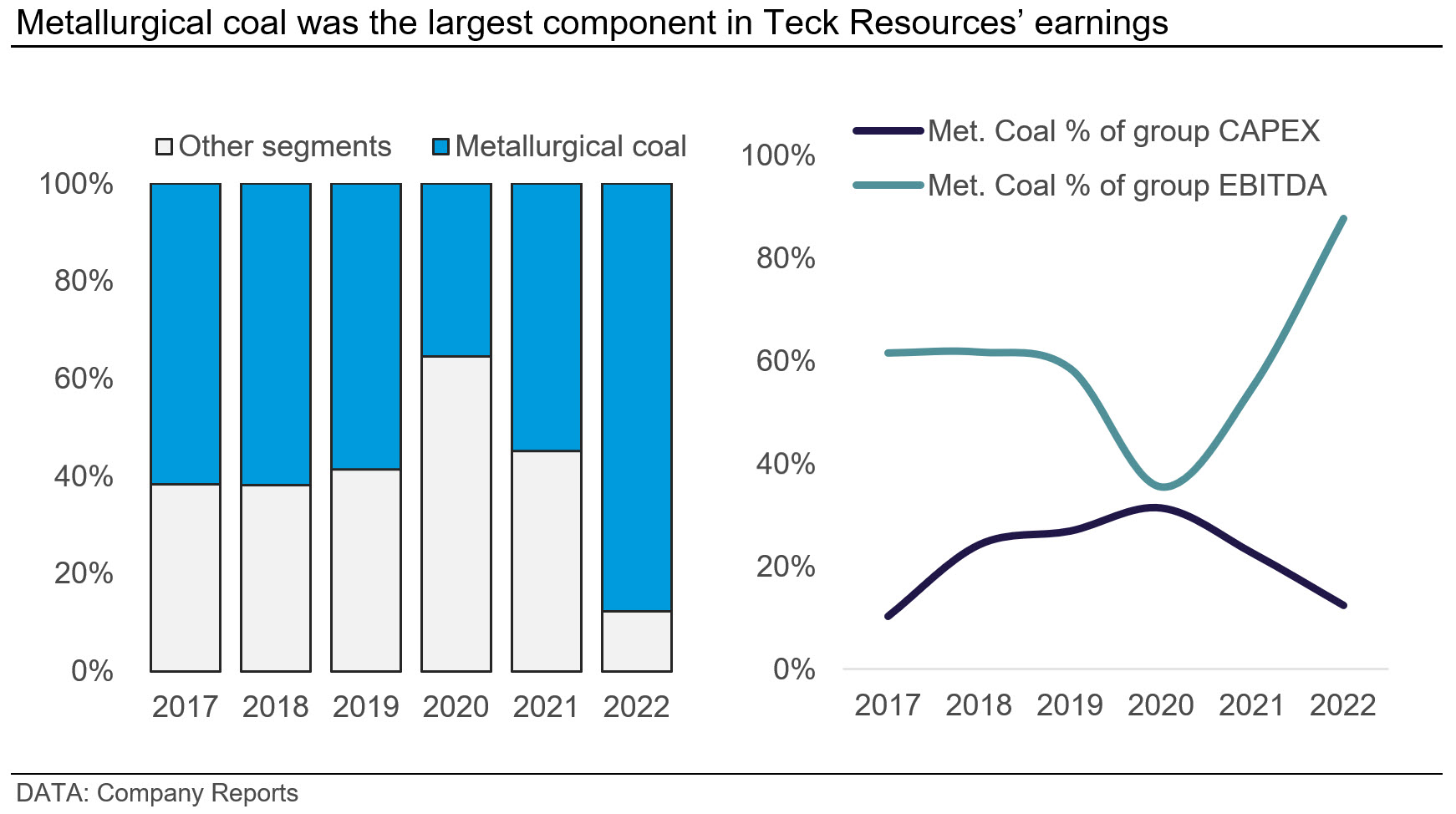

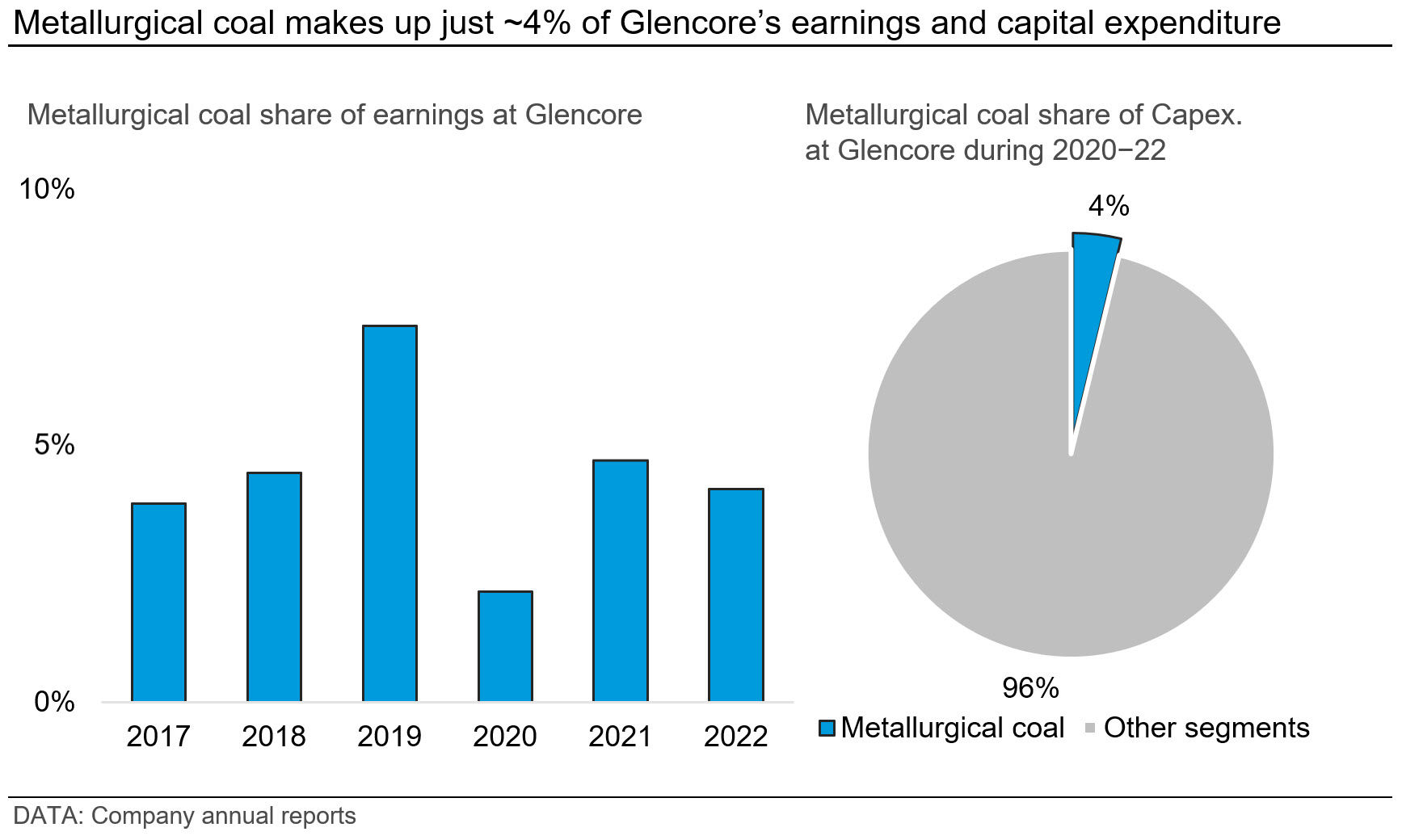

Steelmaking coal has contributed to ~60% of Teck’s EBITDA over the past five years, in contrast to BHP where coal contributed to ~20% of their earnings since 2017, while requiring less than 10% of group capex over the same period. Metallurgical coal makes up only 4% of Glencore’s earnings. Much like BHP, the share of profits generated by Teck’s metallurgical coal business has far exceeded the share of capital spend on the segment.

