Co-author Willis Thomas

Head of CRU+ View profile

Co-author Adina Sholanova

Consultant View profile

The metal has positive electrochemical qualities that make its use advantageous on a technical level for all sorts of energy-related applications. That said, market participants interested in commercialising the soft metal’s new uses, have a major concern fundamental to any resource market: will there be enough supply? This Insight explores the resurgence of interest in tin along with the current supply outlook, including a review of the major risks.

Tin is a vital ingredient in the production of a wide range of products, though rarely represents more than a few grams per kilogram of final product. This includes computers and other consumer electronics, packaging, and in our automobiles. Due to this wide range of applications, total tin demand is driven by a combination of developments in the broader world economy. More specifically, tin demand is driven by the metal’s main use in the manufacture of solders, chemicals and tinplated steel, which account for just under 80% of total tin consumption.

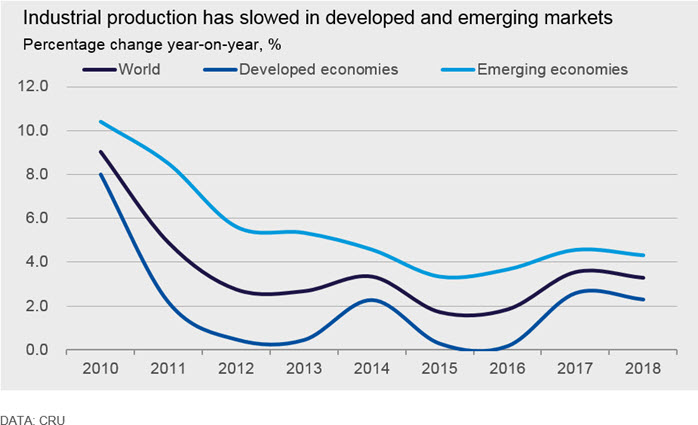

In recent years, manufacturing sectors around the globe have seen lower growth rates than found in the latter half of the 20th century and first decade of the 21st century, especially in developing nations where consumer electronics, along with many other tin-containing products, are concentrated. This has affected tin demand growth directly, especially in chemical and construction end uses.

Potential demand growth for tin sits tantalizingly close

Tin’s final role in new energy applications is far from set today, but the outlook is positive. Specifically, the International Tin Association’s (ITA) research has continued to support the potential for tin’s use in new energy1. The ITA details its recent research on potential new market opportunities for tin, including in the soft metal’s potential use in upcoming versions of the increasingly adopted lithium ion batteries, as well as in improved versions of the lead-acid battery. Growing production of electric vehicles could potentially increase demand of tin in lithium-ion batteries as well as in connecting the myriad new wiring needed in electric vehicles. Beyond this, 2018 saw the publication of the results of a report by the Massachusetts Institute of Technology (MIT)2, sponsored by Rio Tinto’s New Ventures Team, which also points to tin’s potential in new energy applications beyond the automobile. This includes the potential extended use of tin in robotics, renewable energy, as well as advanced computers and IT. With the publication of these studies, among others, there has been much recent interest in tin’s technical potential. It is expected that much of the new demand will include increasing uses of solder and other tin-containing materials for contact points, which are expected to rise exponentially in new energy uses.

From technical potential to supply reality

From the mid-1980s, the two key features of the tin mine supply situation have been:

- two decades of low prices relative to production costs which resulted in very low levels of exploration and investment in new tin mines, and

- more than half of total production coming from small-scale or artisanal operations which have high costs, variable output and a host of other issues.

Although mine production has risen in response to higher prices and stronger market conditions in recent years, the increase is mainly from expansions/extensions of old mines or improvements in ore processing technology – as well as the “black swan” of the return of Myanmar tin concentrate shipments to the market.

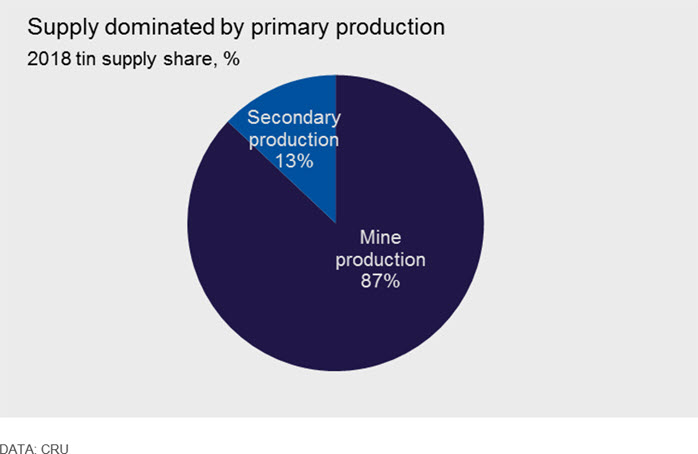

Over the last few years, world tin production has been relatively static. Refined tin production was between roughly 340,000 t/y and 370,000 t/y with primary (mined) supply making up between 80-85%, the difference between the two was filled by some 50,000 – 70,000 t/y of secondary (recycled) refined tin production.

