Implementing mandated policy cuts, particularly those aimed at achieving a flat crude steel y/y in 2023, is going to be challenging given the weak economic conditions. A strict implementation of policy will require at least 17Mt y/y cut in the last four months of 2023. The local government’s need to balance growth in 2023 will be a challenge and barrier to the cuts. These cuts, however, provide an upside risk to prices in case they are implemented in full.

Author Zhenzhen Jiang

Analyst View profile

Contributor Shankhadeep Mukherjee

Senior Analyst and Team Leader View profile

17 Mt steel supply cut too large to be strictly implemented over August-December period

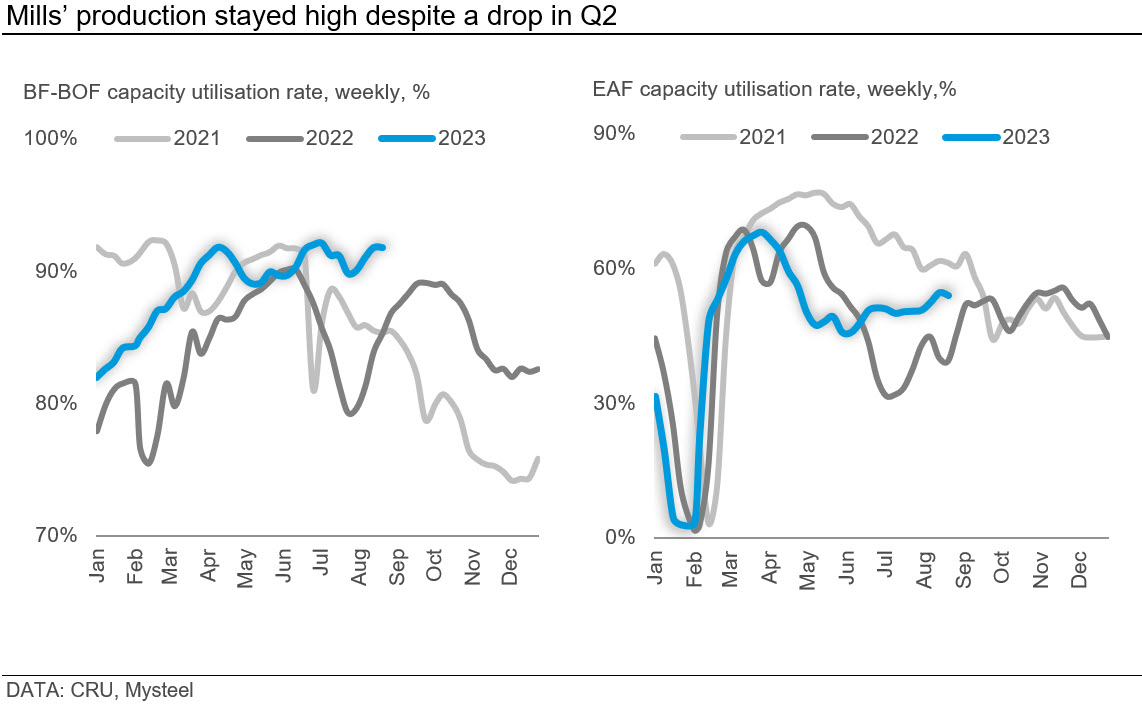

According to the National Bureau of Statistics (NBS), the total crude steel production in 2023 achieved 626 Mt in January-July. This is ~61% of the total crude output in 2022 as both BOFs and EAFs stayed at a high utilisation rate (see chart below). This suggests if the government mandated cuts were to be implemented in full, we would expect a cut of 17Mt y/y from this August to December period.

For this to happen, crude steel from August to December will be no more than 391Mt. The implied average monthly output in August to December will be 78 Mt, a 12% drop compared with 89 Mt of average monthly output in January to July.

