Our client, a major phosphates producer, was interested in gaining a better understanding of how to price phosphorus units used in the production of lithium iron phosphate (LFP) type cathodes for lithium-ion batteries.

Author Juan Brihet

Senior Consultant View profile

Contributor Piyush Goel

Consultant View profile

Contributor Garrett Haffner

Consultant View profile

Contributor Alex Laugharne

Principal Consultant View profile

Contributor Ionut Lazar

Principal Consultant View profile

The LFP industry is growing rapidly, and therefore has been identified by many major phosphate producers as a potential market for their product. This means that developing a deeper understanding of potential pricing mechanisms for high-purity phosphate in LFP production could be key for decision-making in relation to new business opportunities.

This client approached CRU looking for a comprehensive study that investigated current pricing schemes and market dynamics across the LFP value chain, provided opinion on prospective future changes, and described analogous situations in other cathode raw material markets such as lithium, nickel, cobalt and manganese.

How did we answer the key questions?

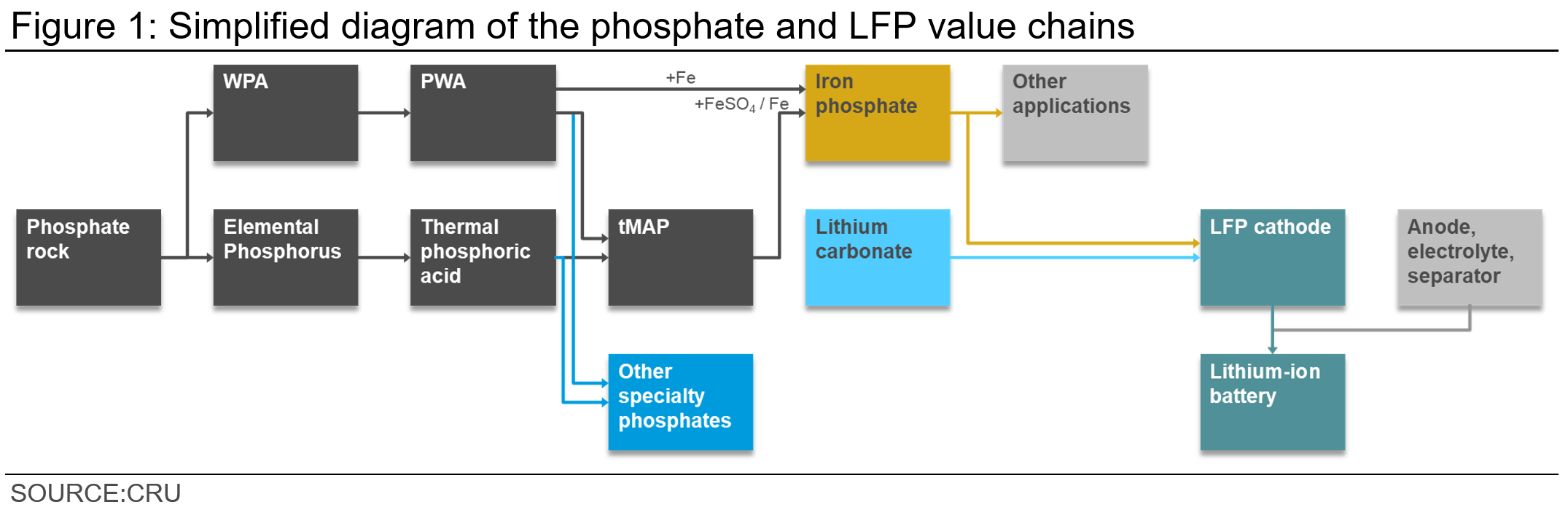

The starting point was to provide a detailed analysis of the LFP and electric vehicle (EV) value-chain for our client. We presented the different lithium-ion battery cathode chemistries with a focus on LFP, and then introduced an overview of the main LFP production methods. This allowed us to highlight the role of phosphorus in the production – and specifically the cost structure – of LFP, and to identify key intermediate products such as iron phosphate.

