Author Wan Ling

Head of Chinese Analysis, Aluminium View profile

Author Kevin Bai

Analyst View profile

Author Tianyu He

Senior Analyst View profile

Contributor Alex Tuckett

Head of Economics View profile

It details how these sectors will reduce and control carbon emissions from both the demand (consumption) and supply side (production). The fundamental solutions to decarbonisation are clean energy production and electrification.

China has set a strategy to ensure carbon emissions peak by 2030. During this transition period Chinese companies need to find solutions to reduce carbon emissions. Carbon neutrality before 2060 is the goal that China has pledged to achieve. The total carbon emissions (inc. land use, land-use change and forestry activities, LULUCF) in China reached approximately 10.5 billion tonnes in 2019. Carbon emissions from energy activities were estimated to be ~9.8 billion tonnes (or 87% of total emissions). Total carbon emission from China’s steel industry accounts for more than 15% of total carbon emission of the country.

The key to “peak carbon emissions” is to reduce and control carbon emissions from both the demand (consumption) and supply side (production) of commodities market. The fundamental solutions are clean energy production and electrification. Decarbonisation will significantly shift the energy source towards renewable energy and clean energy for steel, aluminium and copper. Electrification will largely alter the demand for steel, aluminium and copper in China, as these metals are used in the power generation, transmission and the manufacturing of new energy vehicles.

Structural shift to renewable and clean energy

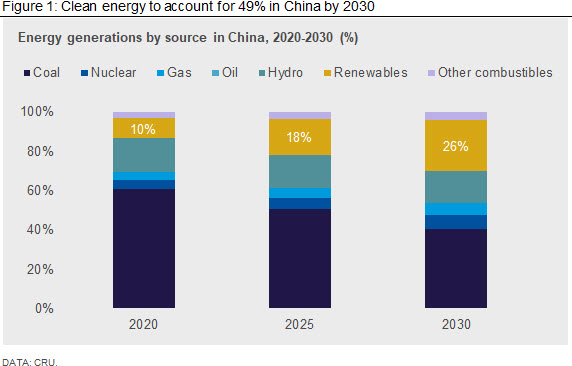

China’s clean energy production strategy is to develop and promote the use of clean energy such as solar power, wind power, hydro power, nuclear power and biomass, in order to limit the consumption of fossil fuels. According to Chinese government’s plan, energy generation from non-fossil fuels is expected to reach 20% by 2025 and 25% by 2030.

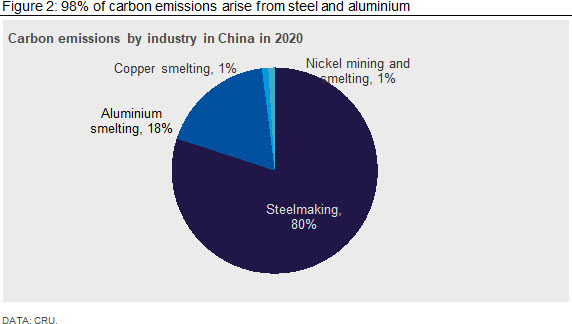

CRU tracks and models carbon emissions from the global metals industry on a plant-by-plant basis, including producers of steel, nickel, copper, aluminium, etc. Our modelled Scope 1 and Scope 2 emissions by industry in China can be seen in Figure 2.

The carbon emission from steel making and aluminium smelting accounts for 98% of the total carbon emission in the metals industry. Steelmaking alone accounts for 80% of emissions, with the aluminium smelting industry accounting for 18%. Therefore, it is extremely important for both steel and aluminium to find efficient way to reduce carbon emission.

Aluminium, structural shift to renewable energy, notably solar power

Around 16% of Chinese aluminium production now relies on renewable energy, primarily hydro power. This share is projected to rise to 27% by 2025 aided mostly by the development of new hydropower projects in Yunnan and Sichuan, and the shift of coal-based aluminium production into these regions. It is impossible for all aluminium smelters in China to shift to hydro power, as there is insufficient hydro power in China to support this electricity demand. Therefore, the journey towards carbon neutrality requires aluminium smelters to move into renewable energy sources, either from local grids or smelters will have to build bespoke solar and wind plants themselves. Such a transition is likely to take time, and large-scale usage of solar and wind power for aluminium industry has to be equipped by the strong power storage system. For instance, in Huolinhe of Inner Mongolia, solar power installations have been linked to the distributed grid for the smelters and now supply a portion of the power for the smelters there.

