Author Caroline Alglave

Senior Analyst View profile

The reduction of free carbon permit allowances to smelters will raise smelting costs for the average smelter by $10-$25/tAl depending on final EU policy decision. The increasing permit price will also drive indirect carbon costs higher, but the effect varies greatly from smelter to smelter.

The EU Emissions Trading Scheme (ETS) has directly included aluminium production since 2013. Before this the aluminium industry had only faced added costs from the EU ETS in the form of higher power costs, this is known as indirect emissions costs. I.e smelters were forced to pay more for power due to emissions costs associated with power generation. In 2014 EU leaders agreed a binding target to reduce GHG emissions by 40% from 1990 levels by 2030. To achieve this objective the EU announced planned reforms of the ETS stage four from 2021-2030. The major change of the policy is the increasing rate at which permits will be removed from the carbon market, rising from 1.7% to 2.2%.

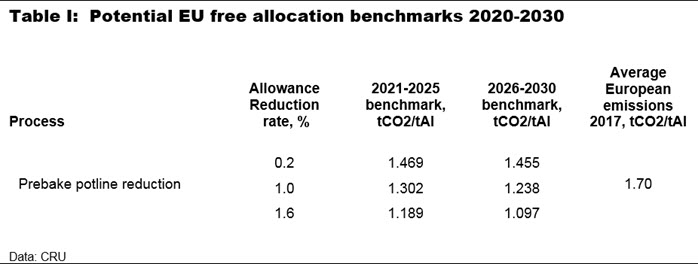

Aluminium producers receive an allowance of free emissions permits per year. Free allowances are provided to protect the industry from substantial cost increases and avoid production moving overseas to regions without carbon pricing, a process known as carbon leakage. There are a different number of free permits for anode plants, reduction potlines and casthouses. Here we only consider the reduction process, as emissions costs from the other two processes are minor on a per tonne of aluminium basis. Anode production and casthouse emissions account for 15% and 3% respectively of direct emissions at a smelter, but the benchmark for Anode production is relatively stringent and thus the cost is minimal on a per tonne of Aluminium basis. The free permits a smelter receives is based on a benchmark amount across the industry set by the EU. For phase 3 (2013-2020) this was set at 1.514tCO2/tAl based on the top 10% of EU installations in 2008.

Under current proposals, in phase four, two new benchmarks will apply, one for the years 2021-2025 and one for 2026-2030. The two benchmarks will be calculated by reducing the original benchmark by a factor between 0.2%-1.6% for every year between 2008 and the midpoint of the respective period. Table I shows the potential free allocation benchmarks this could result in and the emissions of the average EU smelter in 2017. The reduction rate for each process is yet to be decided by the EU and will be based on the ability of an industry to reduce emissions intensity. For aluminium smelting, CRU would expect a relatively low reduction rate as efficiency gains can be hard to achieve and most of the readily achievable efficiency savings have been made already.

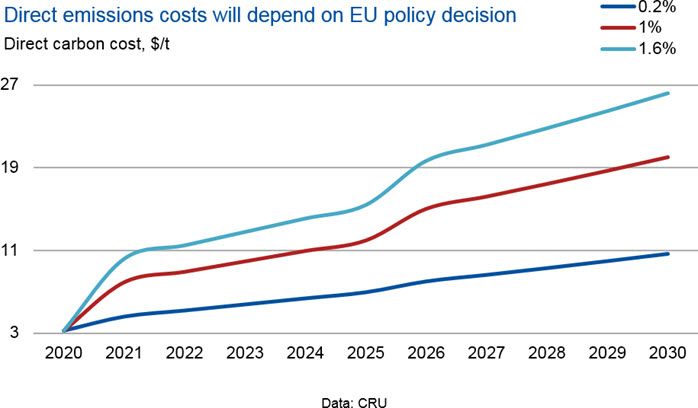

Below is a graph showing the carbon cost from direct emissions which the average 2017 European smelter would face from 2020-2030 under three different allowance reduction rates. EU ETS permit prices forecasted by CRU Economics have been used. Even if granted the most lenient allowance reduction rate of 0.2%, by 2030 the average EU smelter would incur over $10/t of direct emissions cost. At a reduction rate of 1.2% the cost is over $25/t.

The graph above only considers direct emissions costs. Aluminium smelters are also exposed to indirect emissions cost as power costs increase due to carbon pricing. The aluminium industry has been able to negotiate a compensation scheme for these indirect costs. The scheme is on a national basis and is not compulsory, the amount of compensation varies country to country. Under the EU ETS reforms, compensation of indirect carbon costs is encouraged but there are no rule changes that will have an effect. As a result, the effect of increased carbon permit prices on indirect carbon costs will continue to vary substantially from smelter to smelter. For more information on indirect power costs, CRU includes smelter specific discussions in the Aluminium Power Tariffs Service and the effects are modelled in the Aluminium Smelting Cost Model.

Explore this topic with CRU

Author Caroline Alglave

Senior Analyst View profileThe Latest from CRU

Decarbonisation will reshape global steel trade flow

CRU’s Steel Long Term Market Outlook presents comprehensive analysis of global steel trade flows until 2050. Decarbonisation will play a significant role in redefining...