In this context, the EU Commission is planning to impose carbon border tax adjustment (CBTA) – a tariff levied on carbon emissions embodied in imported goods into the EU – to “level the playing field”. Such measures have significant potential to redraw the competitive landscape for these strategically critical industries. But their ultimate impacts are highly uncertain and substantively dependent on policy and market specificities. What does is mean for your business?

European metals markets under pressure with a fundamental policy shift seeming likely

The EU ETS scheme is fundamentally altering the economics of metals and fertilizer production in Europe. The European carbon price has rallied to over €25 a tonne of carbon dioxide (CO2), and is set to rise higher in the longer term, fundamentally altering the economics of metals and fertilizer production in Europe (see here for a more in-depth discussion).

With metal production costs in Europe – already high by international standards in many cases – rising faster than among producers in competing jurisdictions, the future of much of the European metals industries looks uncertain. It is likely that further policy reforms will be required to ensure sustained industrial activity in a higher carbon price world.

The EU Commission is plan¬ning to impose CBTA to “level the playing field”. The new president of the EU Commission, Ursula Von der Leyen, has made no secret of her plan to introduce a CBTA (a proposal that has long had support of powerful European stakeholders, including the French authorities). Officials are now understood to be drafting guidelines for potential carbon tariffs on steel, cement and power industries. Aluminium, copper and other base metals are also likely to fall under the eye of the policy makers.

How would a carbon border work?

A CBTA is intended to ensure that imported products are subject to the same carbon costs as domestic producers. In the simplest of terms, a CBTA would measure the carbon emissions embodied in imported products and levy a tariff equivalent to the difference between the carbon price in the exporter country and that prevailing in the EU on those emissions. Notably, it may also see a rebate on any carbon costs in the production of goods in the EU which are exported outside the union.

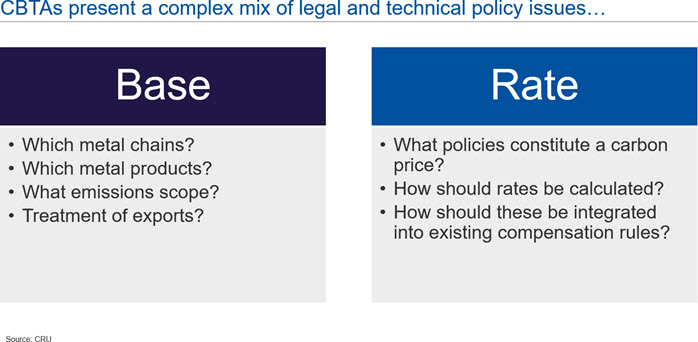

But the devil is in the detail, and there are a huge number of uncertainties surrounding the future design of any CBTA, including what should be subject to a tariff. Besides the rather obvious question of which industries should be subject to such a tariff – steel, cement and power being the preeminent regulatory targets (with aluminium and base metals industries following on close behind) – a key question relates to what products within any value chain should be levied. In theory, at least, the entire value would be subject to a tariff, but this raises a number of technical implementation issues.

The ability to measure carbon embodied in international metals and mining production is also a key issue. A set of robust technical benchmarks will thus be required to administrate a CBTA. The granularity and precision of these policy rules will be key in determining the impacts of any carbon-based tariffs. Can such rules accommodate, for example, heterogeneous carbon intensities within markets (a particularly challenging issue in downstream markets where feedstocks can be more complex, flexible and opaque), or will these be determined at the market level? More granular metrics, for example, would impact the most polluting exporters to Europe more than a single market wide benchmark.

Fundamental questions extend also to the CBTA rate. Current EU discussions are centred on the ETS as the key reference price for any CBTA (and therefore presumes that few imports are subject to any material carbon charge). However, WTO rules are likely to require consideration of all policies and measures implemented by trading partners as part of a fair comparison of carbon prices across respective countries. This raises deep questions regarding the treatment, not only of carbon taxes, but also wider fiscal policies, such as diesel and power excises and sales taxes/VATs, as well as potentially implicit costs of renewables support and other regulations.

