Physical market preferences for attributes of FOB US Midwest mill HR coil (HRC) prices have recently been established by independent market research.

Key findings are that weekly FOB US Midwest mill prices are regarded as more accurate than daily; a price being transaction-based is more important than being daily, including for the purpose of physical contract settlement; the reputation of the Price Reporting Agency (PRA) is important, as is the association of a physical price with a financial derivative (futures/options) contract.

Highlights

Physical market preferences for attributes of FOB US Midwest mill HRC prices have recently been established by independent research of the market at large. The physical steel market in North America remains committed to CRU’s FOB US Midwest HRC price, according to these findings, which in summary are:

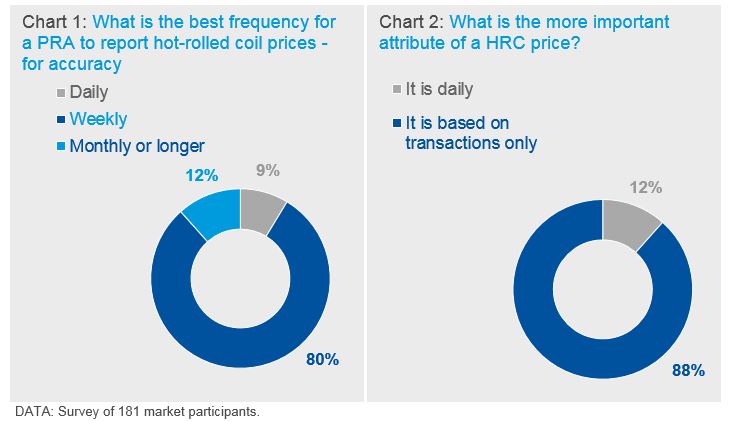

- Weekly FOB mill US Midwest prices are regarded as more accurate than daily, with 91.3% of survey respondents indicating this as their view;

- A price being transaction-based is more important than being daily for the purpose of physical contract settlement in 88.4% of answers;

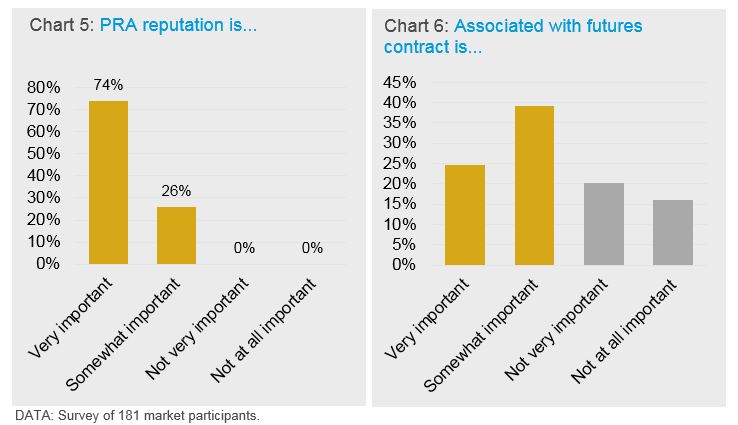

- The reputation of the Price Reporting Agency (PRA) is considered important to all responders, with 73.9% rating this as ‘very important’;

- The association of a physical price with a financial derivative (futures/options) contract is seen as important or very important by 63.7% of responders.

Research objectives and methodology

CRU has a long-established and proud history of serving the market with its US Midwest prices, but index-based pricing has moved in and out of favour, and alternatives to CRU prices have presented themselves. CRU welcomes all forms of choice in the market. With this context, CRU commissioned third party research in order to clarify current attitudes towards price frequency, methodology and use of financial derivative contracts by the industry. We commissioned similar research in 2015 and this year we repeated and extended it to help ensure CRU's services continue to meet market requirements.

Methodology

The scope of the survey was the FOB US Midwest mill physical HRC market, and therefore the sample was of North American physical market participants. A privately-owned independent global market research company conducted the research in February-March 2019. The research and responses were anonymous, meaning the company commissioning the research (CRU) was unknown to the research subjects. In addition, the answers given by research subjects could not be matched with the identity of the respondents. The research was conducted by means of SurveyMonkey and telephone interviews. 51% of individuals asked to participate were not CRU customers.

Results

Frequency – weekly preferred

The quantitative survey results show that the physical market prefers weekly pricing for FOB mill/ex-works HRC pricing. The overwhelming majority of physical market participants prefer weekly or less frequent pricing both from the perspective of accuracy (Chart 1 below) and in terms of how the data is used in their business.