In our view, the relatively large proportion of current earnings by Teck’s steelmaking coal arm poses challenges for the company until its base metals output and cashflow increase. Ultimately, ESG still drives Teck’s desire to split the portfolio between energy transition and growth-focused base metals business (including copper); and metallurgical coal – a transition enabling commodity which is likely to see accelerated decline during the later stages of the energy transition.

Metallurgical coal asset ownership is increasingly conditional upon high medium-term cash generation. Teck’s coal and metals businesses represent two polarising ends of the energy transition. This move by Teck somewhat transfers the decision on ownership and capital allocation to shareholders while executives focus on pursuing the business objectives.

This contrasts with BHP’s metallurgical coal holdings, which are larger in absolute volume and higher in quality but are a relatively smaller portion of earnings. BHP’s steelmaking business can be seen as a diversified holding on to high-quality world-class assets in a commodity with high barrier to entry. Nonetheless, BHP continues to balance the medium term high expected cashflows with ESG and energy transition risks.

Glencore has the smallest relative exposure to metallurgical coal

Glencore is a diversified mining and trading powerhouse with operations spread globally across oil & gas, metal and mining, energy and agriculture sectors. Metallurgical coal makes up a small portion of Glencore’s earnings (4.4%) and capital spend program (3.9%).

Glencore has historically been a major player in the thermal coal market with production volume close to 100 Mt/y and additional marketing rights to third party volume making up ~20% of the global seaborne thermal coal market. Glencore’s thermal coal business generates about 50% of its earnings. The miner has outlined plans to cap thermal coal production and eventually run down asset reserves. Nonetheless Glencore faces increased scrutiny from investors to explain how its projected coal production aligns with Paris agreement principles.

Glencore’s proposed acquisition of Teck Resources will allow the company to increase its share in the metallurgical coal market. This proposal could be as much about replicating its thermal coal success as it is about increasing exposure to a more acceptable asset class from an ESG perspective.

