CRU hosted its first virtual Jakarta Seminar on 8 June 2021. This provided commodity market participants an opportunity to discuss key issues concerning Indonesia’s metals and mining industry within the context of global supply chains, decarbonisation and a rapidly changing geopolitical landscape.

The event comprised of presentations from CRU consultants, a panel discussion with industry experts, followed by a live Q&A with the attendees. The main themes that were discussed during the event are as follows:

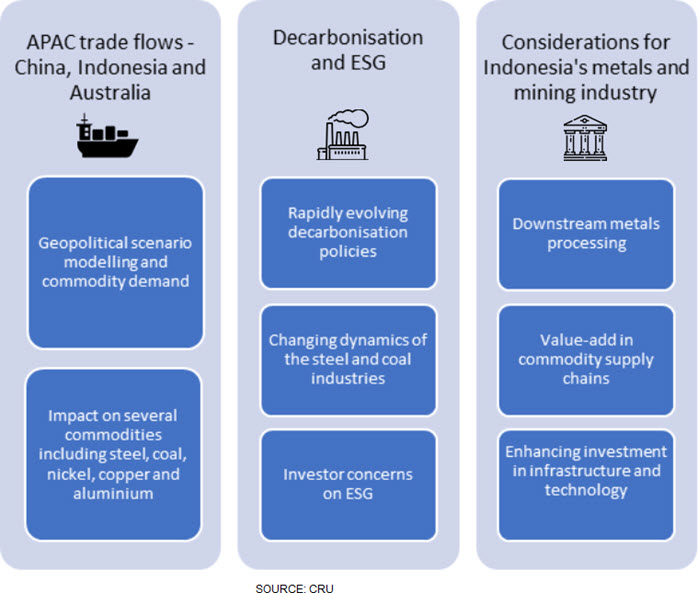

The seminar showcased presentations that explored the bilateral dependencies between Indonesia, China, and Australia. With China becoming Indonesia’s largest export destination, it is critical to understand the possible developments in trade relations between these countries in the future. One of the key takeaways was that, while China is aiming to increase its reliance on domestic resources, it still needs to secure supply of key commodities such as nickel, copper and iron ore from Indonesia and Australia. Recent developments between Australia and China’s trade relations were also addressed. These included restrictions on imports for certain products like coal, seafoods and agricultural produce from Australia. However, it is having a considerable impact on international commodity trade flows and prices. For instance, on the back of these restrictions, China’s domestic coal prices have increased significantly compared to the international prices.

Analysis from CRU’s geopolitical scenario modelling showed favorable outcomes for Southeast Asia in terms of continued future FDI, including that from China. However, even in the most economically cooperative future scenarios, stagnating commodity demand could increase vulnerability to political outcomes and trade flow shocks.

The other presentations provided key linkages between the global push for decarbonization and its impact on the steel market. While Southeast Asia and India are expected to exhibit strong steel demand in the medium term, steel demand in other regions will stabilize. CRU’s analysis showed a need for drastic emissions reductions to meet the global warming target of 1.5 ºC set by the Paris Agreement.

The seminar concluded with presentations and an expert panel which provided a broad overview of Indonesia’s downstream operations and some domestic policy issues within the mining industry. CRU’s experts highlighted that there was a growing potential for increasing downstream processing in Indonesia, especially for nickel, aluminium and copper. This was underpinned by Indonesia’s competitive edge as one of the lower cost producers. Analysis of value-added products in supply chains also revealed that nickel and alumina exports had high domestic value add.

Having said that, ESG concerns and waste disposal issues pose challenges to these developments. For example, technical expert analysis elaborated the concerns faced in the nickel industry with tailings – where disposal was restricted due to Indonesia’s environmental protection obligations and tropical climate conditions. Further discussions also highlighted potential future steps to alleviate foreign investor concerns about environmental issues and satisfy constraints in developing infrastructure and technological capability.

To find out more, or to discuss any of these issues and better understand the implications for your business, please contact CRU using the button below.

Explore this topic with CRU