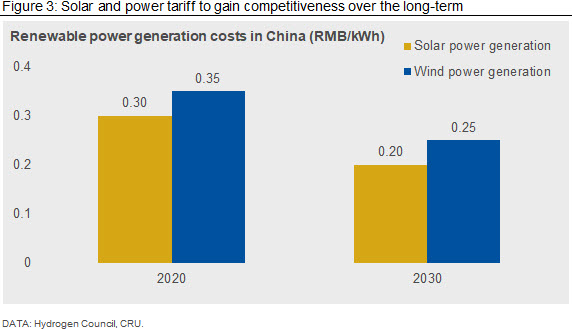

Benefiting from the abundant renewable energy resources in China’s northwest, northeast and southwest regions, the costs of solar power and wind power generations in China are comparatively low, currently at 0.3 RMB/kWh and 0.35 RMB/kWh. These two numbers are already lower than the costs of coal-fired power generation in some regions of China. By 2030, the costs of solar power generation and wind power generation are expected decrease further, to around 0.2 RMB/kWh and 0.25 RMB/kWh respectively. The carbon trading scheme will make solar power relatively more competitive against fossil fuels in future. Thus, the shift to solar and wind would also help provide cost competitiveness for aluminium smelting over time.

Steel, increasingly invest in CCUS and hydrogen direct reduction steelmaking

China’s coal consumption per ton of steel has fallen to a globally advanced level, and the iron and steel industry has largely completed its capaScity reduction program, a campaign to identify and close outdated and environmental unfriendly capacity of 140 Mt including induction furnaces. Therefore, there will be limited potential to reduce carbon emissions through these two methods.

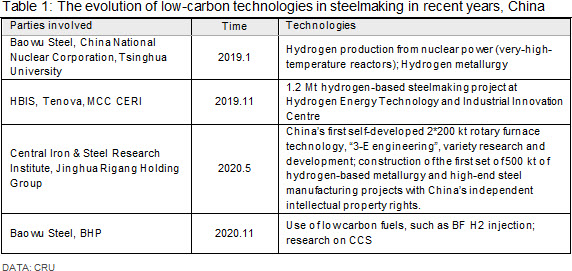

Carbon emission reduction in the future, is expected to be driven by approaches such as higher investment in environmental protection equipment (e.g., CCUS, Carbon Capture, Utilisation and Storage) and breakthrough in steelmaking technologies (e.g., hydrogen direct reduction steelmaking). China’s leading steel companies such as Baowu Steel and Hebei Iron and Steel Group (HBIS) have been actively conducting research on environmental equipment and innovative steelmaking technologies. However, these technologies are yet to be commercially viable in the Chinese iron and steel industry.

Electrification will boost demand for copper and aluminium

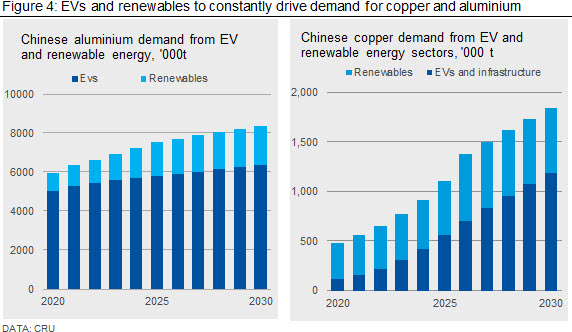

Aluminium, copper and steel are the very important materials in the construction of solar power and wind power. For instance, aluminium consumption is around 19,000 t in the construction of per 1GW solar power generation sets. Electrification is another important way to reduce carbon emission in China. New energy vehicles are an efficient way to reduce carbon emissions from the power usage end. Electrification also involves the construction of ultra-high and super-high grid construction, transmitting the solar and wind power from China’s west to east, linking the renewable energy generation and electrification. Both aluminium and copper are widely used in grid transmission, charger stations, solar wind, new energy vehicles etc.

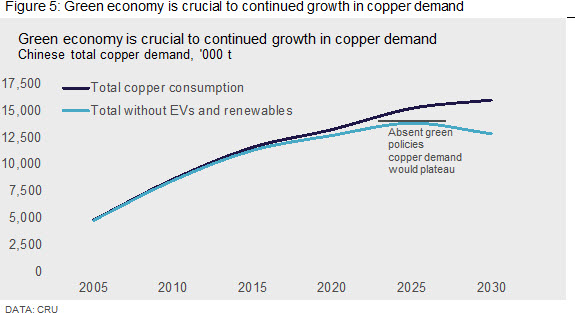

CRU estimates the aluminium demand in energy vehicles and renewable energy sector will grow by 40% to 8.39 Mt by 2030 from 6 Mt in 2020. Figure 5 shows that the demand for copper excluding EVs and renewables would plateau around 2025.