What might this mean for businesses?

The impact of CBTA on businesses will likely depend on a range of trade, technology, market and policy issues, including:

- How important are exports to the EU? Firms operating in industries and segments with a high degree of trade exposure with Europe are most at risk of being impacted by a CBTA (see here for a discussion of key impacts in steel product markets)

- What is the potential for EU domestic supply response? The market impact will, in part, be determined by the extent of any domestic supply substitution, or, alternatively, increased export competition arising from any rebate on carbon costs on EU products sold overseas. This will be a function of spare capacity and related cost positioning and longer-term investment dynamics.

- Would businesses be able to pass any costs on? In the event that any CBTA only covers a part of the value chain (for example, primary products), there is the risk that EU producers incur higher input costs associated with CBTA but are unable to pass on their costs to their customers.

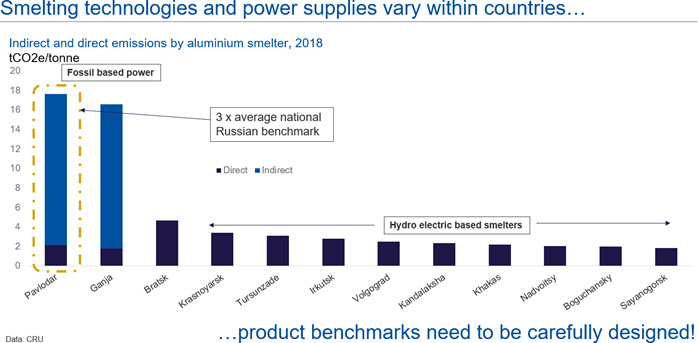

- How carbon intensive is your production and what product benchmarks would apply? The relative carbon intensity of metals production within and beyond the European Union determines the theoretical base of any tariff adjustment. However, the operation of any product benchmarks will determine the practical basis of any future levy. Whether or not relatively carbon intensive exporters to the EU will be subject to an accurate measure remains unclear. This is likely to be a key issue particularly in downstream markets and coal based primary producers operating in markets with extensive hydro powered production.

- Will EU producers continue to receive wider compensation for carbon costs? EU producers currently receive compensation in the form of free EU ETS allowance (see here for further details). Some electro-intensive base an d ferrous metals producers also receive compensation for higher carbon related electricity prices (see here for details). The expectation is currently that any CBTA would ultimately replace these support mechanisms.

- How enforceable is any measure? There are a number of key compliance risks. Notable among these is the risk that physical trade flows adjust in response to any CBTA with imperfect traceability on carbon costs. These risks are likely to be greatest in semi and finished product markets.

Getting ahead of upcoming regulatory impact assessments

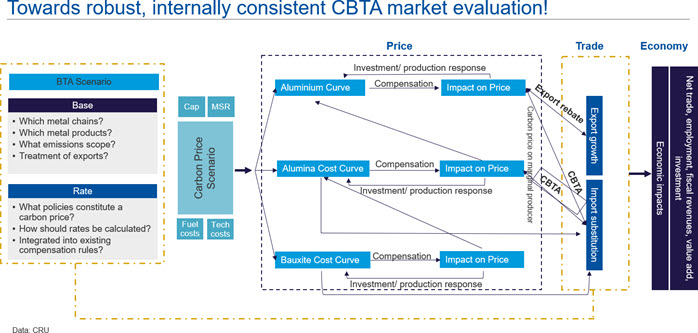

CBTA policy development is underway. The metals industry has a short window of opportunity to better understand the balance of risks and opportunities under different carbon border tax designs. This will be critical to both influencing the eventual shape of future regulation as well as adapting to the commercial impacts.

The Latest from CRU

Decarbonisation will reshape global steel trade flow

CRU’s Steel Long Term Market Outlook presents comprehensive analysis of global steel trade flows until 2050. Decarbonisation will play a significant role in redefining...