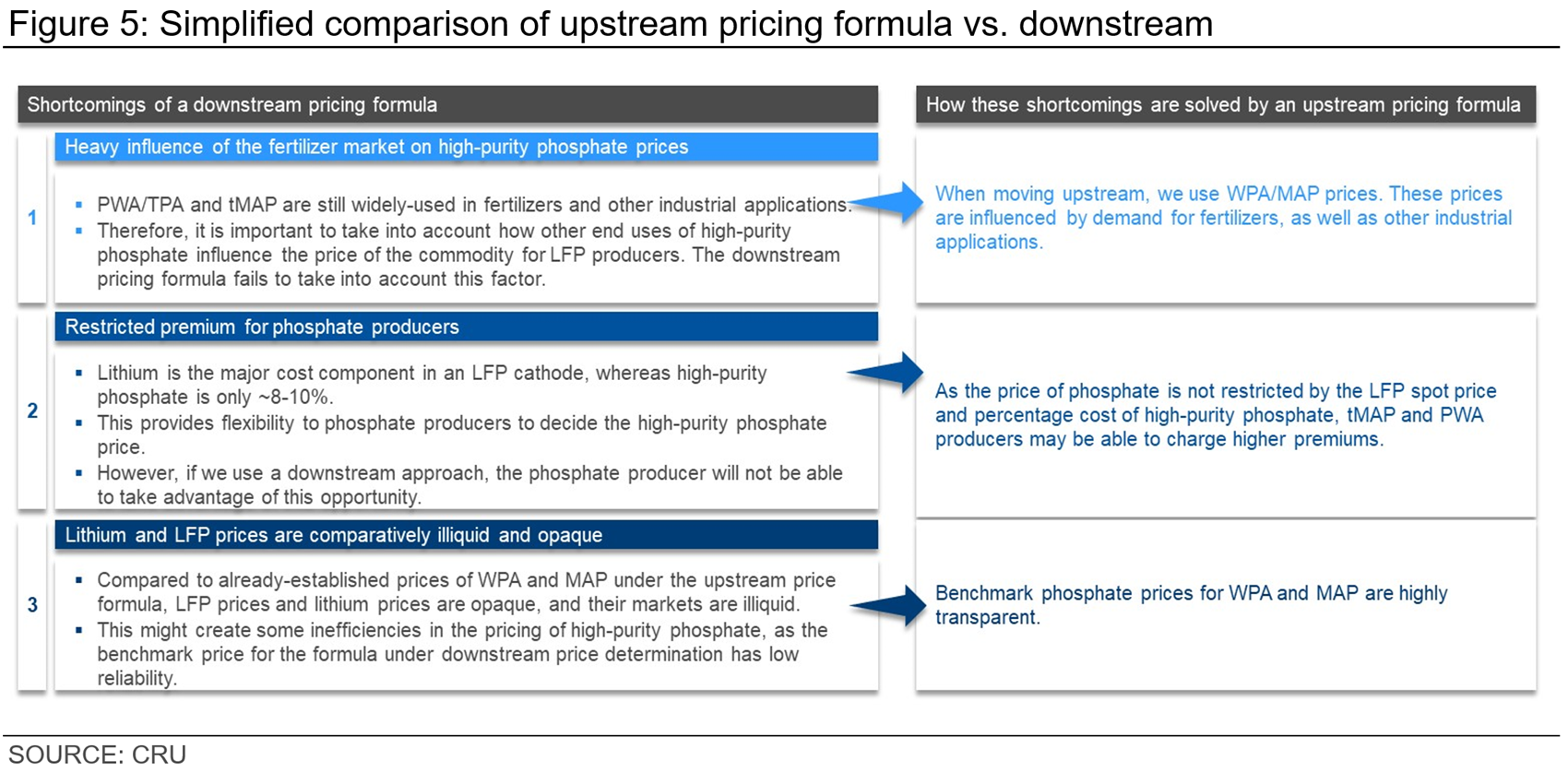

We also identified key underlying and more transparent price benchmarks within the existing fertilizer value chain, such as MAP (monoammonium phosphate) and WPA (wet phosphoric acid) price benchmarks for tMAP (technical MAP) and PWA (purified wet acid) prices, respectively. This corresponded to our goal of increasing the transparency associated with tMAP and PWA, by using the more widely transacted products and their greater levels of market transparency.

