Author Minxin Chen

Senior Consultant View profile

Contributor Alex Tonks

Head of CRU Australia and New Zealand View profile

Contributor Richard Lu

Senior Analyst View profile

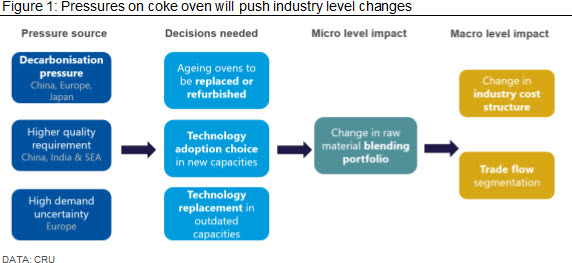

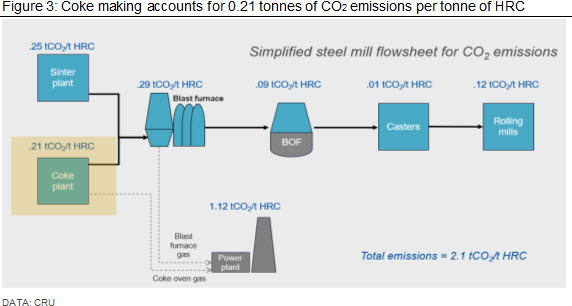

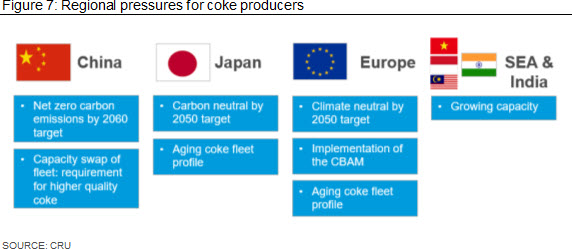

However, carbon neutrality targets have taken the discussion further to include decarbonisation, as coke making accounts for ~10% of steelmaking emissions. In China, while a capacity swap continues to impact technology adoption of coke ovens, more actions must be taken to meet the announced carbon neutral target by 2060. In mature markets (Japan & Europe), aging coke ovens means replacements or refurbishment will be required – where decisions will depend on available technology, capital, and emission related policy restrictions. Specifically in Europe, the upcoming carbon border adjustment mechanism (CBAM) will add more uncertainty in the decision making. South East Asia (SEA) and India have less pressures due to relatively young capacity fleet and less intensive carbon restrictions, but the technology profile is also key for growing capacity that will be constructed over the next decade.

Clients needing a comprehensive understanding of the decarbonisation impacts upon the coke oven industry have turned to CRU's team of experts. For more information on CRU’s capacities in the coking industry and technology solutions for decarbonisation, please get in touch.

Reducing cost, maintaining coke strength, and now decarbonisation are all major drivers of coke oven technology developments

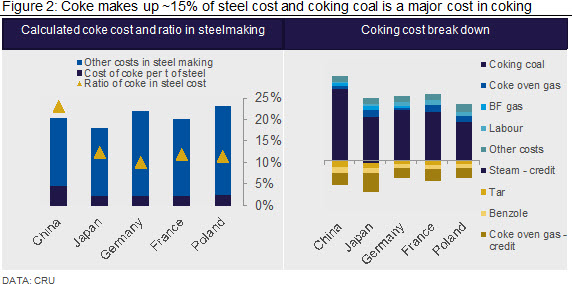

Coke costs represent ~15% of total steelmaking costs. However, as the costs of production vary significantly, some steelmakers report coke costs to be over 40%. As a result, the availability, quality, and price of coal have become key factors for reducing steel costs of production. Traditionally, a higher ratio of hard coking coal results in increased coke strength but also brings with it a higher cost (blended coal cost represents ~80% of total coke making costs), and there is usually a trade-off between higher coke strength and lower cost. As such, any technology to help increase the ratio of low-quality cheap coal while maintaining coke strength can significantly lower cost for operations.

