After years of supressed deal flow and merger & acquisition (M&A) activity, fertilizer companies are now seeing a flurry of transactions. Vastly improved cashflow and a more positive long-term outlook for the industry underpins this. In this Insight, we analyse the recent and upcoming deals.

Author Chris Lawson

Head of Fertilizers View profile

Fertilizer earnings soared in 2022

Fertilizer prices reached multi-decade highs in 2022. High natural gas prices, Russia’s invasion of Ukraine, sanctions on Belarus and strong agricultural commodity prices all contributed to soaring returns for fertilizer producers. Publicly traded companies have maintained a disciplined approach to managing improved cash and capital flows, with share buybacks taking place through the year. Annual reporting of major fertilizer companies showed strong free cash flow at the end of 2022, and this may be utilised over 2023 to fund merger and acquisition activity.

CF expands its presence in Louisiana with Waggaman

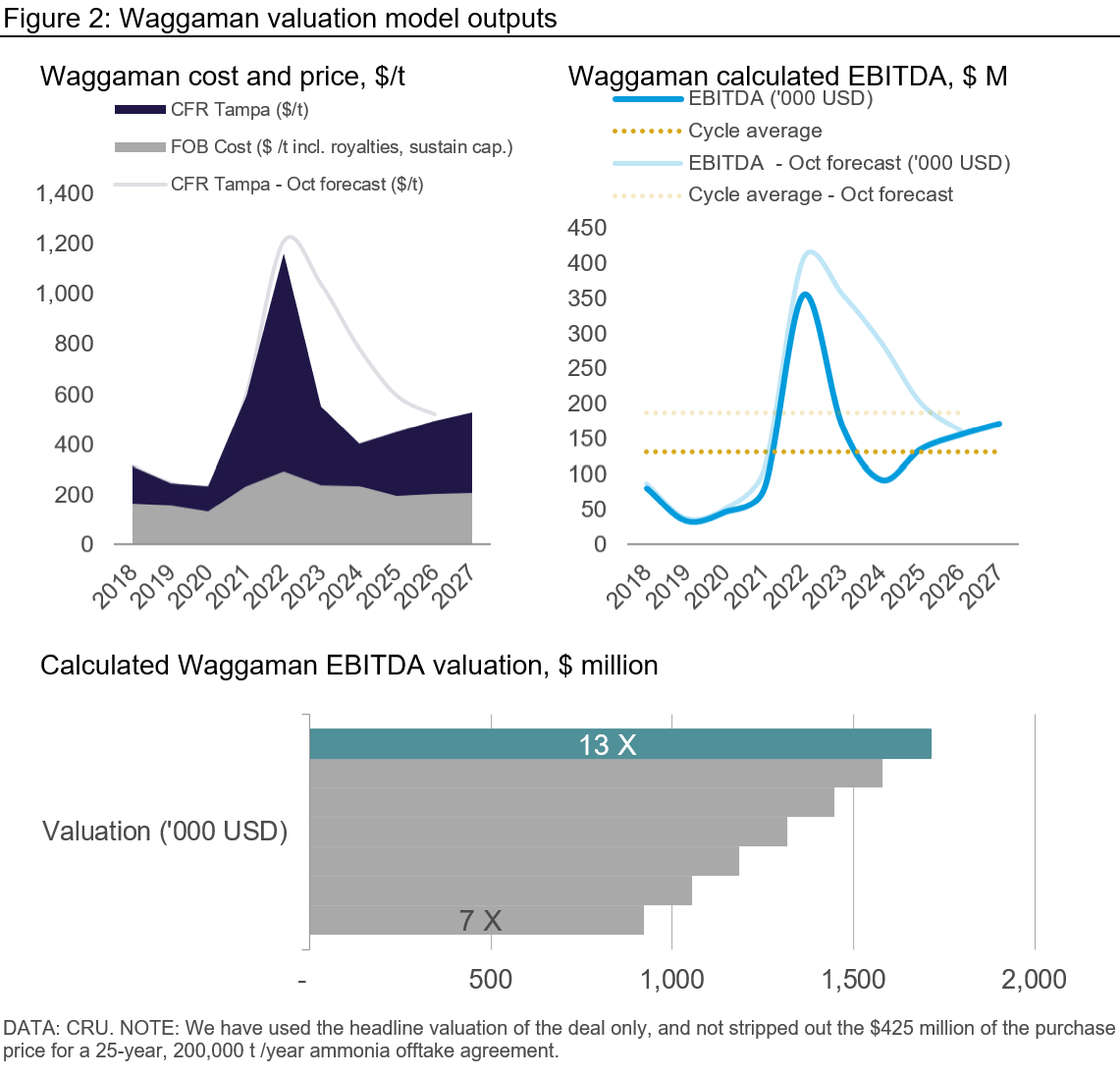

The headline M&A deal of 2023 so far has been CF Industries’ agreement to buy Incitec Pivot’s ammonia production facility and related assets at Waggaman, Louisiana, for $1.675 billion.

On the announcement of the Incitec Pivot review of the Waggaman plant in November 2022, we published an Insight, which suggested the valuation of the asset, and competition for it, could be high. Our (admittedly unsophisticated) EBITDA valuation model suggested a Waggaman deal could reach $1.5 billion and that CF was a likely buyer.

We have updated this model for our most recent ammonia price and cost forecasts, both of which have been revised lower on the faster-than-expected correction in gas and ammonia prices. Using these new inputs, the CF-Waggaman deal suggests a 13X multiple of cycle average EBITDA – well above industry standards.

More US nitrogen deals to follow?

The high valuation of the CF-Waggaman deal suggests more activity may follow. Indeed, stakeholder of the Gulf Coast Ammonia project, Lotus Infrastructure Partners (formerly Starwood Energy), is widely rumoured to be undergoing a process to sell its stake in the asset. The project, which is set to have a capacity of 1.26 Mt/year, is due to commission in 2023 Q3 and is forecast to have a lower cost base than Waggaman.

But the deals are unlikely to stop there. Competitive gas prices, generous subsidies through the inflation reduction act (see our analysis of blue ammonia costs here) and a variety of new potential end markets for ammonia mean that owning ammonia assets remains an attractive proposition (elaborated on further within this Insight).