Secondly, we conducted a deep dive into the Chinese LFP industry. This was of great interest to our client as China currently accounts for 99% of global LFP cathode material supply, and is highly concentrated, with only a small number of large-scale producers. CRU believes that the dynamics in this market will have a significant impact on the future development of the industry outside of China, not only because it provides a guide for how the industry might develop in regions such as Europe and North America, but also because the risk of possible overcapacity in both the Chinese iron phosphate and LFP markets increases the potential for exports of these products.

Moreover, we presented several case studies of different types of partnerships across the LFP supply chain in China, in order to help our client to deepen its understanding of how the relevant major players are defining their market strategies within this industry. We identified various phosphate producers that are currently developing partnerships in order to enter the LFP industry, and benefit from:

- a guaranteed offtake for their PWA or tMAP;

- a stable supply of other raw materials such as lithium;

- access to technical expertise provided by existing industry participants;

- and increased reputability in the value chain up to LFP cathode manufacturing.

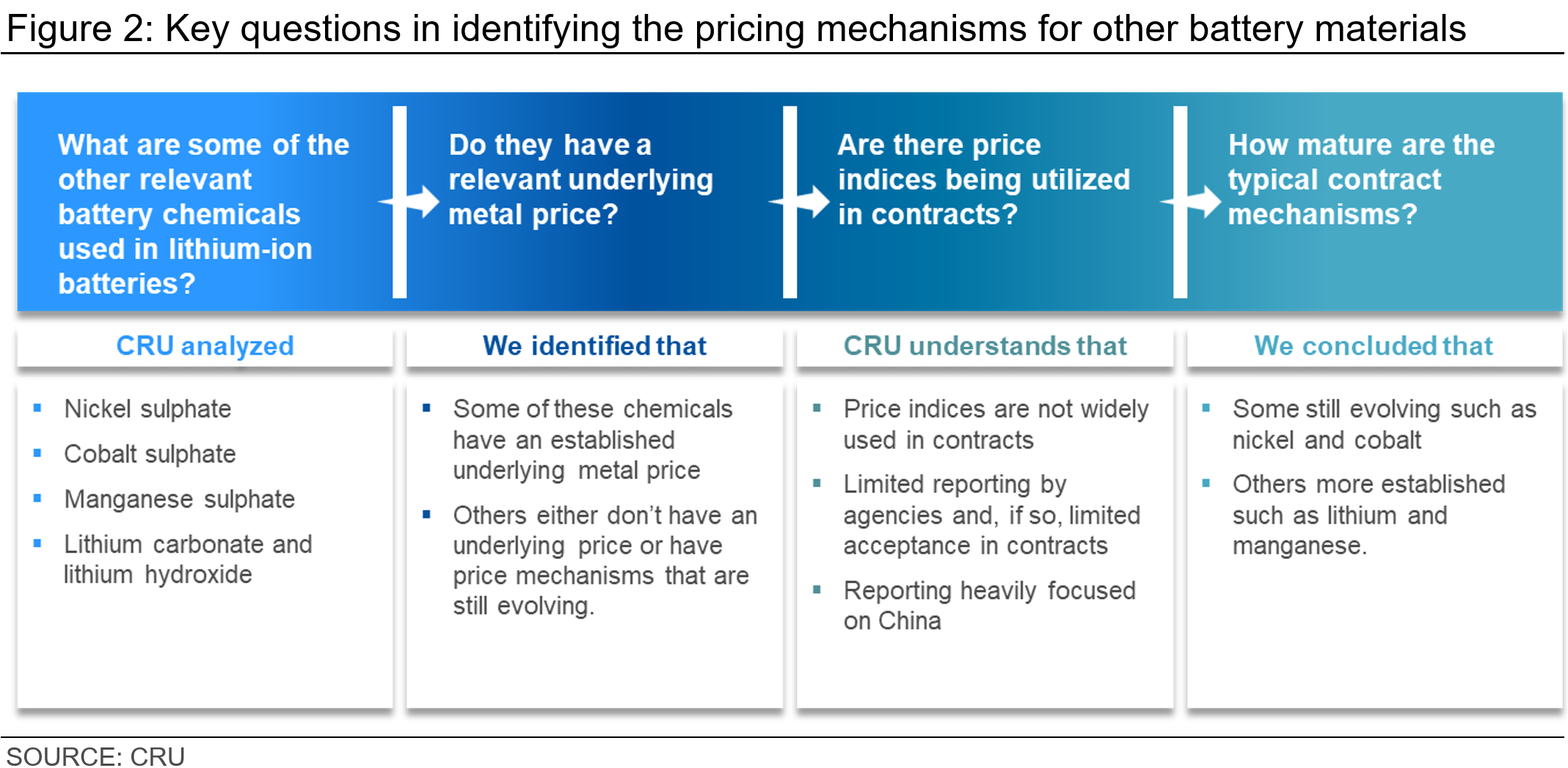

Thirdly, we provided a detailed analysis of pricing mechanisms currently used in other battery raw materials. Due to the illiquid nature of these markets, a variety of pricing schemes are used for different battery chemicals as there is no globally accepted price index. We provided individual price analysis, and the drivers behind those prices in the form of four case studies: lithium, nickel, cobalt, and manganese – all of which have different pricing mechanisms currently. Thanks to this analysis, our client was able to better understand how other battery materials are priced in related markets, and how this may be relevant for the pricing of high-purity phosphates for LFP production.

Finally, we developed a comprehensive analysis of possible approaches for pricing high-purity phosphates for LFP battery manufacturing, which represented a key part of the recommendations that we provided to our client. An overview of our approach is provided in the following section.

