CRU’s deep knowledge of slab and scrap mass flows to the rolling industry, as well as its understanding of practical realities in the use of scrap, helps clients all over the world to make risk-aware investment decisions.

This case study illustrates how CRU helped a client to identify the market potential for a slab expansion, and how to optimise the raw material mix by using recycled metal alongside primary aluminium. The approach would be relevant to any company considering either a casthouse expansion or a raw material optimisation.

CRU's approach

CRU has led the analysis of the aluminium rolled products industry since the 1980s, and tracks mill-by-mill mass flows as part of its Aluminium Rolled Products Cost Service. Alongside our work on casthouse products, we build up a view of the demand for, and supply of, third party slab, as well as the raw material mix at both smelter and rolling mill casthouses.

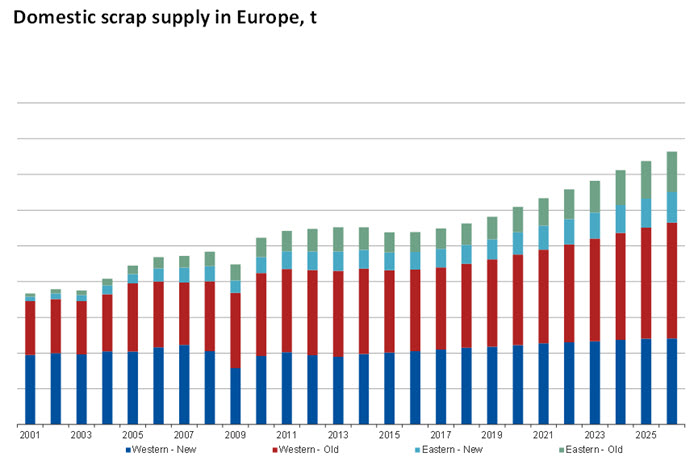

The supply of aluminium scrap typically depends on both the generation and availability of scrap given that not all scrap generated over a given period will become available in the marketplace. CRU models regional scrap markets on a bottom-up basis, taking into account historic aluminium consumption, recycling and recovery rates, and generation of new scrap at OEMs. We reconcile these against top-down figures (e.g. overall metal balance, trade data, remelter production) to form a view of current and forecast scrap supply.

Example: identifying customers and raw materials for a slab expansion project in Europe

Our client was a primary aluminium producer planning to invest in a casthouse expansion to produce rolling slab, some of which would be targeted at European producers of automotive body sheet (ABS). The client’s smelter was relatively high cost and so the client wanted to optimise raw material costs by procuring scrap for the expansion. CRU was engaged to address two key challenges:

• Demonstrate that there would be a market for the slab

• Identify how to secure sufficient quantities of the right types of scrap

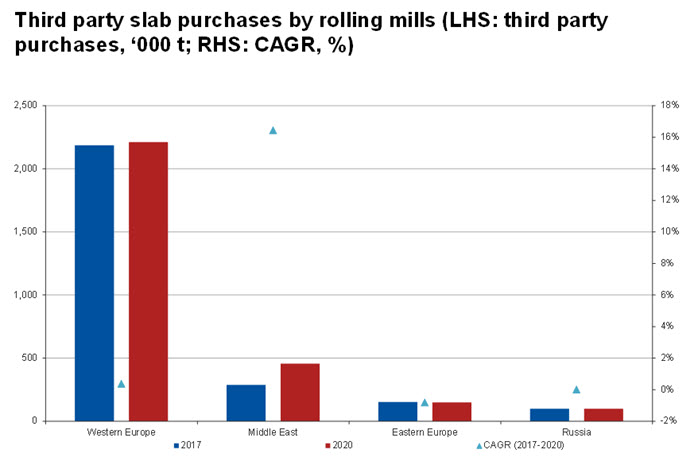

Rolling mills normally prefer to source slab internally for a number of reasons, for example raw material optimisation, flexibility on specifications and shorter lead times. In addition, rolling investments are often very large and the addition of an internal casthouse is a modest component. Many rolling mills require additional slabs from an external source, but historically these have mostly been internal company transfers. In North America over 80% of mills’ slab requirements are fed from internal supply and in Japan, this figure is over 90%. In Europe there is a much larger third party market for slab. In the post-World War Two era, integrated national champions built smelters near their power source and rolling mills near to industrial centres. As companies consolidated, this evolved into a pan-European web of slab transfers. More recently, the unfavourable economics of producing primary aluminium in Europe meant that rolling companies have been willing to import slab from further afield.

