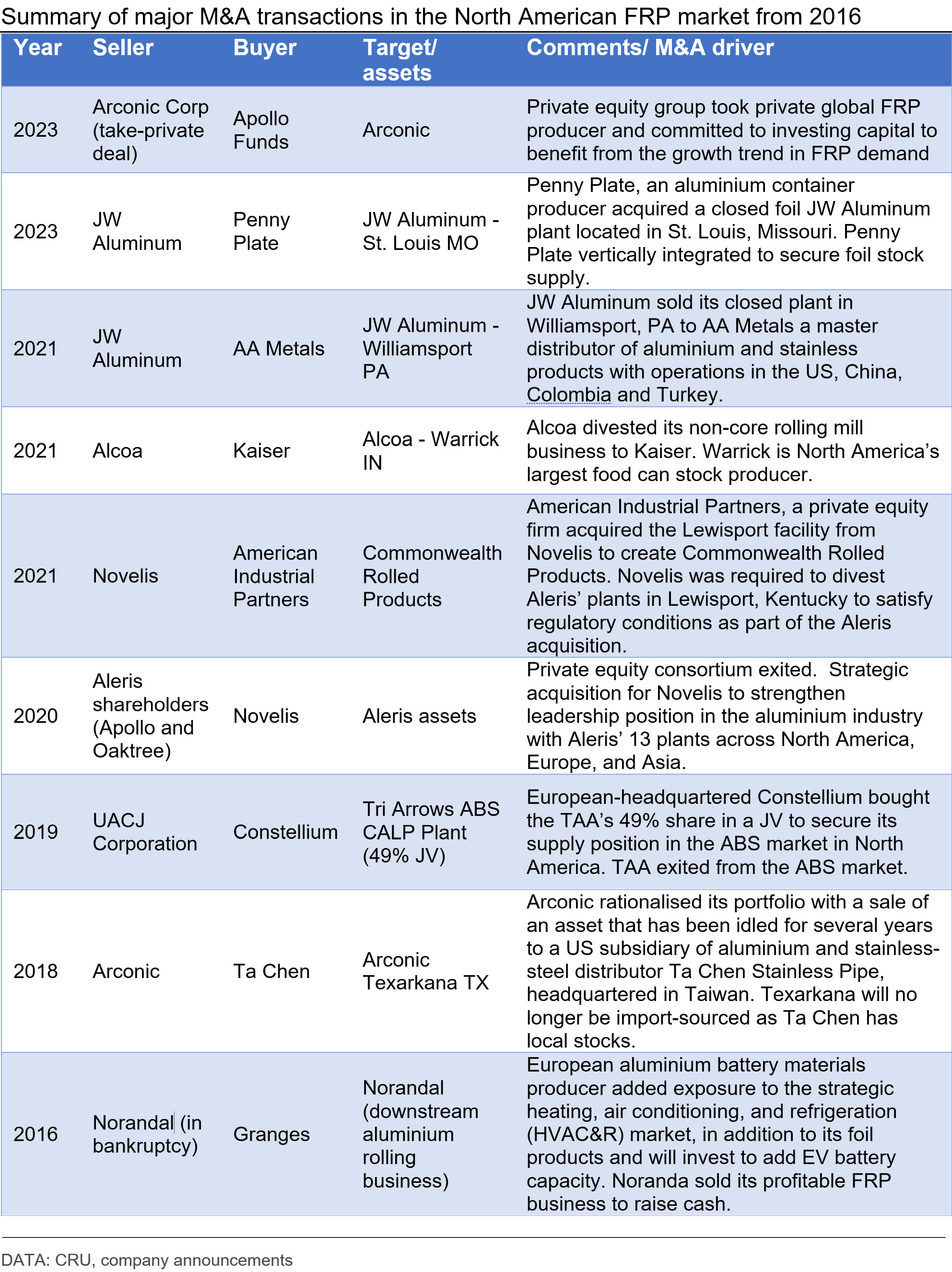

We continue our analysis of the completed M&A deals in the flat-rolled markets. In this Insight, we expand on our previous analysis on the European market to apply the same methodology to North America. The context and main conclusions are similar for both regions. Despite falling rolled products consumption in 2023 and weak conversion fees, M&A activity is high in North America. However, the nature of this is different. In the case of North America, one sizable deal was closed in 2023. The acquisition of Arconic by Apollo Funds is significant for the North American market. In 2022 Arconic had an estimated 17% share of total FRP production, while 66% of the global Arconic sales were in the United States. We extended our historical M&A deals analysis past 2023 to collect more data.

Author Alexey Pavlov

Senior Analyst, Aluminium View profile

Author Matthew Abrams

Research Analyst View profile

Contributor Steve Williamson

Research Manager, Aluminum View profile

Despite the currently challenging market conditions, M&A activity is high in the North American semis market

In the Insight titled “Aluminium rolled products: What we can learn from M&A activity in Europe” we analysed remarkably high M&A activity in the European flat-rolled market in 2023. This is despite currently challenging conditions. For this analysis, we focus on M&A in the North American flat-rolled market.

Regarding underlying FRP consumption trends, there are similarities between European and North American markets. To start with, both markets are going through challenging times in 2023. CRU now forecasts a significant decline in 2023 FRP consumption in North America, while transport is the only sector to grow y/y in 2023 (see more here). However, the United Auto Workers (UAW) strike might stall auto body sheet (ABS) growth in 2023.

As for conversion fees, we believe North American fees are holding up better than in Europe but are still on a downtrend from their peak in January 2023. For instance, 3003 alloy is down 10% from January 2023 to October 2023; while 5052 declined by 8% for the same period (see more details here). The decline in fees in the US is moderate in comparison to Europe. European common alloy fees are down around 20% from January 2023– October 2023.