Cost analysis and similarities with other battery material markets

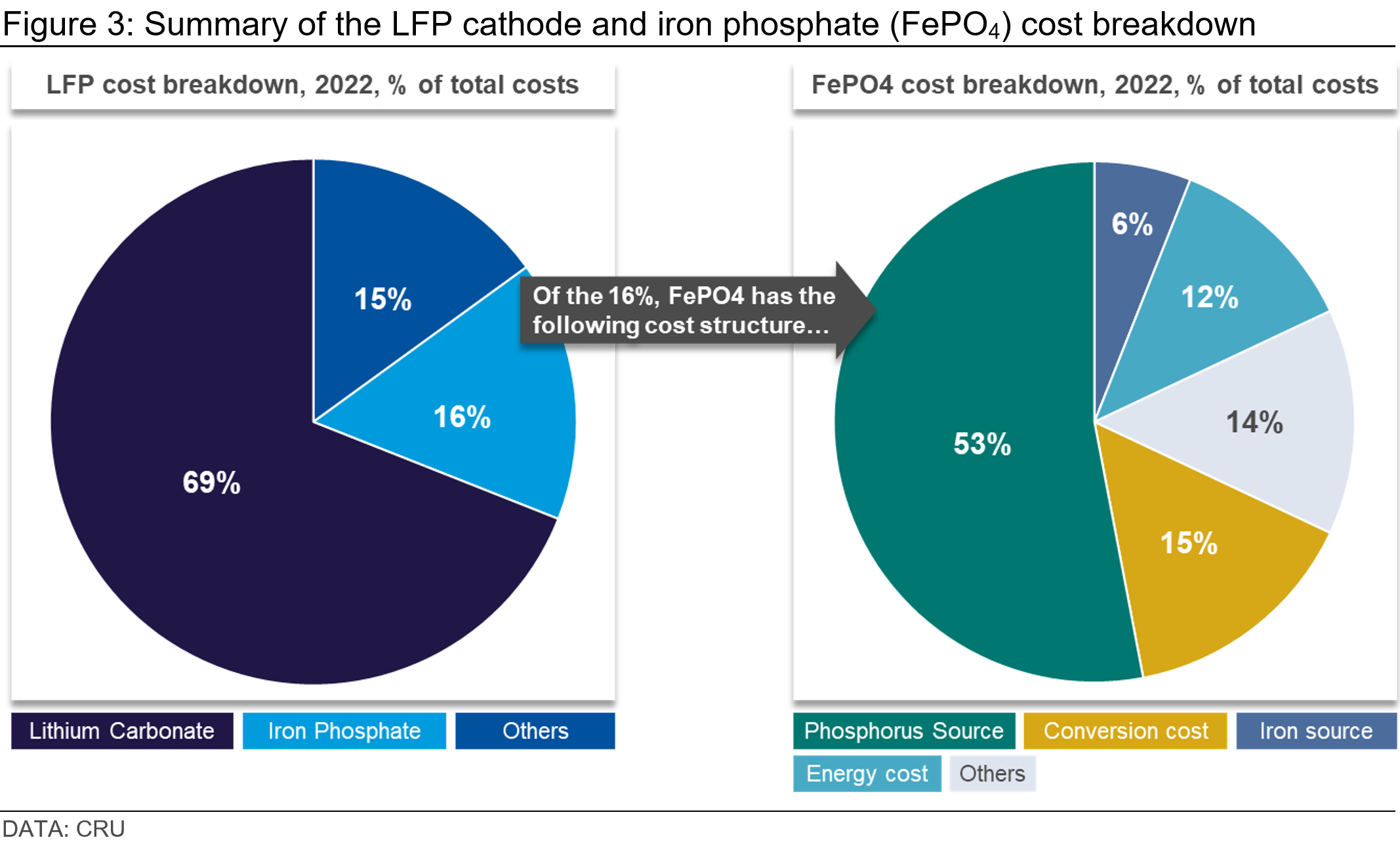

As iron phosphate (FePO4) is the key intermediary between the phosphate and LFP sectors, we developed an analysis to understand the cost structure of iron phosphate production, as well as its importance to LFP cathode production costs.

Roughly 1/6 of LFP cathode costs are accounted for by iron phosphate, and in turn around half of this comprises of phosphate raw material costs. Therefore, using the 2022 average price for lithium carbonate, phosphate accounts for 8–10% of the total cost of LFP cathode production under the most commercially widespread production method currently.

Pricing mechanisms in other battery materials were used as a basis for how to price high-purity phosphate for LFP producers – focusing on our client’s position in the market and considering how this may evolve in the future.

For nickel, cobalt, manganese and lithium, we categorised the price analysis using a range of different elements, such as the existence (or lack thereof) of an underlying metal price, the use (or not) of price indices for typical contracts, and how they currently work and have been evolving over time.

Using our analysis for other battery materials, we identified that manganese – specifically manganese sulphate, i.e., MnSO4 and HPMSM (high-purity manganese sulphate monohydrate) – had relevant similarities in relation to its role in the production of NMC batteries, when compared to the role of phosphates in LFP – in terms of market dynamics, resource base, and the importance of its costs in cathode production.