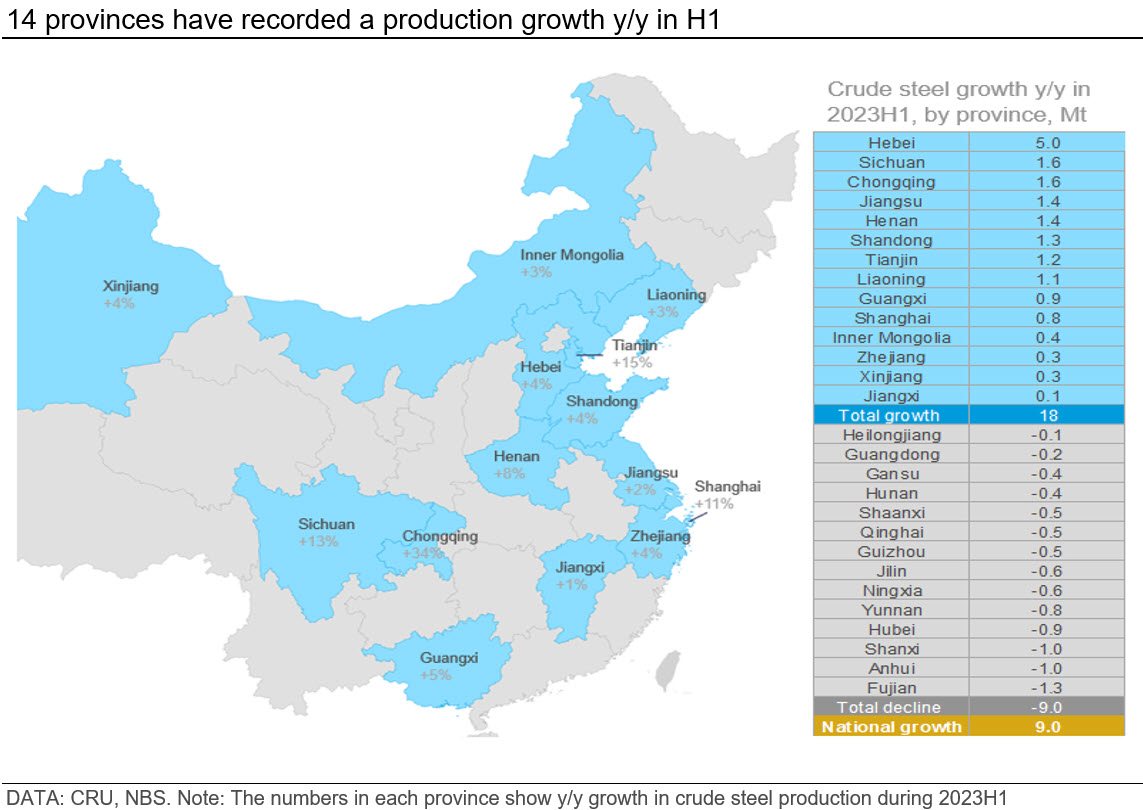

We believe this sharp decline in crude steel output will be too large to implement strictly. Meanwhile, the current YTD growth is concentrated in 14 of the 31 steel producing provinces. Hebei province, with steelmaking capacity of more than 250 Mt/y, is the largest steel producing province in China and has produced the most in 2023 H1 – see map below for full province by province details. Therefore, this makes the pressure of steel supply control differ among these provinces.

The need to balance the economy with decarbonisation in 2023 may be a barrier to cuts

Supply cut rumours increased following the drive towards decarbonisation

The mandated supply control starting from 2021 is regarded as part of decarbonisation efforts. We continue to believe that this will become a new normal for supporting the steel industry to reach the carbon peak before 2030.

Therefore, since August 2023, rumours about a policy-led cut for the rest of 2023 have increased. The rumours firstly started in Yunnan and Tianjin province and were quickly followed by rumours about Jiangsu, Shandong, and Shanxi provinces implementing similar production cuts.

Here we provide an analysis of the ease of implementation of production cuts in 2023 considering the weak economic conditions, the drive of the government to help reach the GDP growth target set for 2023 and the high YTD steel supply.