Due to its high carbon intensity, steel and coke making has been one of the key industries in the decarbonisation discussion. Unlike the aluminium industry where green products can be produced via cleaner energy source such as hydro power, there is not yet an economic and green path to produce high quality steel products: hydrogen technology is high cost (see hydrogen-steelmaking for more information), and EAF cannot completely replace BOF steel especially for high quality products such as flat steel products. As such, steelmakers are looking for means to decarbonising the BF/BOF route. Within the BF/BOF steelmaking route, coke plants have abatement potential.

Chinese coke ovens will need to accelerate technological change to meet carbon targets

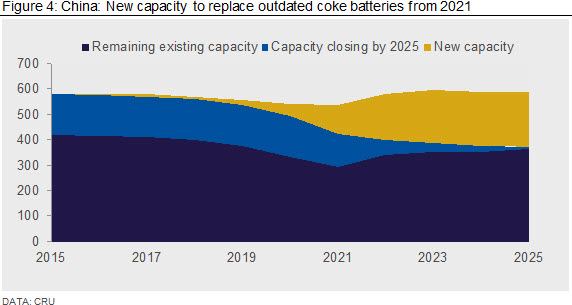

In China, coking capacity has been progressively reduced since 2016 as the government implemented a capacity swap initiative aimed at replacing outdated and pollution-intensive coke batteries (please refer to this insight for more information). However, CRU forecasts that a large amount of new capacity will be added into the market from 2021, to replace outdated capacity, and the technology adoptions within these new ovens are critical as they will need to match China’s steel making trend of higher quality as well as lower emissions.

Coke dry quenching (CDQ) technology is energy-efficient and produces lower emissions, while also allowing for electricity generation using waste heat recovery. As part of the Chinese government plan, CDQ technology has been promoted as a target in all three five-year plans since 2002 and it is required by law for new ovens. However, the uptake of CDQ has been slow given high capital costs. As the Chinese central government announced its ambitions for net-zero carbon emissions by 2060, there are increasing expectations for government action to accelerate CDQ uptake. The Chinese government is also drafting “The Carbon Reduction Action Plan for Iron and Steel Industry”, which we believe will likely heavily impact the coke industry.

The announcement of the 2060 carbon neutral target has also brought heat recovery ovens back to sight. Heat-recovery coke ovens recover the by-products generated during the coking process and have lower emissions, while non-recovery ovens collect the by-products and emits the waste gas and have higher emissions. The Chinese market is dominated by high emission non-recovery ovens, which account for over 95% of coking ovens as it brings more monetary benefit by selling the by-products. The abatement potential would be huge if a substantial share of new ovens adopted heat recovery.

Overall, the shift in switching the technological profiles must accelerate sharply to meet the carbon emissions targets, as well as quality requirements.

Japanese and European ovens are ageing, but the solutions are different for the two regions

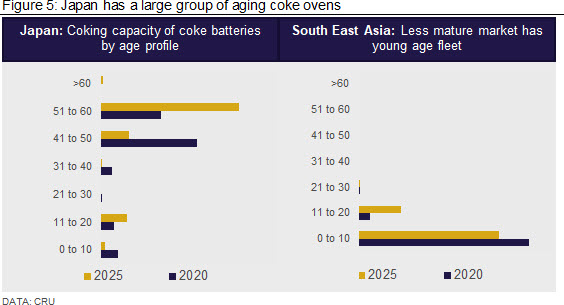

Japan hosts the largest share of old coke ovens globally. Many of the Japanese coke ovens were constructed during the rapid economic growth period between 1964 and 1973. CRU estimates that ratio of aged coke ovens (greater than 40 years old) in Japan will reach ~85% by 2025.

However, Japan is also leading in the adoption of coke oven technologies such as CDQ, Dry-cleaned and Agglomerated Pre-compaction System (DAPS) and Scope 21. These technological advancements have provided Japan with options when replacement of existing capacity is needed. As Japan relies completely on seaborne coking coal imports, shifting technology will have an impact on the product segmentation of seaborne coals.