We investigated historical M&A deals past 2023 to collect more data and summarise completed transactions from 2016 in the table below.

Recent M&A activity in North America did not lead to market consolidation

What can we learn from historical M&A activity in North America? Overall, strategic M&A in a time of turmoil reflects the longer-term positive view of the market. Firstly, European producers expanded in the North American market. In 2016 Granges, a European aluminium battery materials producer, expanded in the strategic heating, air conditioning, and refrigeration (HVAC&R) market with the acquisition of the profitable Noranda FRP business. Granges added HVAC&R to its foil products and is expected to invest into the addition of EV battery foil capacity to the US mix. Then in 2019, European Constellium bought the TAA’s 49% share in a joint venture to secure its supply position in the ABS market in North America.

Secondly, we observe major players rationalising their portfolios with the sale of the non-core or idled facilities. For example, in 2018 Arconic sold the Texarkana TX plant that has been idled for several years to a US subsidiary of aluminium and stainless-steel distributor Ta Chen Stainless Pipe, headquartered in Taiwan. Then Alcoa divested the non-core rolling mill business at Warrick to Kaiser.

Moreover, JW Aluminum sold a closed plant in Williamsport as well as a foil producer in St. Louis, Missouri to AA Metals – a master distributor of aluminium and stainless products; and Penny Plate – an aluminium container producer. It should also be noted that all the idled facilities were restarted by the new owners. For instance, Penny Plate became vertically integrated and secured foil stock supply, while Ta Chen managed to leverage the domestic Texarkana TX supply position and no longer be import-sourced. Foreign investments in US rolling assets are allowed to get benefits from IRA/BBB/Chips Act and Science/USMCA.

Thirdly, private equity companies play an important role in the market. This can be confirmed not only with the already mentioned Arconic–Apollo deal but also in 2020 Apollo and Oaktree sold their stakes in Aleris to Novelis, while in 2021 American Industrial Partners acquired the Lewisport facility from Novelis to recreate Commonwealth Rolled Products.