However, the government’s need for economic growth is a challenge to supply cuts in 2023

As China’s central government prioritises economic growth in 2023, provincial governments will rush to meet their respective GDP growth targets. This will introduce competing pressures on the provinces as they balance the need for growth with the need to decarbonise. We believe this is the reason that there has not been any public announcement about output control from the central government (i.e., unlike previous years) and this is a barrier to achieving a strict production control this year.

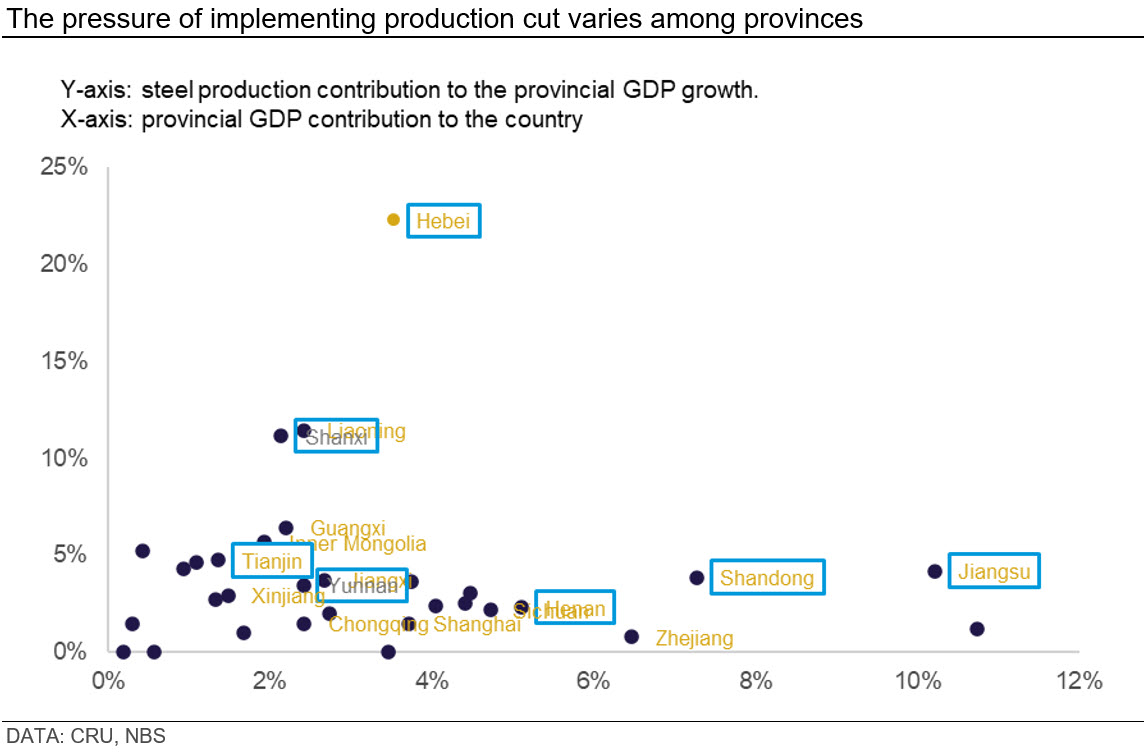

We looked at two factors to quantify the challenge – the importance of steel production to the provincial GDP and the share of provincial GDP to the overall country GDP. The chart below shows this with the factors plotted on the Y-axis and X-axis, respectively. On this, we have then superimposed provinces who have exceeded production in 2023 H1 (i.e. marked in yellow) and provinces with rumoured production cuts mandate (i.e. with blue frame).

We expect provinces in the bottom right corner will find it easier to cut supply given their lower reliance on steel as well as lower contribution to China’s overall GDP. These are mostly located in coastal regions, e.g., Jiangsu and Shandong provinces. In contrast, provinces in the upper left corner, including Hebei and Liaoning provinces, will be more difficult to cut their output as steel is more important to its GDP growth. Most of these are in inland regions as well.

Supply cuts are, however, an upside risk for steel margins and prices

Towards the end of 2020, the Ministry of Industry and Information Technology announced it would begin strict control, ensuring production in 2021 was lower than the levels seen in 2020. The total crude steel consequently achieved a 32 Mt y/y reduction in 2021. As explained in previous sections, we do not expect that the same feat can be achieved in 2023.