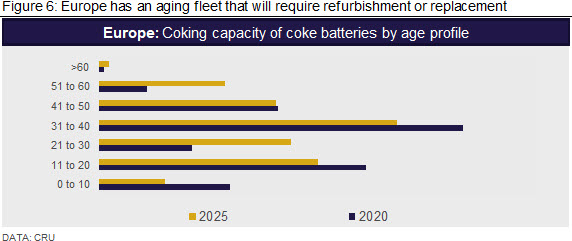

Does Europe rebuild or refurbish its aging fleet of coke ovens?

The aging fleet in Europe requires either refurbishment or replacement in the very near future. Yet, the increasing EAF share in steelmaking, unpredictability in the commercialisation timeframe for hydrogen-based technology and higher carbon prices in Europe is driving high uncertainty in coke demand. The difficulties in obtaining financing will only get worse for technologies that are not “greening”.

A complete shift to EAF steelmaking is unlikely given the need for high quality automotive steels in Europe (EU). Relying on imports will be a costly option as well - the upcoming Carbon Border Adjustment Mechanism (EU CBAM) imposes a tariff on high emission imports into the EU, which will make it harder for European automakers to import BOF steels.

A commercial-scale breakthrough before 2050 for new steelmaking such as hydrogen-steelmaking is also risky – due to high capital and operating costs, there are still many hurdles and levers for hydrogen-technology before it can become a feasible option for widespread adoption.

Hence the BF-BOF route will remain essential for European steelmakers and as part of decarbonisation of this processing route, coke oven technology is critical.

What decisions are you facing in a low carbon economy?

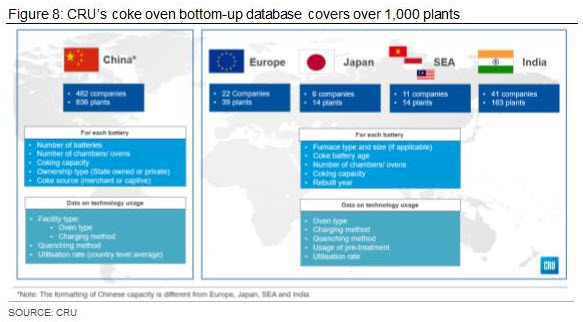

With the world looking towards net zero carbon emission targets, technology choices that enable decarbonisation and meet demand side requirements in the steelmaking process are becoming increasingly paramount. Our bottom-up database is focused on regions where understanding of coke oven technology is critical, either from cost control perspective or decarbonisation perspective. Chinese ovens are in urgent need to accelerate the technology shift under the carbon neutral target and we expect the government to publish “The Carbon Reduction Action Plan for Iron and Steel Industry” in the near future, which will likely impact the Chinese coke industry in the next decade; Technology adoptions in the new capacities in China and in the replacement ovens in Japan will have an impact on seaborne coal trade flows; Europe will face harder decisions following the implementation of CBAM; While, SEA & India are the key growth areas for coking capacity, decisions on technology will impact their competitiveness for several decades.

We understand that the steel industry and other commodity producers may be facing a series of tough questions over the next few months regarding the management of their assets and portfolios. CRU Consulting stands ready to support your business in taking complex decisions amid highly uncertain financial, industry and policy-related conditions. CRU’s bottom-up coke oven database covers over 1000 plants covering China, Europe, Japan, SEA and India.

CRU Consulting’s analysis and wider decision support tools are at the cutting edge of management support to the mining, metals and fertiliser industries. They are built on our rich market knowledge, client-centric approach, as well as technical experience and data capabilities. Put simply, we can help you with the decisions you need to make, so please do get in touch – either to discuss any of these issues, or to better understand the key opportunities and risks affecting your business.

Explore this topic with CRU

Author Minxin Chen

Senior Consultant View profile

Contributor Alex Tonks

Head of CRU Australia and New Zealand View profile

Contributor Richard Lu

Senior Analyst View profile