Finally, we observe that since Novelis made a strategic acquisition of Aleris’ 13 plants across North America, Europe and Asia in 2020, and Kaiser bought the Warrick facility from Alcoa in 2021, most recent M&A transactions did not lead to North American FRP market consolidation but were influenced by US antitrust market concentration considerations.

Is consolidation viable in the North American FRP market?

As we discussed above, the most recent M&A activity in the North American FRP market has not led to market consolidation. However, in terms of other types of corporate activity and after 40 years in the making, there are two new greenfield recycle-remelt-rolling projects, which are underway in the North American market. As such, Novelis began construction of its $2.5 bn recycling and rolling plant in Bay Minette, Ala; while Steel Dynamics announced the construction of the $1.9 bn aluminium flat rolled mill in Southeastern US. Hence, considering the strategic interest and investments in the FRP sector, the still valid question is whether North American consolidation is theoretically feasible. This is a complicated subject with strategic, financial and operational considerations to name a few. In the case of the US market, it is also subject to antitrust market concentration considerations. However, firstly we need to understand if the structure of the FRP market in North America allows for consolidation.

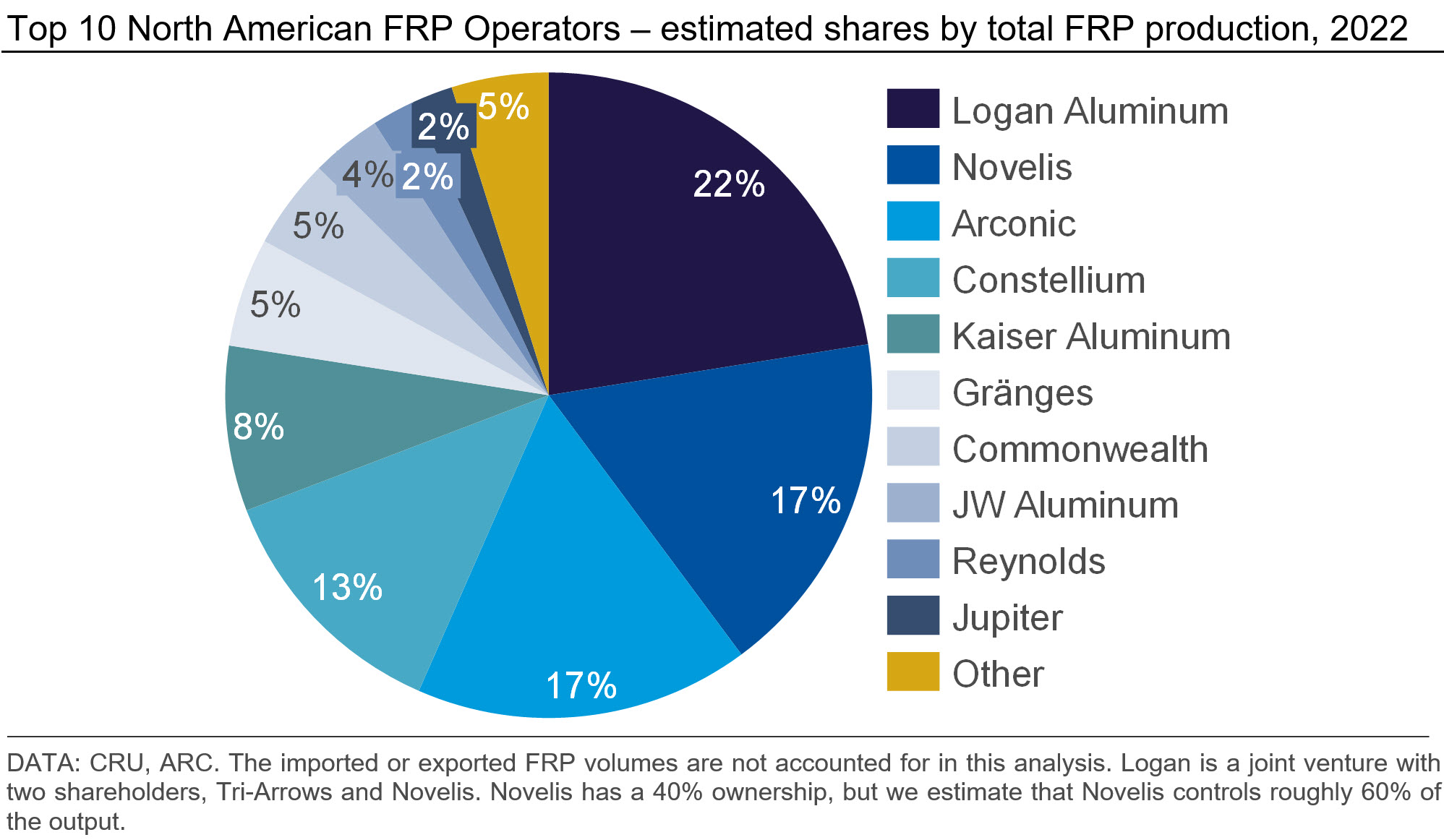

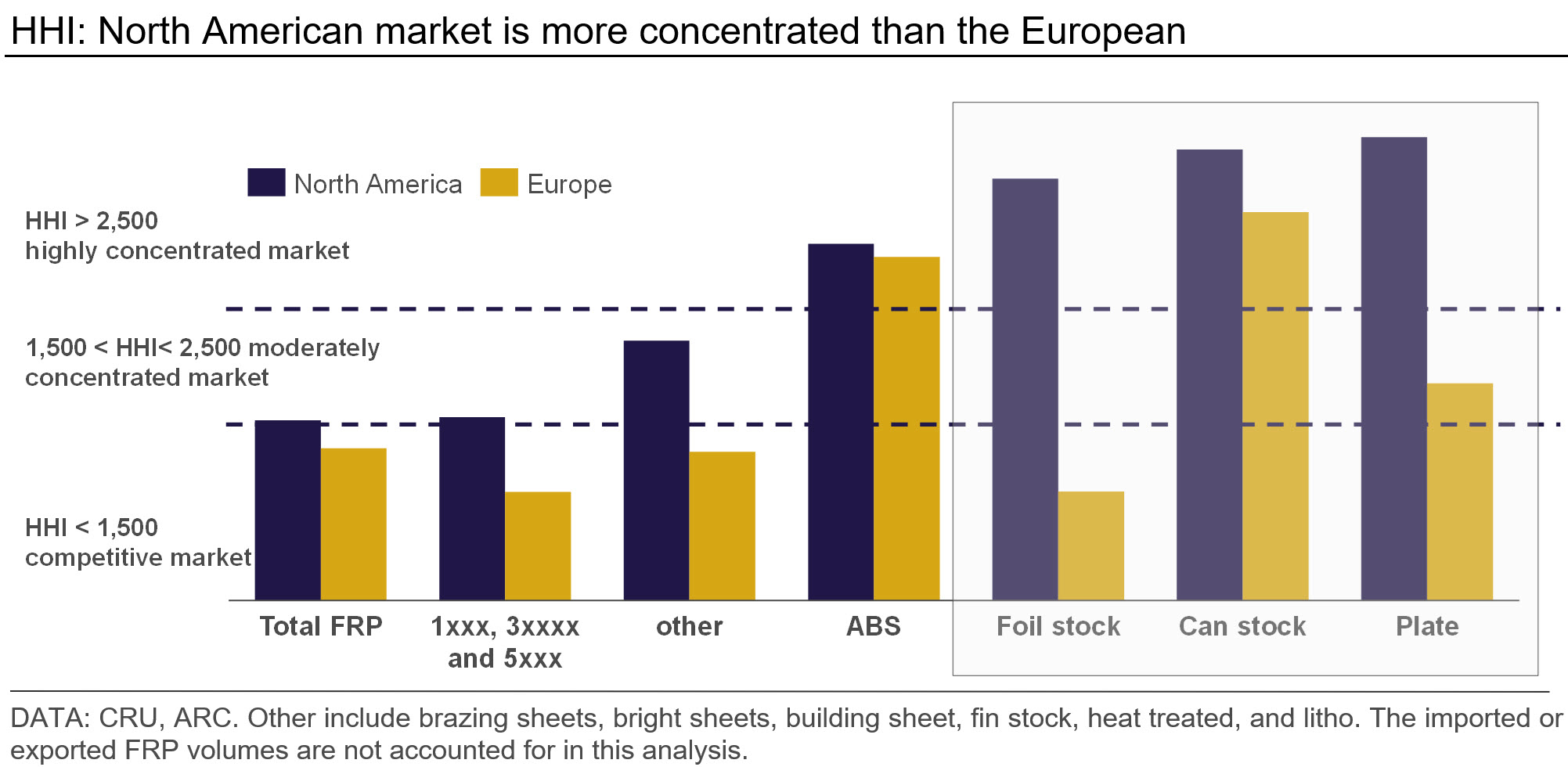

To answer this question, we analysed detailed production data by product type from the CRU Aluminium Cost Model (ARC), which covers 18 operators and 35 mills based in North America. The imported or exported FRP volumes are not accounted for in this analysis. The by-mill data was combined by the operator to come up with the consolidated production profile. We have also calculated the Herfindahl-Hirschman Index (HHI), which is used to determine market competitiveness pre- and post-M&A, and applied it to measure market concentration for combined FRP market as well as by-products. Furthermore, as we adopt a consistent data set from ARC and the same methodology – which was applied to the European market – both markets can be compared to draw cross-border conclusions.

The high-level results are presented below. We estimate that the top ten FRP operators in North America produce 95% of the total FRP market volume (the share is 82% for Europe), while the top three operators control 55% of production, which is similar to the European level. Additionally, among the top 10, there are six operators with shares between 2–8%. Hence, in such a market, a top 4 producer with a 13% share can theoretically improve their position from fourth to third via the acquisition of any of the top 5–7 producers. In this case, its production share will improve roughly to 17% or 18%. Additionally, a consolidation of three operators with production shares between 5–8% can potentially create a top 4 player with a 17% market share, assuming a combination of 8%, 5%, and 5% shares.

However, as was the case for the European market, a more detailed segment analysis is required as FRP operators run complex diversified operations producing unique products, as a single operator can produce all products and have various production shares.