Chinese copper demand from EVs and renewable power will see high growth rates. However, these are from a low base level. These industries will see long-term sustainable development, pushing demand higher y/y. We forecast that Chinese copper demand from electric vehicles and related infrastructure will see a 26% CAGR over the next decade. The renewable energy sector will see strong growth over the next 10 years also, with copper used extensively in solar and wind capacity. There are two further uncertainties. One is the extent to which China can meet its copper needs from copper scrap. The other is the rate of substitution to other materials, such as aluminium, and thrifting.

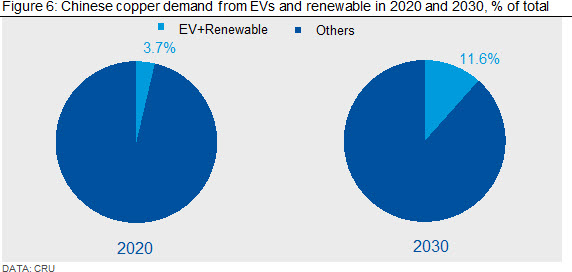

Against a background of policy and environmental support, EV and renewable power's share of total Chinese copper consumption will expand significantly. We forecast that by 2030 around 12% of China copper demand will come from these sectors, up from under 4% currently. These sectors will see further expansions in the following decades. It is no exaggeration to say that the future growth of the Chinese copper market is almost entirely contingent on a rapid green transition.

Greener policies drive quality over quantity for steel

CRU expects that Chinese steel demand has reached its peak or will peak shortly because the country is approaching a maximum level of sustainable floorspace and this is expected to slow construction of buildings going forward, see here for details (CRU subscribers only). Greener policies are still not constraining steel demand as the material is still required for housing, infrastructure and transport. While steel demand slows overall, developments in services and technology sectors suggest a shift in the focus of growth for to more advanced steel grades compared to the historical focus of steel products used in traditional construction of buildings and infrastructure, such as rebar and HR products.

For instance, the development of renewable energy is expected to become faster. China’s ambition for new wind and solar energy installation will generate a total of 120 Mt of steel demand in the next ten years. Although the annual addition is below 2% of total steel demand, this is a shift in the share of renewables in China’s energy mix from 28% to 47% over the same decade.

The development of renewable energy vehicle and light-weight requirement in EVs will also mean more high-strength and alloy steel demand than that of traditional type of vehicles. However, EV production was 1.4 M units as opposed to 25.2 M units of total auto production in 2020. Although existing plans on EV industry will mean a significant increase for EV production in the 5–10 years, it does not necessarily mean a significant jump in total steel demand in the auto sector. This is because EV car production remains a small share of total auto demand.

A journey defined by electrification and renewable energy

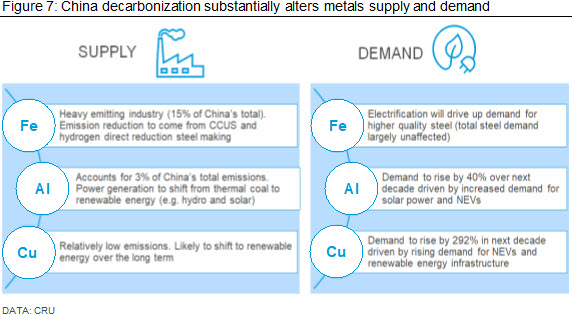

China’s journey to carbon neutrality will involve a major shift towards renewable energy. This is particularly the case for aluminium, where renewable power is expected to rise from 16% today to 27% by 2030. Solar power has the largest potential for growth in the aluminium industry. Hydrogen energy is expected to be widely used in the steel making sector, but for now these technologies are not commercially viable.

On the consumption side, decarbonization efforts require building a low carbon infrastructure on which the economy can operate – this includes smart grids, solar panels, wind turbines and electric vehicles – this infrastructure requires a lot more aluminum and copper. We expect consumption of aluminum and copper in low carbon infrastructure to increase by 40% and 292%, respectively between 2020 and 2030. Unlike base metals, total steel demand will not be a huge beneficiary of green policies, although there will be increased demand for certain niche metals.

Your journey towards carbon neutrality

Join industry leaders including Anglo American, Alcoa Corporation, Alumina Ltd, Constellium, Emirates Global Aluminium, Glencore, Sumitomo Corporation (SC), Vale, voestalpine AG and others who have already committed to reducing emissions with the help of standardised, high-quality emissions data and analysis.

Understand your value chain emissions and plot your course towards net zero. Learn more about the asset-level data and emissions curves readily available on CRU's new interactive web-based platform.

Speak to our team about CRU's Emissions Analysis Tool >

Schedule a demo with an analyst >

Explore this topic with CRU

Author Wan Ling

Head of Chinese Analysis, Aluminium View profile

Author Kevin Bai

Analyst View profile

Author Tianyu He

Senior Analyst View profile

Contributor Alex Tuckett

Head of Economics View profile