Author Ian Warden

Senior Analyst, Steel View profile

The insight below will analyse China’s ban on Australian coal and its impact on the domestic metallurgical coal and coal tar market.

A shortfall of met coal imports after China’s ban on Australia

The outbreak and spread of Covid-19 negatively impacted global metallurgical coal demand in 2020, resulting in a significant price drop in March. China was the first major metallurgical coal consumer to commence an economic recovery, helping make up for demand loss elsewhere around the globe from April. With strong economic growth in 2021 Q1, China’s coal demand is expected to be robust for the remainder of the year.

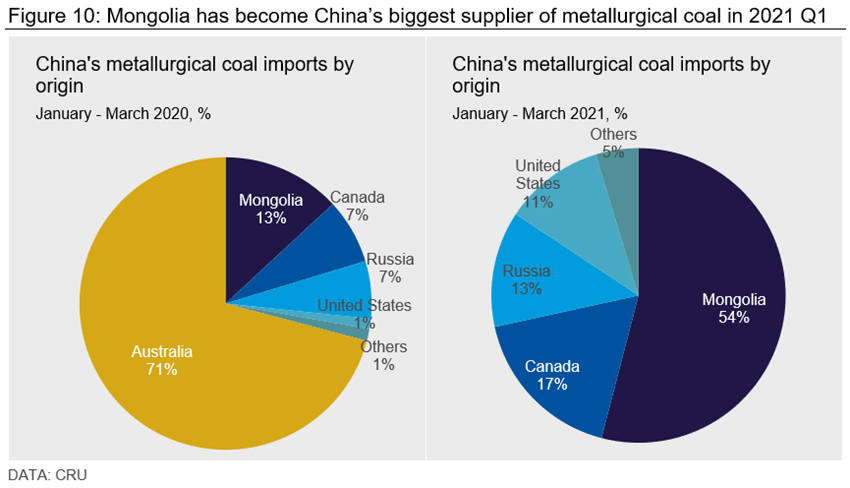

The restrictions on imported coal from Australia came into effect in October 2020 and continues to distort the global metallurgical coal market. China’s ban on Australian coal has resulted in higher prices for domestic supply and non-Australian supply landed into China, drawing supply from the Atlantic basin. According to trade data, Mongolia has replaced Australia and become China’s biggest supplier of metallurgical coal after the ban of Australian coal imports, meeting 54.1% of imports in the first quarter of 2021, up from just 13.1% in 2020 YTD. China has also increased its metallurgical coal imports from the United States and Canada.

However, China has seen an import shortfall with significant volumes of non-Australian supply unable or unwilling to switch into the Chinese market due to existing contracts. Without Australian supply, Chinese imports of metallurgical coal are forecasted to fall by 22 Mt this year, to 51 Mt. Consequently, metallurgical coal supply in China is very tight at this moment.

Meanwhile, China’s ban on imported Australian coal has also created a significant price premium for domestic metallurgical coal and non-Australian coal imports into China. According to CRU’s assessment, Chinese the price premium for Chinese metallurgical coal delivered from Shanxi into the key ironmaking province of Hebei has sat at ~$100 /t compared with the price that Australian coal would receive if It could be delivered into Hebei. This compares with a spread of less than $40 /t before to the ban.

Domestic coal tar price surges due to tight supply

There has been a greater shortfall in Chinese metallurgical coal imports than the decline in Australian exports. Market participants expect that increased domestic production will offset the shortfall. However, environmental and safety checks have been constraining this path to a balance market and the growth of metallurgical production in China has been restricted so far this year.

Rising metallurgical coal price, tight metallurgical coal supply and environmental restrictions at coke plants during the energy transition era have caused a decrease in coal tar supply in the domestic market. Coal tar distillers in major Chinese CTP producing provinces reported to CRU the current coal tar market is very tight as they are struggling to get these raw materials for CTP production.

Therefore, domestic coal tar prices have surged by RMB350 /t m/m to trade between RMB3,700-3,900 /t ($571-602 /t) in May 2021. The strong growth of coal tar prices and high utilisation rates at anode plants in China are driving domestic CTP prices after the Labour Day holiday (1 May 2021 – 5 May 2021), which have significantly increased by RMB1,050 /t ($167 /t) m/m to trade in the range of RMB4,800-5,200 /t ($741-803 /t).

Chinese domestic metallurgical coal production is expected to decrease over the medium term from 733 Mt in 2020 to 673 Mt by 2025, falling in line with declining hot metal output. However, in 2021, domestic production will increase by 14 Mt, to 747 Mt, to partially compensate for the shortfall in imports arising from the ban on Australian imported coal.

Coal tar supply will continue to be constrained as the current political signals do not indicate a relaxation of Chinas ban on Australian imports will materialise this year. CRU latest forecasts assume the ban is maintained through 2021. Therefore, coal tar prices will remain strong for the rest of the year. We also forecast higher CTP prices in the domestic and export market in Q3 and Q4 from Q2 levels as raw material prices will keep CTP prices robust in 2021 H2.

Explore this topic with CRU

Author Ian Warden

Senior Analyst, Steel View profile