Instead, our base case incorporates the conventional production cut like the Winter Heating Season cut, event-led cut or cut-driven by air quality control. We expect a steel production cut of 2 Mt in 2023 H2 as mentioned in our latest Crude Steel Market Outlook. In addition, for production in 2023 Q4, we expect crude steel to be 10 Mt lower than 2023 Q3 and 2 Mt less y/y.

A national large-scale mandated supply cut is an upside risk for steel prices and downside risk for raw materials. Given the YTD production, if there is government action starting from September, it will require the average monthly crude steel production from the Sep-Dec period to have at least a 15 Mt decline compared with the crude output in July. This, together with the traditional demand peak season (Sep-mid-Nov), will quickly drive-up steel mills’ margins and this can provide an upside risk to prices.

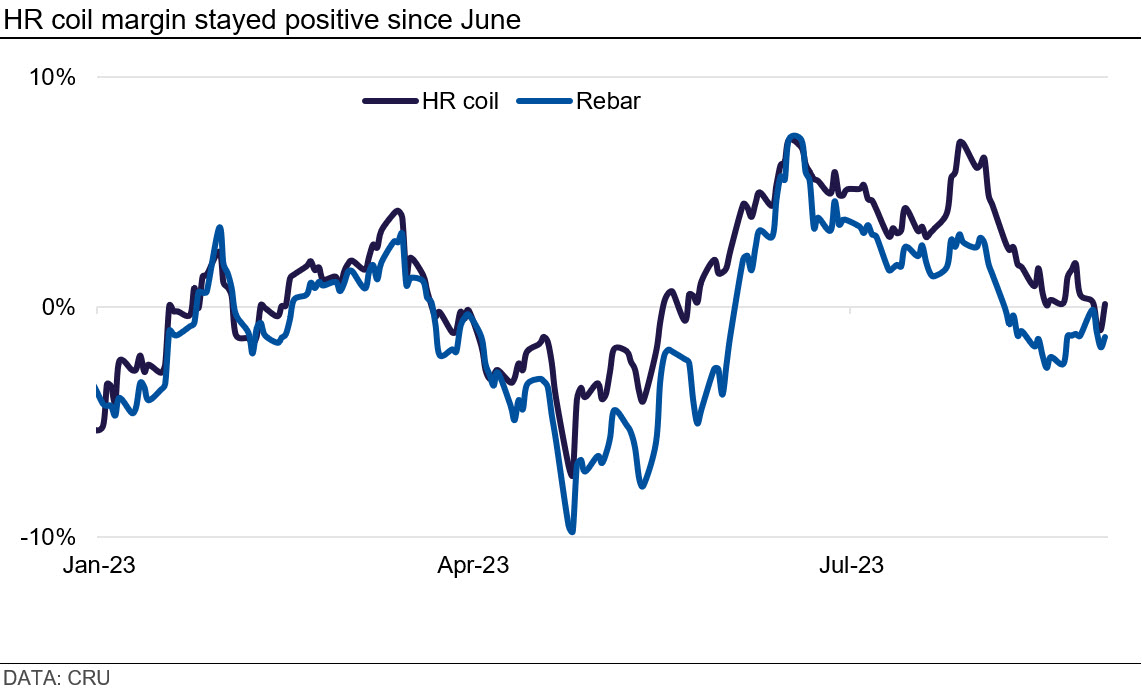

As assessed in our model, despite the margin of HR coil and rebar having dropped from the high point reached in late July, it recovered after entering September. The market-led production cut may be hard to occur significantly in the short-term considering the seasonal demand improvement. This could result in the government struggling to implement strict production cuts.

As there are still uncertainties around government actions, CRU will continue to track the progress of the national mandated cut closely and update accordingly.

Explore this topic with CRU

Author Zhenzhen Jiang

Analyst View profile

Contributor Shankhadeep Mukherjee

Senior Analyst and Team Leader View profile