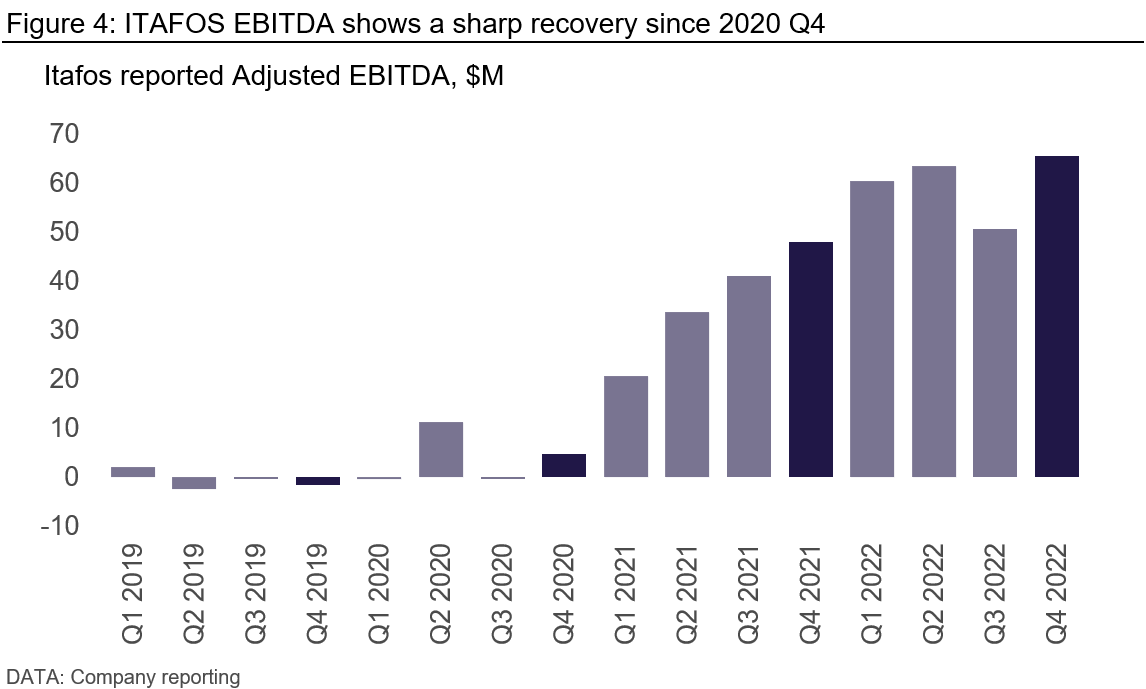

ITAFOS places itself under strategic review

A key point of difference between the US nitrogen and phosphate industries is the producer structure. US phosphate producers have consolidated over the past 20 years, with only four domestic producers remaining – Mosaic, Nutrien, Simplot and ITAFOS.

ITAFOS is the smallest of the four players, and recently said it was looking at “strategic alternatives”, including a possible sale of the company, to boost its value to shareholders.

ITAFOS owns two operating assets alongside a set of undeveloped projects. Its Conda phosphate rock mine and downstream production facility produces super phosphoric acid, MAP and NPS, most of which is typically sold west of the Mississippi River. It also produces sulphuric acid in Arraias, Brazil where a phosphate rock mine and downstream production facility remain undeveloped/idle.

The sale comes at a time in which ITAFOS has benefitted from higher phosphate prices and has started to yield sustainable earnings. The consolidated nature of the phosphate market within the US may restrict current players from bidding.

A risk is the pending approval of the proposed Husky 1 North Dry Ridge Phosphate Mine, which is required to maintain phosphate rock supply once its Rasmussen Valley mine reaches depletion around 2026. A final environmental impact statement on the new mine was completed in November last year, and a final decision is expected in 2023 Q2.

The ITAFOS strategic review acts somewhat as a litmus test for the phosphate industry. If the company attracts high and multiple bids, it will be indicative of a new-found confidence in a market that suffered a severe downturn and consolidation in 2019/2020. Alternatively, another private equity firm, similar to the current majority owners of ITAFOS, may take the company on.

The Nutrien and BHP question continues to linger

No analysis of fertilizer industry M&A would be complete without mentioning the ongoing speculation over a partnership or takeover between BHP and Nutrien. Indeed, analysts and industry watchers were not surprised to see this scenario raised again in March, when a senior BHP executive said the company would be ‘happy to partner’ when asked about Nutrien.

Despite potash prices rallying through 2022, we maintain our view, elaborated within this 2021 Insight, that Nutrien leadership and shareholders will be the key stakeholders in determining if such a deal eventuates. Nutrien recently restarted idled mines to capture higher prices over 2022. The challenges and success in this will serve as ample evidence in the company reevaluating its strategy. Should it reconsider this approach and look to work with a new, comparatively low-cost mine in BHP Jansen? Or should it double down on its current strategy?