Approaches for pricing high-purity phosphate in LFP production

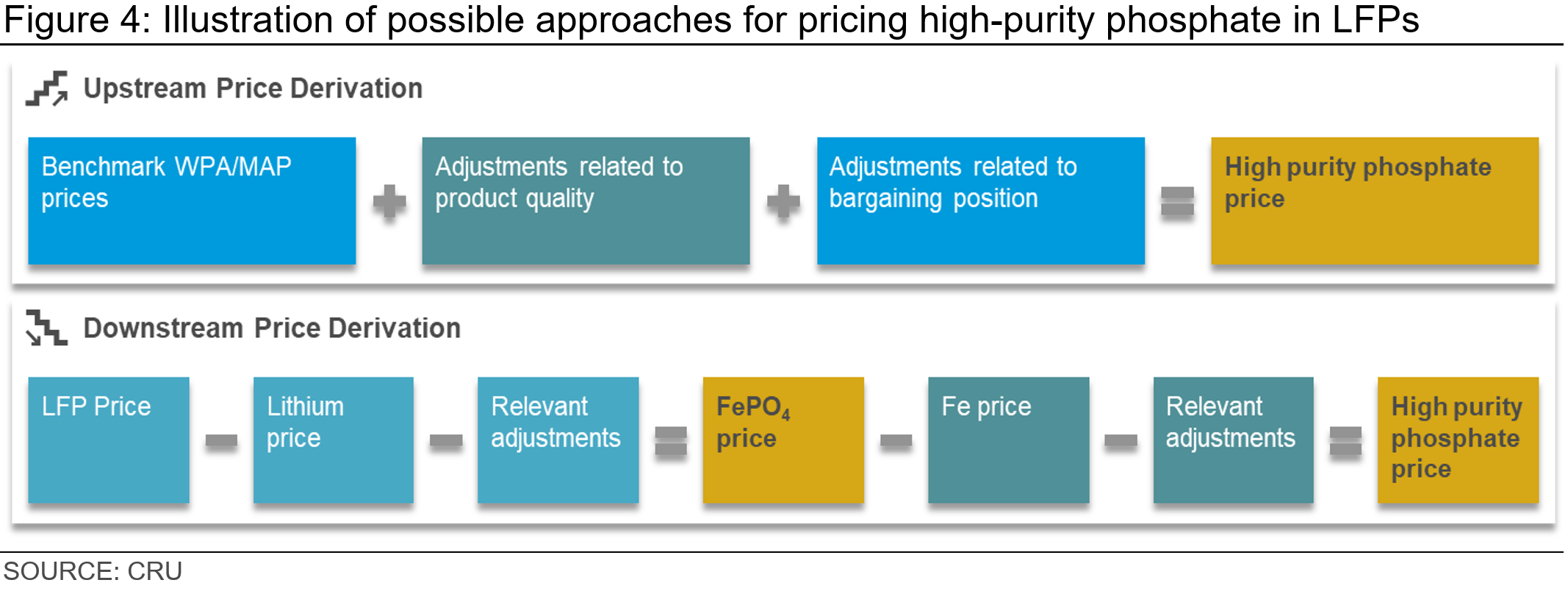

Generally, our analysis showed there are two approaches for pricing high-purity phosphate such as PWA and tMAP in LFP production – either an upstream or a downstream formula.

The downstream pricing approach was thoroughly examined but eventually discarded, due to the importance of other end uses in the pricing of high-purity phosphate currently, the relatively small share accounted for by phosphate in LFP production costs, and the comparatively opaque nature of LFP and lithium market prices.

Our conclusion was that a new entrant into the LFP industry should rely on an upstream pricing formula when aiming to achieve the best possible premium for its high-purity phosphate.

We presented theoretical pricing equations and analysis for different WPA and MAP price reference points and concluded that achievable premiums in the not-yet-existent LFP market outside of China will be a function of a PWA/tMAP producer’s market power. This may attract an additional premium, as well as adjustments for the P2O5 content and low impurities associated with their product.

The CRU team also presented a forward-looking analysis to our client, as the weighting of adjustments in the pricing formula and producer premium in the long term are uncertain, due to the volatile nature of battery materials markets and the nascent LFP industry outside of China.

