Steel sheet price volatility has peaked in the USA after record average w/w price changes during 2022. In our view, prices will trade in a much narrower band over at least the next five years (barring any further black swan events) – especially given some key structural changes within the domestic market itself. Indeed, volatility is likely to evolve back towards levels seen prior to the pandemic over the coming years. We expect steel sheet prices to eventually come back in line with their more historical relationship to underlying costs.

Author Ryan McKinley

Senior Analyst View profile

Markets have now stabilised following immense volatility

Stability has now by and large returned to the market after mills enforced price hikes in early December 2022. While prices will likely rise a bit more in early 2023, there are structural reasons that make a repeat of 2022 (or frankly 2021) highly unlikely. Firstly, new sheet capacity in the US will keep domestic supply better matched to demand. In total, net growth in North American sheet capacity should be around 10.5 Mt between 2021 and 2024. This means that even if availability from abroad becomes constricted, there will be enough new supply on the continent to make up for import shortfalls – even in the face of rising demand.

The threat of raw material disruptions will also be lower moving forward. The successful readjustment of pig iron supply chains away from Ukraine and Russia, alongside some pig iron production domestically, mean that impact of another disruption will not be as severe as in 2022. Indeed, it is likely that greenfield or brownfield expansions for DRI/HBI operations will continue to occur in the near future, making risks to metallics access much lower from a geopolitical perspective.

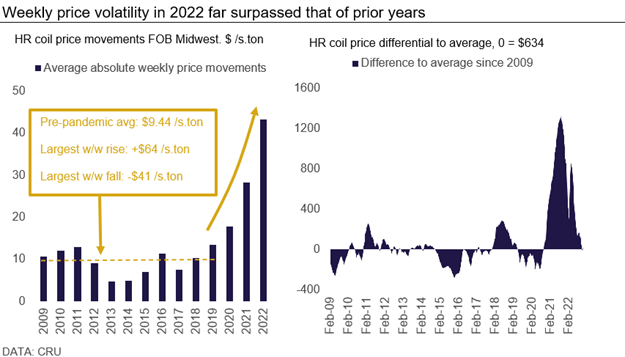

How did last year’s volatility compare to other years?

The year 2022 was the most volatile we have ever recorded in terms of weekly steel sheet price movements. This is because a specific set of circumstances, especially geopolitical ones, worked together to disrupt supply chains globally and within North America itself – albeit to a lesser extent for the latter. While it is difficult, if not impossible, to forecast another black swan event like the war in Ukraine, developments within the North American market itself also mean that such price shock is unlikely to occur again. As such, the extreme volatility last year will likely not be repeated any time soon.

Last year’s intense price movements were partially the result of a comedown from record levels set in 2021. For a quick comparison, the average absolute price movement per week in 2022 was about $43 /s.ton – double the averages for 2021 and 2020 which were both volatile years in their own right. From the record-breaking price level of $1,958 s/.ton set in the last week of September 2021, prices had crashed by over $1,000 /s.ton by the first week of March 2022. This was a steeper and faster price decline than during the Great Financial Crises between 2008-2009, when prices took ten months to fall by $702 /s.ton.

This price collapse was halted by Russia’s invasion of Ukraine. Combined, both countries accounted for 60–70% of total annual pig iron exports globally. With sanctions and self-imposed embargoes hitting the former, and combat preventing exports from the latter, pig iron supply was substantially disrupted and mills around the world were forced to search for new sources. In particular, US EAF sheet mills needed to locate new sellers as the country was nearly 100% reliant on imported pig iron to keep furnaces running. With mills making large offers to foreign pig iron providers, sheet prices underwent an unprecedented w/w price spike of $182 /s.ton from the second to the third week of March.

Extreme sheet price volatility has peaked

Overall, our near and medium-term outlook is that price movements will be much more stable compared to the prior three years. From peak to trough, 2022 prices moved by $875 /s.ton compared to ~$950 /s.ton in 2021 and ~$400 /s.ton in 2020. Barring another black swan event, we project that steel prices will be much less volatile in 2023, with a total peak to trough move of around $85 /s.ton. Indeed, extreme sheet price volatility has peaked in 2022 and while prices may not be flat, they will be much less volatile due to structural changes in both steel sheet production capabilities and within raw material acquisition practices.

Explore this topic with CRU

Author Ryan McKinley

Senior Analyst View profile