The European dilemma

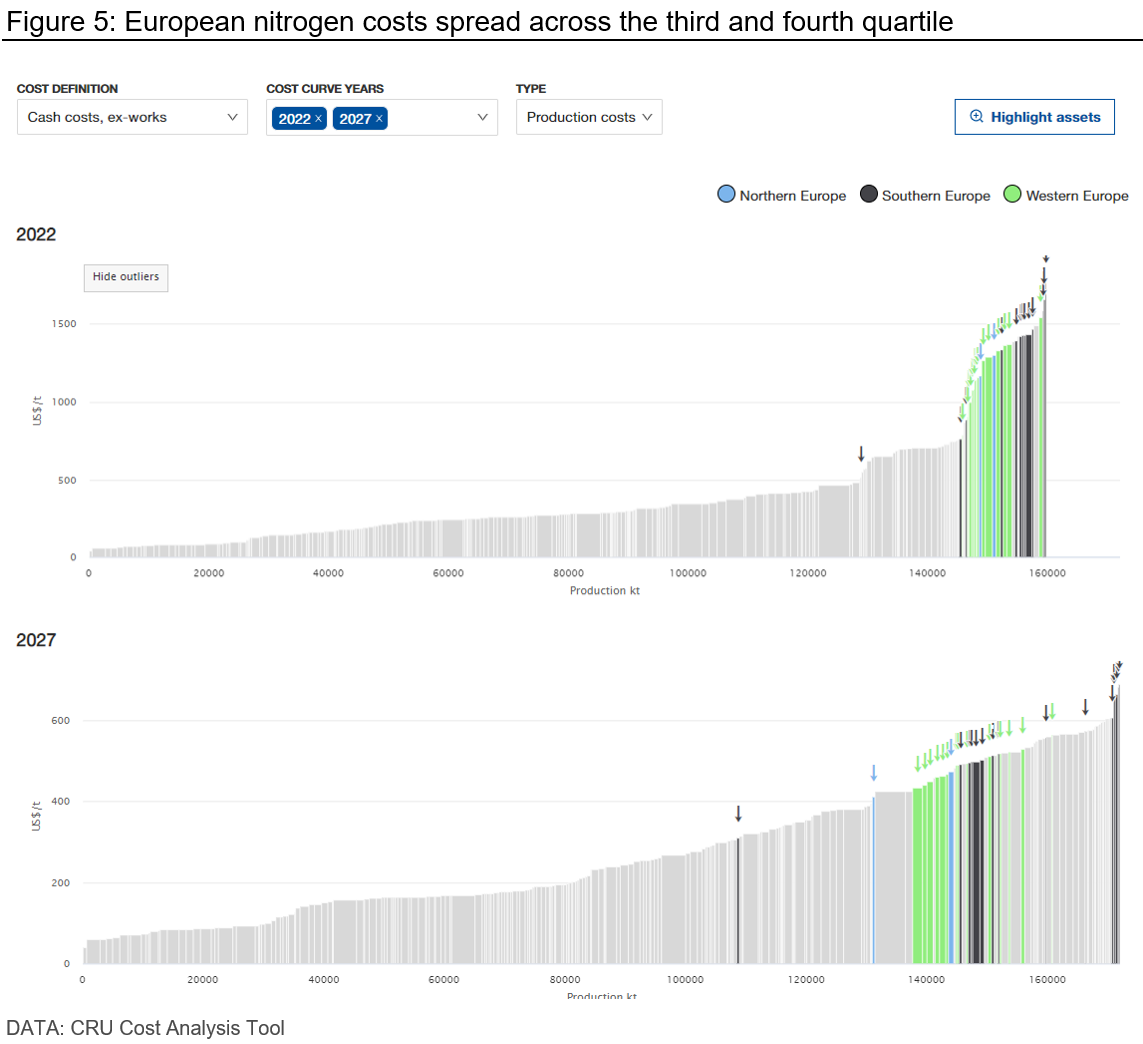

While the investment environment of nitrogen assets in the US is favourable, the same cannot be said for Europe. Uncertainty over high gas prices and fertilizer demand within the region create a less favourable long-term outlook.

Nevertheless, some deals are being executed. Agrofert recently received approval to buy the nitrogen arm of Borealis for $869 million. Turkish conglomerate Yildrim also recently won approval to acquire a majority stake in Croatian nitrogen producer Petrokemija for €55 million.

OCI was recently subject to calls by an activist investor to reconsider the structure of the company and its assets. This may signal even more potential activity in the nitrogen space and within Europe.

Will falling prices and higher interest rates curb activity?

Companies have so far looked to finance recent activity through improved cash balances, rather than debt. But as fertilizer prices come down, cash flows will follow, and the purse for M&A activity will likely shrink. With rising interest rates, companies may be reluctant to take the route of debt.

Financing risks aside, we expect to see a continuation of M&A activity in the fertilizer space, particularly in nitrogen and within North America. This is primarily due to the momentum supporting ammonia in new end markets and generous credits within the IRA. As highlighted in our Top 10 calls for 2023, we believe fertilizer companies will also look to roll the dice on agri-tech companies. This opportunity may be even more prevalent now given higher interest rates and reduced venture capital flow into new companies. Some promising agri-tech companies are likely to have more palatable valuations over the coming years, which established fertilizer producers may be more willing to pay for.

After a few quiet years, fertilizer M&A is back and there are plenty of opportunities to keep an eye on. CRU will help you to ‘watch this space’.

Explore this topic with CRU

Author Chris Lawson

Head of Fertilizers View profile