DATA: CRU

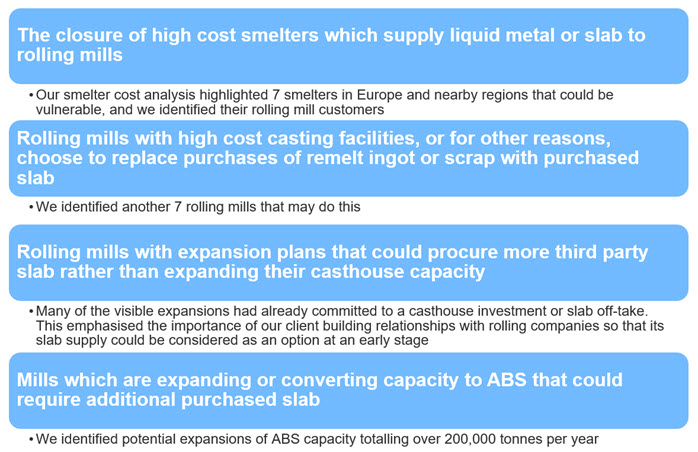

Our client understood that an investment in slab capacity would need to be backed by customer off-take agreements, and so we identified the potential for new customer demand. This could occur for one of four reasons:

We reviewed the approach to scrap sourcing taken by the leading slab producers (smelters, independent casthouses and rolling mills) in order to identify success factors and learnings. A number of models were evaluated, for example staying out of scrap collection altogether or integrating downstream into scrap processing and shredding.

While the recycling of high percentages of aluminium from packaging and some automotive applications has been commercialised and become economically attractive, the varied and unique compositions and performance requirements of ABS limit the suite of available recycled metal that can feasibly be used. Aluminium alloys used in ABS (5xxx, 6xxx and 7xxx alloys) contain high amounts of magnesium, manganese or zinc, which makes the recycling process more complicated than the lesser-alloyed aluminium used in other applications. Our client had thought that the local availability and affordability of used beverage cans (UBCs) would be an advantage, but we were able to explain how this was not the case, because of the cost of hardener additions and the low proportion that could be incorporated into the raw material mix. Moreover, the pool of post-consumer ABS scrap (i.e. old automobiles containing ABS) is still very small and in any case likely to contain a broad range of alloying elements and impurities.

This highlighted the importance to our client of partnering with its rolling mill customers, and in turn, their customers, the OEMs, to build closed-loop recycling opportunities and sustainable manufacturing solutions. This requires sizeable investment, but the long-term advantages of these systems – both financial and ecological – are significant. Until that is done, we advised that the client’s production of ABS rolling slabs will be limited to perhaps 15-25% recycled content. It could however achieve a higher proportion of recycled content when producing slabs for less demanding applications.

We evaluated the European scrap market and found that although scrap supply is increasing, investment in secondary aluminium capacity was also increasing the demand for scrap and would likely tighten the availability to our client. We recommended that our client should enter this market as soon as possible to secure the required material for the production of slab. This could be ideally conducted by entering an agreement with a network of major Western European remelters for a large offtake.

DATA: CRU

We also helped our client to understand likely scrap availability from the GCC going forwards. Aluminium recycling in the GCC it is still in its early stages, meaning that scrap is exported in large volumes for processing elsewhere – potentially to our client. We considered likely growth in scrap generation against a regional desire to undertake more processing and semi-fabricating locally. Given competition for scrap from other buyers, we recommended that the client could secure about 15-20% of its scrap requirements from the GCC and proposed practical means for doing so, recognising that the market is still limited, fragmented and highly deregulated.

Our work provided the client with an important reality check on the challenges of entering the slab market while relying on scrap as a feedstock. The client has since switched its attention to billet, where the barriers to entry are lower.

Conclusions

Decisions to invest in slab capacity are tied up with raw material sourcing: not only to identify sufficient competitive feedstock for the slab, but also in the case of scrap, to optimize the types of scrap available against the alloy types that will be produced. CRU’s deep knowledge of slab and scrap mass flows to the rolling industry, as well as its understanding of practical realities in the use of scrap, helps clients all over the world to make risk-aware investment decisions.