The recent changes in government policy and regulation, such as the introduction of the Inflation Reduction Act in the US in 2022, combined with the backdrop of potential oversupply of iron phosphate and LFP cathode from China, was underlined as a key source of uncertainty in relation to the emergence of these premiums associated with high-purity phosphate for the LFP space. Government action to reduce dependence on China in the battery supply-chain has the potential to increase premiums outside of the country, but ineffective policy would leave these markets open to Chinese exports.

A strategic outcome for our client

CRU was able to develop a comprehensive upstream pricing mechanism that was flexible enough to account for the existing uncertainties in the market, but rigid enough to be accepted within the wider industry. The results of this study included detailed research into current pricing mechanisms associated with battery materials across the LFP value chain, and suggested strategic approaches for pricing phosphorus for usage in LFP production.

Reach out and share your key questions with us

CRU Consulting has extensive experience in market and product valuation support for major mining companies and projects, especially those within the battery materials value chains, as well as the fertilizer industry.

Our unrivalled expertise in these sectors, along with our dedicated global team of specialists, allow us to help clients deepen their understanding of the battery raw materials markets, and assist them with their high-level strategic decisions.

Explore this topic with CRU

Author Juan Brihet

Senior Consultant View profile

Contributor Piyush Goel

Consultant View profile

Contributor Garrett Haffner

Consultant View profile

Contributor Alex Laugharne

Principal Consultant View profile

Contributor Ionut Lazar

Principal Consultant View profile