While the tax has been mooted in previous years, the challenging long-term prospect of the domestic FeCr industry has become more apparent this year because of increasing electricity costs. A further 15% increase in electricity tariffs by South Africa’s utility provider, Eskom, in 2021 as well as all FeCr smelters putting out section 189 redundancy consultations this year forced the issue to the Department of Mineral Resources and Energy (DMRE). While a chrome ore tax does protect South African smelting interests, any benefit could be negated by a retaliation from China or a loss of market share from conventional miners.

Alloy supported, but at what cost?

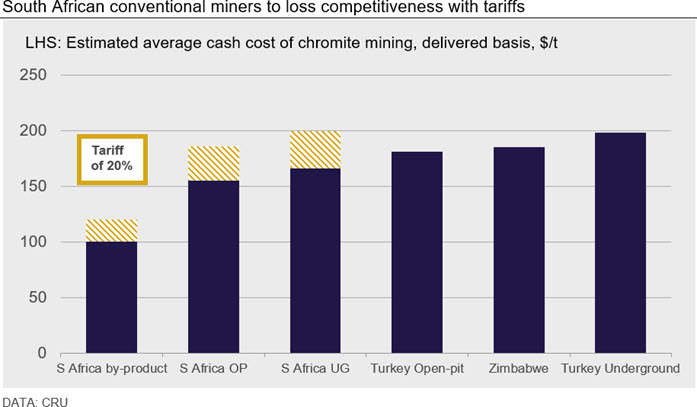

The proposed export tax on South African chrome ore is designed to support domestic FeCr production and its chrome value chain. The plight of the domestic smelting has persuaded the government to revisit the tax on chrome ore exports, which is hoped to make domestic capacity more competitive against their Chinese counterparts. Chinese growing use of by-product UG2 chrome ore and the rapidly increasing electricity tariffs in South Africa has supported the development of FeCr capacity in China. The impact of this tax will increase smelting costs in China, tipping in favour South African smelters. However, for chrome miners, the tax could erode global market share for South Africa’s conventional mines, as it will make them less competitive on a global basis.

An export tax could push South African conventional ore producers towards the higher end of the cost curve and above average costs in Turkey or Zimbabwe.

Longer term, this could shift mine investments away from South Africa. We could see Chinese operators becoming more global with their investments, in line with their belt and road strategy. In the near term, Turkey and Zimbabwe will not be able to ramp up to meet demand levels in China, and significant further investment is needed if they were to. However, Chinese companies could look at investments in these nations to increase capacity and provide chrome ore competitively to Chinese smelters, although South Africa has the largest chromite reserves globally. Zimbabwe is the second place contender and foreign direct investment over the years could be utilised to meet Chinese demand.

Even if the tax is implemented, South Africa will remain dominant in the chrome ore market, meaning that South African chromite will continue to form a large baseline of global supply. The tax offers South Africa a new source of revenue, which in turn could help ease Eskom’s ZAR488 bn growing debt pile.

China to feel the impact

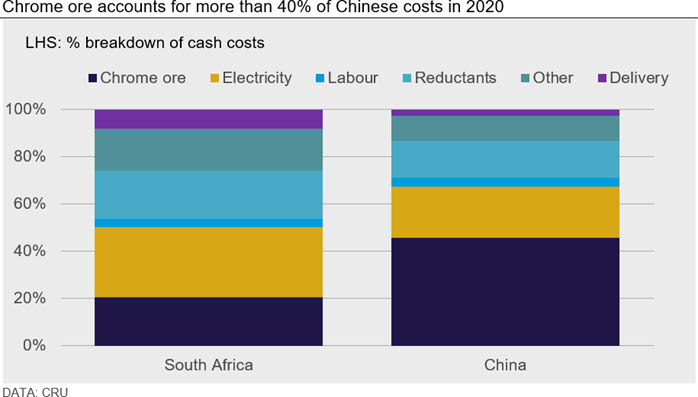

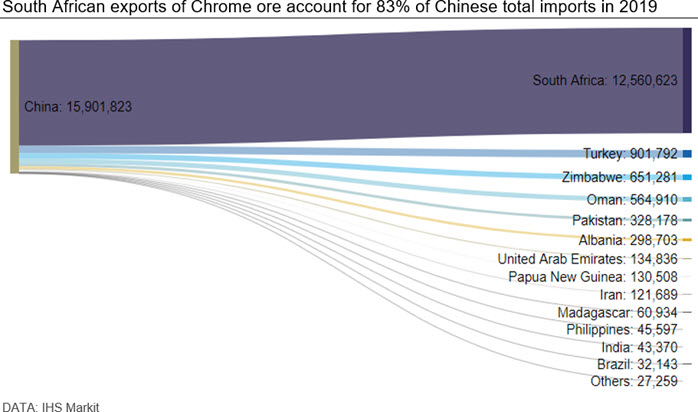

The impact of a tax on ore will inevitably raise smelting costs globally but particularly in China, as they are reliant on South African imports. In 2019, 83% or 12 Mt of China’s total chrome imports were of South African origin. Chinese smelting costs are heavily influenced by the price of chrome ore, while for South Africa energy is the key driver. Increasing costs at Chinese smelters would lead to lower production, particularly in Southern China, where costs are higher. In turn, this could lead to more imports of FeCr from South Africa.

CRU does not believe China will let this happen without some form of retaliatory action. This month’s reported ban on Australian met and thermal coal shows that China is not afraid to use the commodity trade to protect its interests. China has invested heavily to become more self-reliant within the stainless value chain and will likely act to defend this position.

Long term issues not addressed

Electricity tariffs from Eskom have increased by more than 500% (in ZAR terms) over the last 10 years to large industrial customers. This has hit their global competitiveness, for example we have seen the closure or mothballing of over 40% of South Africa’s ferroalloy capacity. A further 15% hike in tariffs is already approved for 2021, with additional increases expected in the medium to long term. The critical component of smelting competitiveness is the availability of a cost-effective and reliable electricity supply. The proposed tax on chrome ore may not save South Africa’s ferroalloy smelting industry if significantly higher energy costs materialise in the mid-term.

The market awaits further clarity from the South African government, so far, the rhetoric is ‘considering’ not ‘implementing’. With conventional miners expected to resist any attempts at imposing the tax and a retaliation from China expected the road to imposition could be long and unclear. Any ore tax will shift the global cost curve, putting Chinese smelting under pressure. In the medium to long term, increased investment in chromium mining in countries like Zimbabwe could chip away at South Africa’s market share.

Explore this topic with CRU

The Latest from CRU

Decarbonisation will reshape global steel trade flow

CRU’s Steel Long Term Market Outlook presents comprehensive analysis of global steel trade flows until 2050. Decarbonisation will play a significant role in redefining...