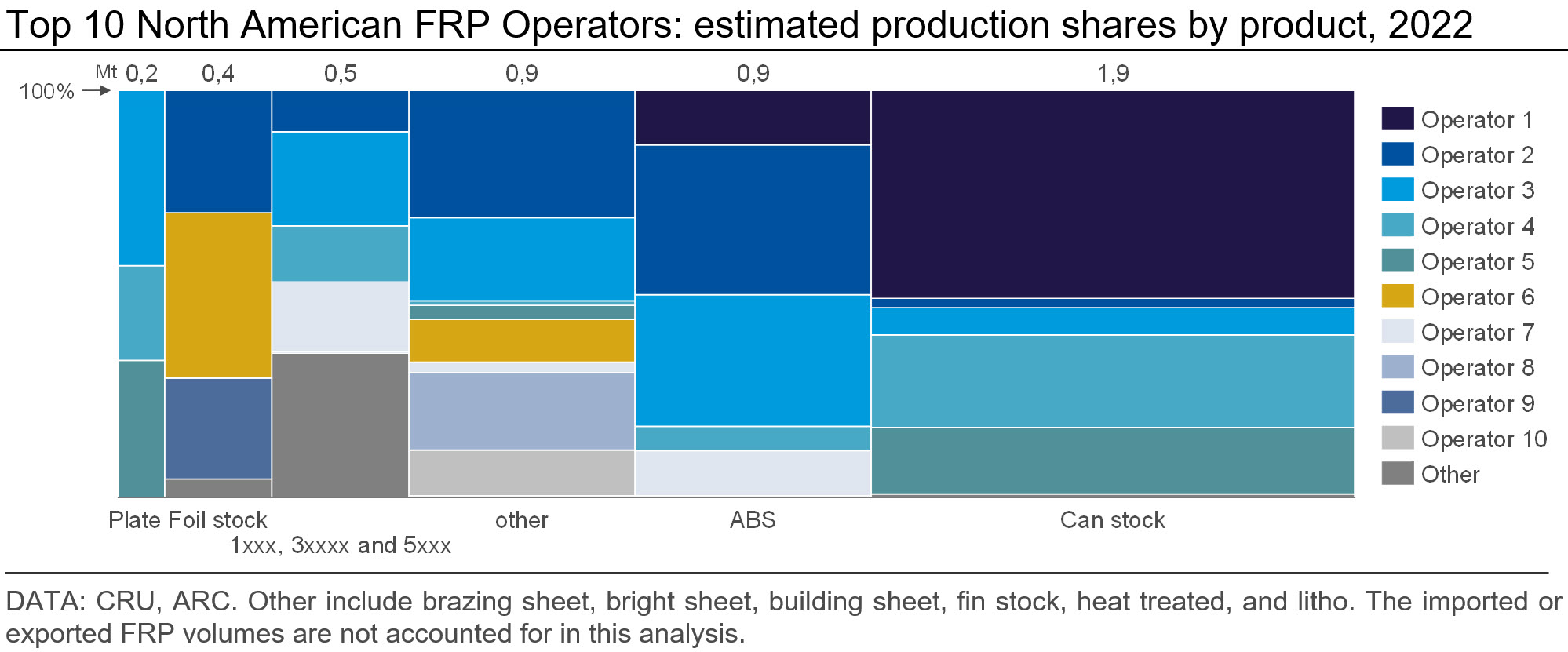

For the North American market, our Aluminium Rolling Costs service also covers 18 different flat rolled product types, which we combined into six key product groups – 1xxx, 3xxx, and 5xxx ‘common’ alloys, foil stock, plate, Auto Body Sheet (ABS), can stock, and others. For each group, we calculated an operator market share by production as well as the HHI. Those results can be also compared with the European output.

As can be seen from the chart below, the combined North American FRP market can be considered competitive as HHI is below 1,500. The same conclusion can be made for 1xxx, 3xxx, and 5xxx markets. However, can stock, ABS, foil stock and plate market segments are highly concentrated, while the other category is moderately concentrated as it sits in the middle, with HHI between 1,500–2,500.

Therefore, we can conclude that the combined market in both Europe and North America can be considered competitive. But on a product-by-product level, there is a notable difference – with the European market being less concentrated in foil stock, plate, and the other category. This raises the prospect of a cross-border consolidation and trade flows.

Therefore, a potential merger of two operators, both producing can stock, plate, foil stock and/ or ABS might not be viable as those markets are already highly concentrated, and a combination might raise antitrust concerns. This might be one reason for the North American producer’s recent investments in green field production. However, we can still come up with potential combinations on the operator level. For this, we need to study operators’ market shares by product in detail. The results are presented below for North America.

We believe that M&A combinations on an operator level are still feasible, based on the segment market structure. However, options are more limited for the North American market, compared with Europe. For example, a top FRP producer exposed to a highly concentrated can stock, plate, foil stock and/or ABS markets can theoretically increase its total FRP market share via an acquisition of a 1xxx, 3xxx, and 5xxx producer from the other category. However, we believe there are more options for reverse acquisitions as an FRP producer (with a strong market share in 1xxx, 3xxx, and 5xxx and/ or other category) can potentially increase its total market share and enter a new segment via the acquisition of a plate or ABS operator.

Explore this topic with CRU

Author Alexey Pavlov

Senior Analyst, Aluminium View profile

Author Matthew Abrams

Research Analyst View profile

Contributor Steve Williamson

Research Manager, Aluminum View profile