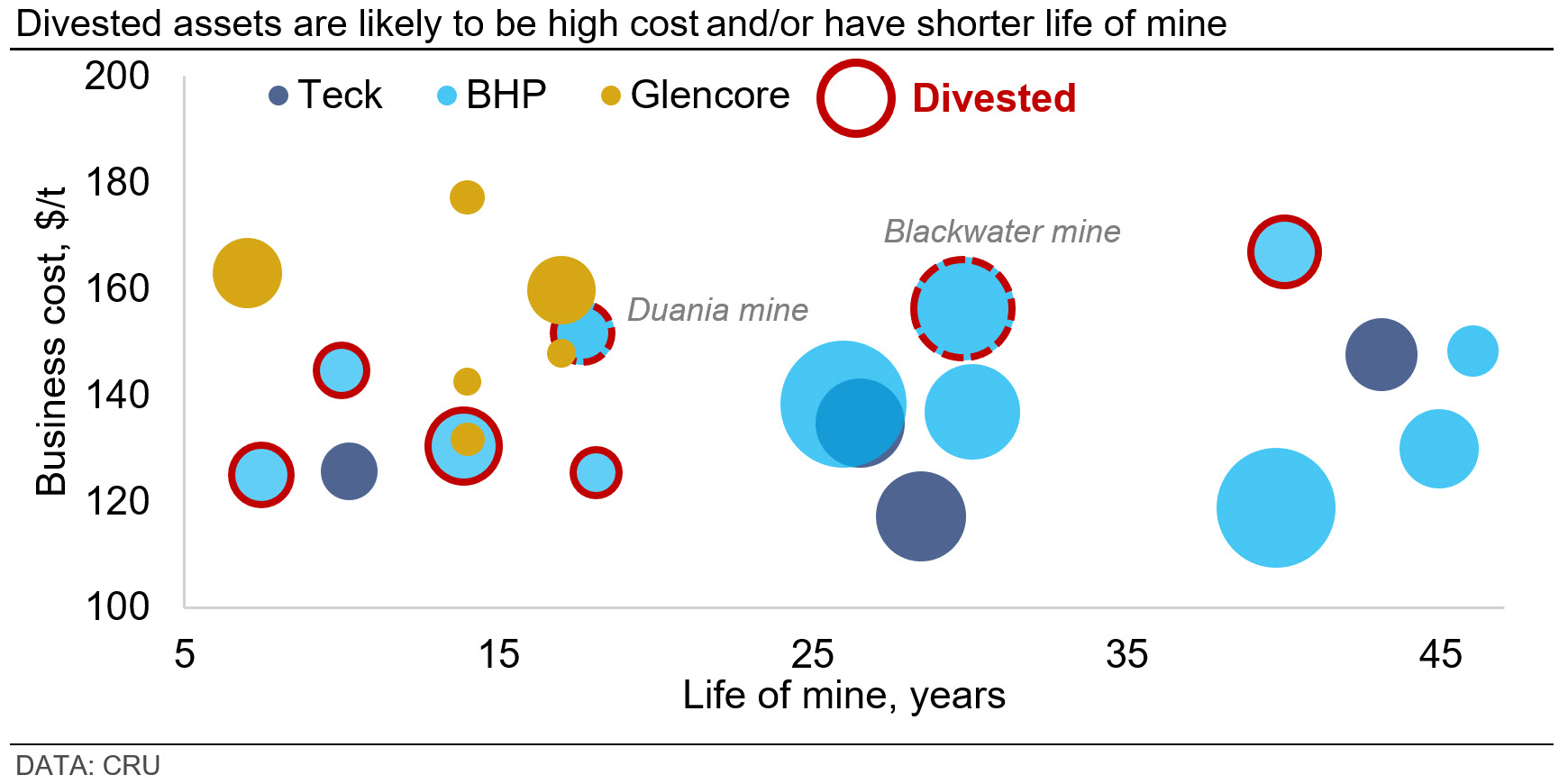

Divested assets have higher costs, shorter mine life

BHP’s recent sale of the BMC portfolio (South Walker Creek, Poitrel, Wards Well) allowed it to offload higher cost and shorter mine life assets relative to its prime BMA assets.

The average Business Cost of the sold BMC portfolio is estimated to be $142 /t for premium HCC FOB Australia, and costs for the on-sale Daunia and Blackwater assets are estimated to be $155 /t. This compares with ~$132 /t for its prime BMA operations. These costs are adjusted for coal quality and value-in-use (VIU) and expressed in nominal terms for 2025.