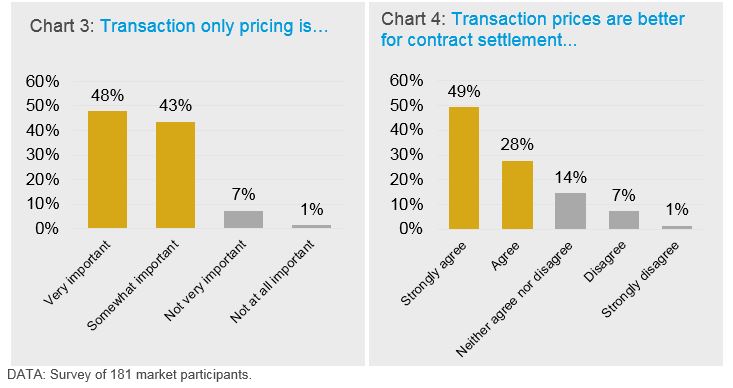

In addition, most survey participants rated a price being solely transaction-based as more important than it being daily (Chart 2).

Qualitative comments related to concerns over liquidity, noise or volatility, accuracy and potential subjectivity of daily FOB Midwest mill prices and included:

- “There aren't enough transactions per day to publish a daily price.”

- “Daily prices can't accurately show changes, to be able to tell a trend.”

- “Daily transactions cause noise and without a quantity referenced are easily manipulated…”

- “…there's too much speculation and volatility in the day to day prices.”

- “…the market isn't big enough for a daily number - most of it is noise.”

Transaction-based prices preferred

The data suggests that physical market participants have a strong preference for transaction only-based pricing only (Chart 3), in particular for the purpose of physical contract settlement (Chart 4).

Qualitative responses related mainly to transaction prices being the real and proper measure of the market and included the following:

- “In this industry, sometimes it's a rumour mill - you have to separate that from what's actually occurring. Transactions are the best measure of what's actually happening.”

- “Anyone can put an offer or bid out there in the market, but it doesn't mean anything until money is actually exchanged.”

- “I want to know the real price, based on people writing real checks. People can throw out flyer bids or offers which add noise that's incorrect.”

- “…transactions are real data, even if it's lagging.”

- “Actual transaction data truly shows what people buy in-market. It eliminates uncertainty.”

- “[Transaction pricing is] pure mathematics of what's going on in the market. Otherwise it's just hypothetical.”

PRA reputation critical

All survey respondents (100%) indicated that the reputation of the PRA was important (Chart 5).

Qualitative responses made reference to CRU prices on themes of the value of cross-commodity/market understanding and perspective, acceptance, reputation and transparency. These include:

- “CRU is more legitimate than [competitor] and others. The international outlook on CRU is strong/credible. Other commodities show they know.”

- “CRU has a global pricing perspective and is more balanced.”

- “CRU is more widely accepted… …they're an older name, people are more familiar with them.”

- “CRU is the go-to - it's their reputation, their name recognition. "Index" and CRU are synonymous.”

- “We recommend CRU right now, only because it seems to be the most accurate in a field that is not as transparent.”

The importance of financial derivatives

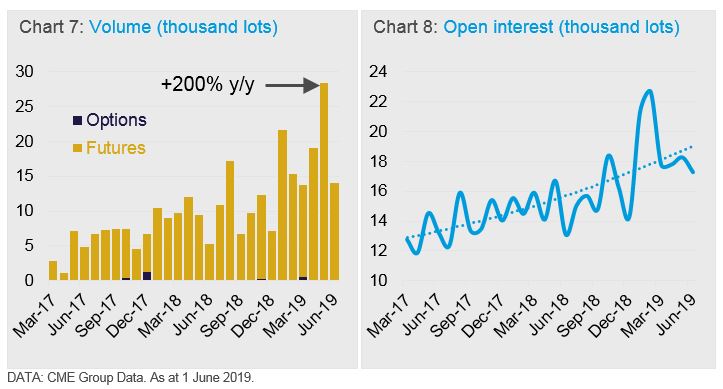

Being associated with a financial derivative contract is seen as important (Chart 6 above). Research findings included evidence of use of the CME’s CRU-settled HRC contract.

This has seen substantial growth in use in recent years and on into 2019 (Charts 7 and 8):

Conclusions

The 2019 research results suggest there is broad alignment between physical market requirements and attributes of CRU’s US FOB Midwest mill HRC price in that the preferred frequency is weekly, with transaction-only based pricing vastly preferred. PRA reputation was deemed critical, and qualitative market responses on themes of the value of cross-commodity/market understanding and perspective, acceptance, reputation and transparency also suggest broad alignment with CRU’s approach.

Finally, being associated with a financial derivative contract is regarded important for the majority. The CRU-settled CME futures contract use has grown rapidly, meeting hedging and other trading needs. Our financial stakeholders are important, and CRU will continue to seek to meet the price requirements of the entire market going forward.

For more information on CRU’s price, analysis and forecasting services and how they can help your business, please submit the form below or email steel@crugroup.com.

Explore this topic with CRU