Co-Author Ian Hiscock

Head of Consulting, China and South East Asia View profile

Currently, uranium production assets can remain cash positive thanks to long-term contract prices that are usually above spot prices. However, utilities around the world are increasing their share of spot contracts due to low prices. In this environment, vast accumulated uranium stocks are positioning China as a market maker and depressing uranium prices. China will make the most of the favourable (low) uranium asset prices to continue acquiring overseas assets for long term supply security and meeting its growing reactor uranium demand.

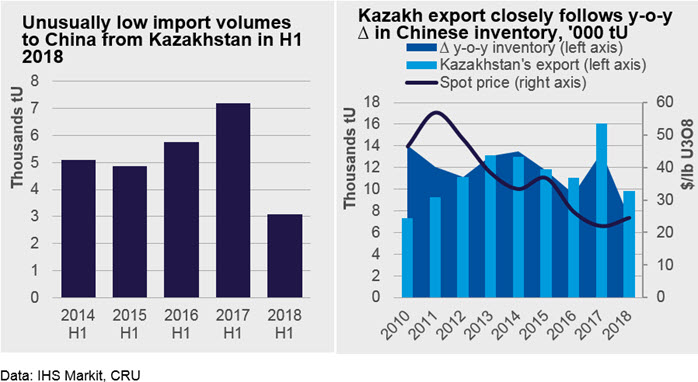

China has decreased uranium purchases following unprecedented supply cuts in 2018

In November 2017, McArthur announced a 10 month shutdown, then in December 2017 KazAtomProm announced a 20% supply reduction from Kazakh mines, prompting a 19% jump in uranium spot prices from $19.9/lb in late October 2017 to $23.7/lb U3O8 by the end of the year. In response in the first half of 2018, Chinese utilities substantially decreased uranium purchases and inventory accumulation fell to the lowest level seen since the start of China’s inventory build up in 2010.

Historically, Kazakhstan supplied Chinese spot purchases and production was closely aligned with inventory accumulation volumes in China. Already in a first half of 2018, uranium imports from Kazakhstan to China has halved. As a result, uranium prices fell slightly from $23.7/lb U3O8 in January 2018 to $22.7/lb U3O8 in early July 2018. It was only the subsequent July 2018 announcements of the Yellow Cake IPO and indefinite shutdown at McArthur mine that has pushed prices back up from $22.7/lb U3O8 to $25.7/lb U3O8 during July 2018.

We believe Chinese utilities were cautious not to spark major bull sentiment in the market, thus inflating prices, which possibly would have provided a lifeline to marginally costly mines.

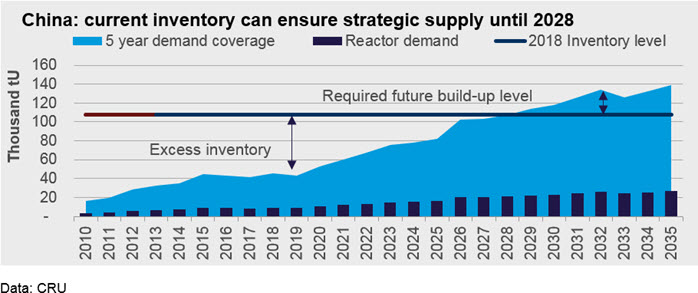

Future Chinese uranium purchases will be less driven by inventory accumulation

Going forward, we expect underlying trends in China for reactor demand and strategic supply to support uranium purchasing.

The Chinese government does not provide any explicit policy guidance on what it considers as an optimum uranium inventory level. CRU assumes that a satisfactory level of Chinese uranium inventories would cover 5-years demand1 . In comparison, demand coverage in the West is historically 1.5 to 2.5 years, while in Japan it remained at 7- 8 years in pre-Fukushima.

The current inventory held by Chinese utilties is sufficient to provide this 5 year buffer until 2028. To maintain this coverage level in 2035, China will only need to add ~31,400 tU to its inventories in the period. This just amounts to an additional 1,845 tU per annum above actual demand over the forecast period.