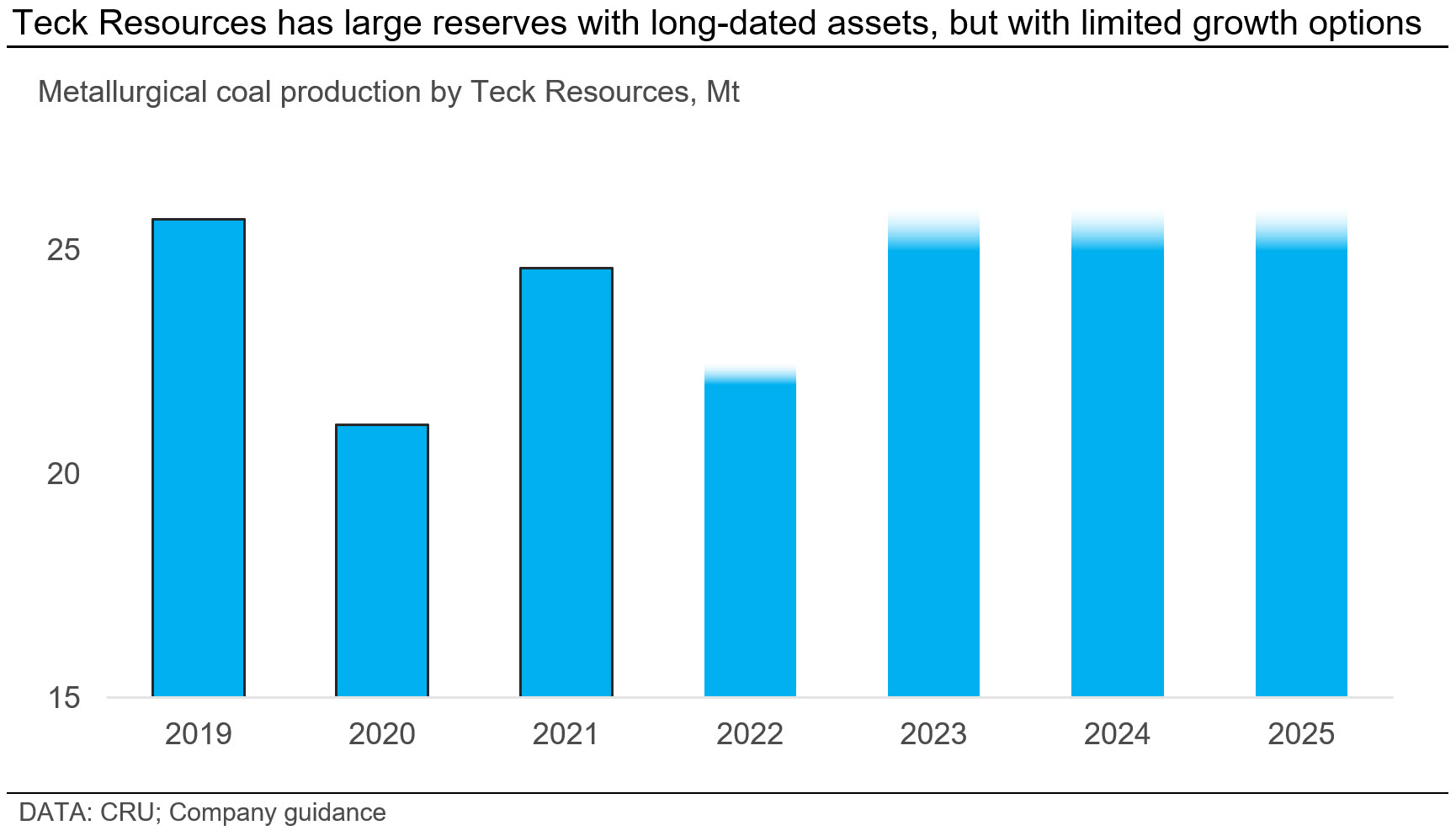

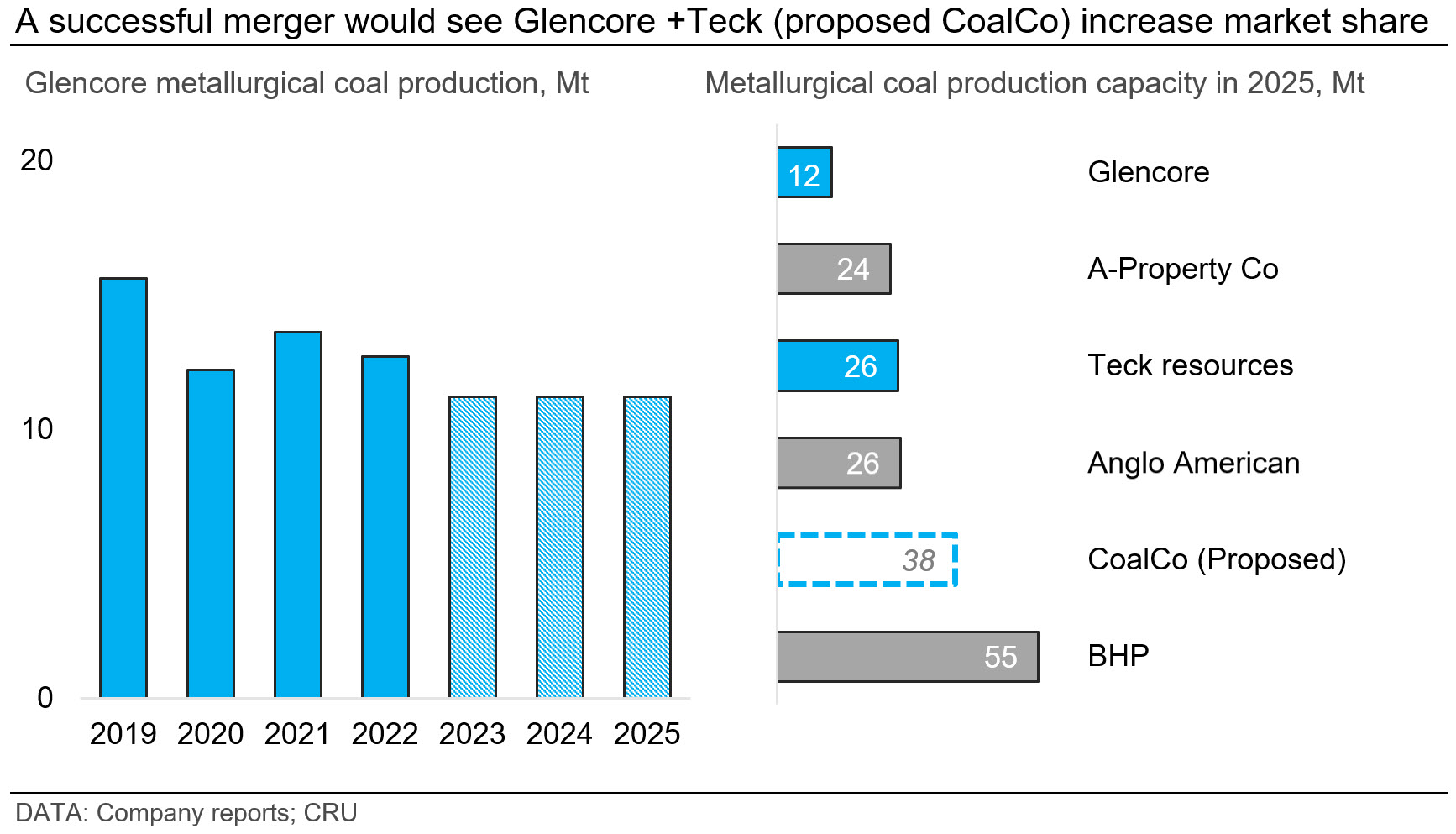

In comparison, the business cost for Teck mines is lower (except Greenhills), and most of Teck’s mines run beyond 25 years mine life, with saleable reserves at Greenhills extending its life of mine beyond 40 years. Acquisition of these assets would complement Glencore’s existing holding of short mine life assets which are a combination of near-benchmark quality and off-spec coking coal.

Glencore’s metallurgical coal assets are generally high cost and short mine life. A successful merger with Teck would elevate the miner’s position to become the second largest metallurgical coal exporter in the seaborne market. The combined entity would control a mixture of long dated, low-cost premium assets based in Canada and a mixture of smaller Australia-based assets. The proposed merger would more than double Glencore’s exposure in the premium hard coking coal market where it would be able to market ~25 Mt of higher CSR premium HCC from Elkview, Greenhills, Hail Creek and Oaky Creek mines.