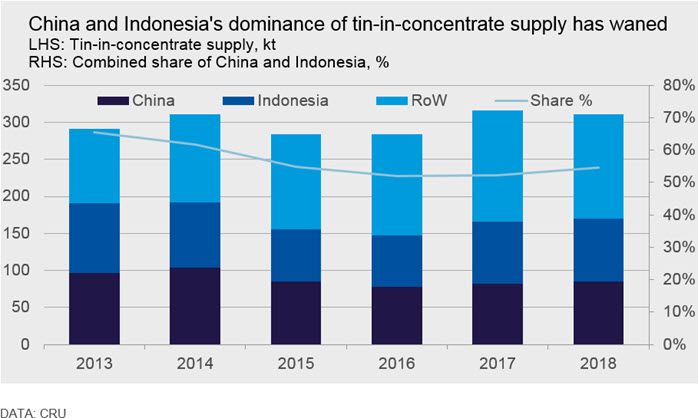

China and Indonesia dominate current primary supply

Most of the primary supply comes from two markets: China and Indonesia. Starting in the 1990s, these countries have figured as major refined tin and tin-in-concentrate producers – accounting for over half of tin-in-concentrate produced in 2018. In recent years, many small operations are being shut down as environmental and safety regulations have been tightened, a theme not likely to ease in the long-term. This theme has spanned markets and many commodities in China, not only tin. While the tin potential of China and its position as the world’s largest tin producer is not under threat any time soon, resources and reserves are gradually declining leaving the long term viability of this industry in doubt.

In Indonesia, producers have reported declining grades over the last decade which has resulted in rising costs and falling mine production. Regardless, the offshore alluvial deposits show potential and there is still new open pit mining being developed. However, production remains subject to significant uncertainty; particularly as Indonesian production levels remain highly sensitive to global tin price fluctuations and changes in regulation – over the past decade these risks have been realised disrupting export flows from Indonesia. Though difficult to forecast, regulatory and political risks should not be discounted again in this important supply market.

Evaluating market dynamics in these countries will not be straightforward for many operators and will require deep understanding of a range of issues including competitiveness impacts, price volatility and long-term policy risks.

Supply risks worry potential adopters of tin-based technology

More broadly, there are wider risks to tin market supply which concern those looking to commercialize new uses of tin in new energy applications:

- Existing mines are ageing, and ore grades are declining at a worrisome pace. For example, Peru’s only tin mine, San Rafael (1975 opening), has seen production from the mine declining from 39,000 t/y in 2008 to 18,300 t/y in 2018 due in large part to falling tin grades. San Rafael is far from the only example of falling ore grades and limited life of mines in the tin supply industry.

- The existing mine base is prone to disruption which, though true of all mineral extraction operations, does appear to happen with increased frequency in tin mines. A recent example is the tragic accident at the Baiyinchagan mine, Inner Mongolia, where a bus carrying workers crashed. It’s an accident which may put the mine out of action for up to 12 months – putting pressure on supply of raw materials as this mine produced around 8% of total Chinese production in 2018.

- Artisanal supply has assumed the role of a high cost swing player in the market in the past 10 years and has remained an important portion of tin supply. Artisanal supply is, however, considered variable supply which is politically and legally exposed to disruption. Even weather can affect their production more than ‘real’ miners. Further, these miners also help to cap price rises, discouraging some exploration investment.

- Responsible sourcing continues to be an issue as tin industry participants are becoming subject to increasingly demanding requirements from both their customers and new regulation to ensure they are sourcing tin responsibly. Tin, along with other ‘conflict minerals’ tantalum, tungsten, and gold (known as 3TG) originating in or near the DRC have been subject to increased supply chain scrutiny since the Dodd-Frank Bill in the US which requires the declaration of origin for these metals. While this is not a ban de jure, it is de facto a ban on DRC tin, though much of this material still makes it to market and is not declared as originating in the DRC. Further designations of ‘conflict’ regions, such as Myanmar’s Wa region, could greatly impact tin supply from these regions. There are efforts underway, with the aid of new technologies to improve the traceability of mined metals which may mitigate this specific risk to tin supply if applied to tin based minerals.

- The market is currently being supplied (and balanced) by Myanmar tin concentrate, whose return to the market after a protracted absence was described by many as a ‘black swan’ event. However, ITA has already noted that shipments from Myanmar to China fell significantly in 2019 relative to 2018 which were also down from 2017 levels. We expect to see a further fall in exports as the move to underground mining from mining from older depleted open cut mines increases costs.

- Today’s tin project pipeline lacks scale and “quality” to meet the supply gap at current prices. Few projects are currently in the feasibility-financing stage of development. Most hard rock projects have grades of 0.5-1% (or often less) with Bisie project in DRC the only exception with grades of <4%. This mine is in the final stages of construction leaving the remaining project pipeline cupboard even more bare. Fresh exploration for high quality, low political risk tin deposits is therefore required.

Due to these risks at a global level we believe that production from currently producing tin mines will be unable to sustain stable primary tin demand into the future. Despite the possibility of supply and other ‘black swan’ events there is still a real need for new investment in modern, sustainable mine projects – though prices must rise from current levels of around $19,000-20,985 /t to levels above $30,000 /t in the long term trigger this.

Endnotes:

- https://www.internationaltin.org/new-technologies/

- https://www.riotinto.com/documents/180321_Presentation_Andrew_Latham_Lithium_Battery_Metals_Conference.pdf

- CRU Insight: With the share of cobalt production from the DRC increasing, does Blockchain technology provide an adequate traceability solution?

- CRU Tin Monitor February 2019

Co-author Willis Thomas

Head of CRU+ View profile

Co-author Adina Sholanova

Consultant View profileThe Latest from CRU

Decarbonisation will reshape global steel trade flow

CRU’s Steel Long Term Market Outlook presents comprehensive analysis of global steel trade flows until 2050. Decarbonisation will play a significant role in redefining...