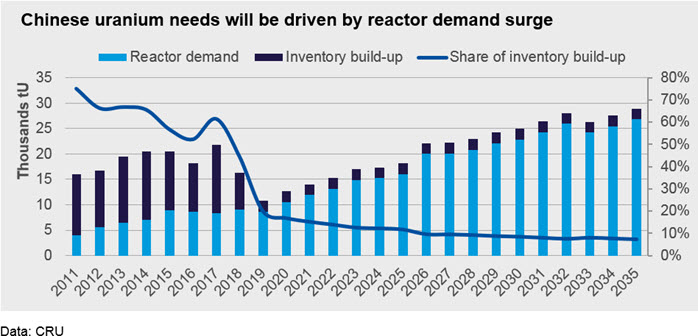

Reactor demand will be the main driver of future Chinese uranium procurement2

Until 2018, inventory build-up accounted for more than 50% of Chinese uranium purchases but surging reactor demand will be far more important driver for future purchases.

Chinese reactor demand is estimated to grow at 7.4% CAGR from 8,600 tU in 2019 to 26,800 tU in 2035. This means that with the required inventory build, Chinese procurement will have to average 20,800 tU/y in 2019-2035 period. In comparison, it averaged 18,700 tU in 2011-2018 period. Without adequate supply security from uranium mines, Chinese utilities will be highly exposed to uranium market over the long-run.

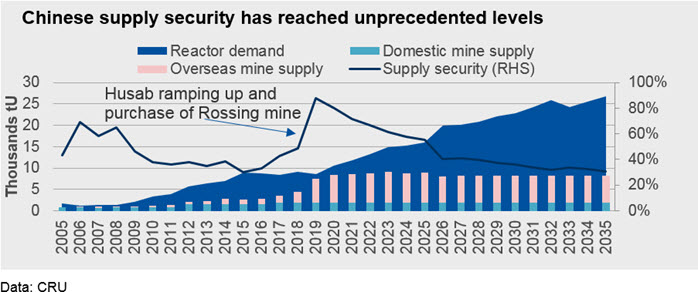

China will need more overseas assets to decrease long-run exposure to the market

Domestic and Chinese owned overseas mine supply accounted for just 42% of Chinese reactor demand in 2017. It was projected to cover only 68% in 2019 but the Husab ramp up and the recent acquisition of the Rossing mine are expected to improve supply security in medium term to 88%.

This will also make it easier to accumulate inventories in the medium term as China will need to buy less uranium from the spot market. It will however continue to acquire more assets, as supply security is expected to revert to previous level, primarily due to the Rossing mine running out of resources by 2025 and the continuing reactor demand surge.

Suppressed uranium prices facilitate cost effective purchase of overseas assets

The purchase of Husab occurred directly following the Fukushima incident, despite ongoing concerns, Chinese utilities proceeded with the purchase, indicating the strategic necessity of supply security.

Since then Chinese utilities have bought several other small scale mines. However, in 2017, CNNC rejected the purchase of the remaining 75% stake of the Langer Heinrich mine which was struggling to remain cash positive. This suggests that Chinese utilities are balancing the cost effectiveness of purchases with their strategic supply imperative.

Most recently Chinese utilities purchased a 69% stake at Rossing mine for a down payment of just $6.5 mln USD, that could rise up to $106.5 mln USD depending on profitability of the mine and the price of uranium until 2025. This is beneficial for Chinese utilities:

- This transfers price risk to the seller

- The pressure from the spot market will be relieved, as the supply security reached 88%, Chinese utilities will need to procure only small volume from spot market in short term

- It is also probable that Rossing would have been idled without this purchase and push the price for uranium up, given that it is running out of long-term contracts and the sale on spot market will have been unprofitable

There is no doubt that attempts to acquire more assets by Chinese utilities will continue in order to ensure long-term supply security and continuing environment of low prices will serve to facilitate this process for Chinese utilities.

Concluding notes:

In 2018, closure of McArthur and other mines tightened the uranium market. Currently, more than half of idled capacity is at McArthur River, which is considered to be low cost mine. CRU expects that mine reopening will only occur at sustainable spot price of $35-$37/lb U3O8. Delaying the market in reaching that point remain the vast accumulation of Chinese uranium inventories. There will continue to play a significant role in providing downward pressure to the market, while Chinese utilities attempt to acquire more good value overseas uranium assets.

Endnotes:

- Demand coverage, which is defined as inventories expressed as a multiple of the demand in that year. Thus, it is the number of years for which the inventory can cater to a given annual demand

- Uranium procurement = reactor demand + inventory accumulation

Co-Author Ian Hiscock

Head of Consulting, China and South East Asia View profileThe Latest from CRU

Decarbonisation will reshape global steel trade flow

CRU’s Steel Long Term Market Outlook presents comprehensive analysis of global steel trade flows until 2050. Decarbonisation will play a significant role in redefining...