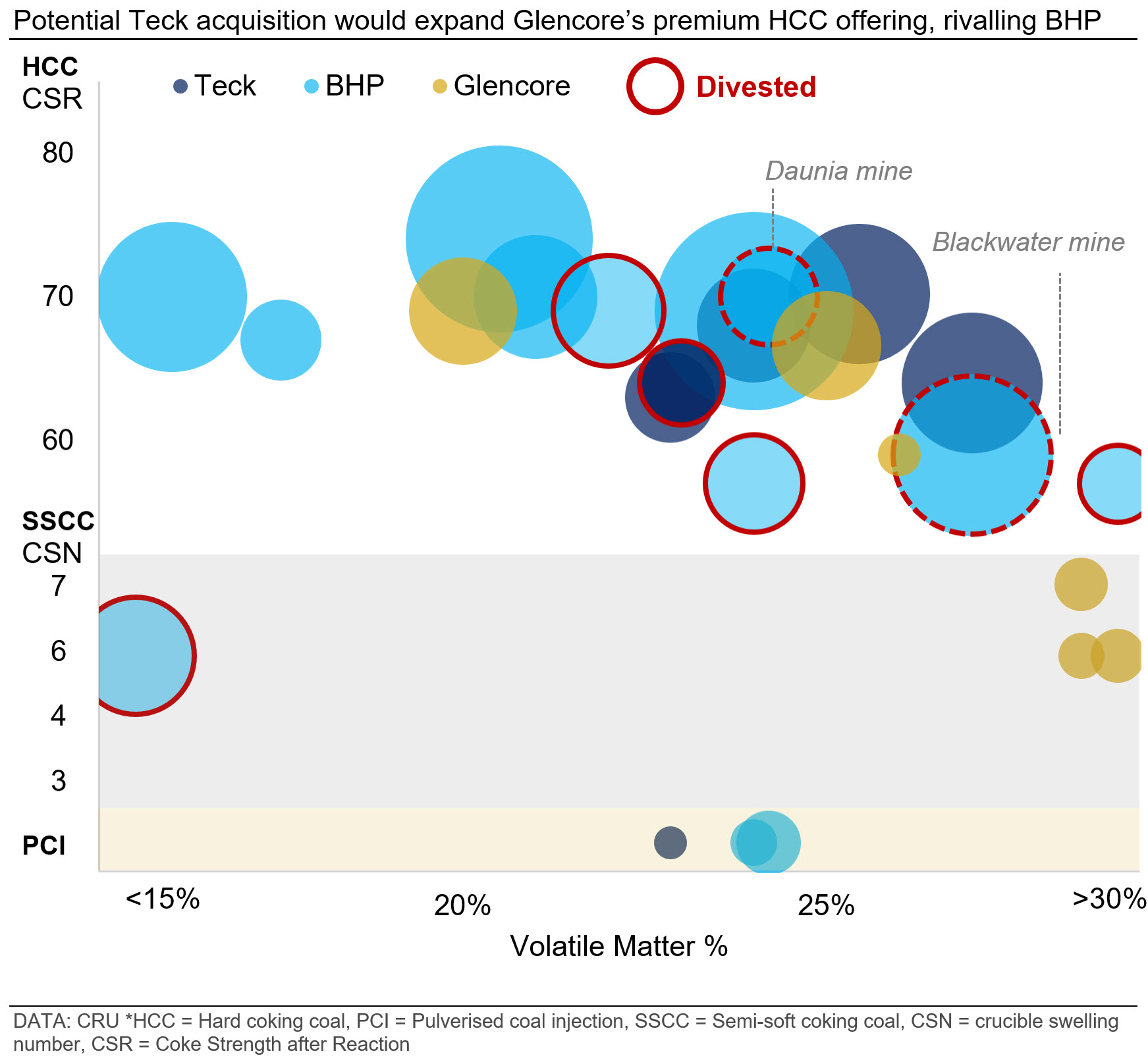

Divested assets are discounted to benchmark quality HCC

BHP’s mines under divestment generally produce HCC, SSCC and PCI at a quality which attracts a discount to the premium hard coking coal benchmark. Canadian (and US) HCC generally has higher volatile matter than the benchmark premium quality coking coal from Australia. Already divested BMC assets from BHP have produced lower CSR coking coal, except for Wards Well where it is likely coking coal will have near benchmark quality CSR. Daunia coking coal is also of high quality in terms of CSR but carries high volatile matter of ~24%. Blackwater HCC is high in volatile matter and has low CSR, which explains the steeper penalty pushing its quality adjusted business costs higher.

Rationalisation of metallurgical coal portfolio to continue

M&A activity in the metallurgical coal sector remains at high levels fuelled by a sustained period of high profits. As ESG pressure continues to mount, miners will need to re-evaluate their coal asset exposure. The case of BHP thermal coal wind-down and met. coal asset sales; and the potential splitting of Teck, act as two more recent examples of strategies to align with the goals of the transition. Stanmore coal was born out of BHP’s BMC divestment. Yancoal has also been rumoured to be a front runner in the purchase of Blackwater and Daunia, although the list of suitors keeps growing.

Some approaches have not been successful. For example, Peabody and Coronado coal recently engaged in merger talks which ultimately failed. The two majors reaffirmed their commitment to grow their annual volume via acquisitions.

These developments reveal the nuanced differences in philosophy and the challenge that lies ahead for long-term metallurgical coal producers. Investors and other stakeholders will look for evidence that producers can balance competing priorities across ESG, commercial imperatives and navigating technological change during the energy transition.

If the Glencore proposal for Teck Resources succeeds, this may be the starting shot for more intense M&A propositions and divestments. Even in the event that Glencore’s proposal fails, Elk Valley Resources will re-emerge as the second largest seaborne exporter of metallurgical coal. This in itself is precedence for further restructuring within the industry.

Explore this topic with CRU